| Stock Data | |

| BOM | PONDYOXIDE |

| Exchange | BSE |

| Industry | Ferro & Silica Manganese |

| Price Perf. | |

| Last 5 Days | +0.39% |

| YTD | +50.18% |

| Last 12 Months | +66.30% |

“Pondy Oxides and Chemicals Ltd. has delivered a healthy quarterly result with a growth rate of 49.2% on year on top line and has delivered an earnings before interest tax, depreciation and amortization (EBITDA) of INR 17.75 crores for the first quarter 2023 vs INR 14.56 crores previous year showcasing a growth rate of 22%. The future outlook of the industry remains relatively positive status quo.“

-Ashish Bansal, Managing Director

Insights into the Q1FY23 earnings call:

Pondy Oxides and Chemicals, which mainly deals with base metal recycling is likely to be affected by the slowdown in infrastructure, automotive and various other sectors in tandem with the global economic cues.

To tackle the uncertain outlook among various global industrial factors, the company has decided to pursue a diversification strategy, targeting other nonferrous metals and recycling materials. The management suggests that these portfolio diversification steps will be reflected in the coming quarters. As per the management, the focus will be on rubber, glass, paper and oil materials while the company has already taken steps to set up a research & development arm in Lithium Ion. With the payback period to be estimated around 18-24 months for the majority of the segments, there seems to be a steady working capital cycle.

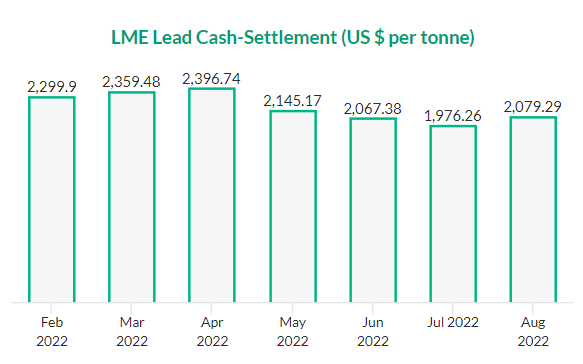

Meanwhile, the Indian economy has shown signs of positive growth and the nation’s economic growth prospects seem optimistic. Additionally, the global refined lead consumption has seen a dramatic increase and the segment is expected to grow at a substantial pace.

Thus, management remains optimistic on the future of the company as they believe that the firm is well-equipped to tackle market volatility and garner steady results. The management projects an 18%-20% growth in volumes with the trend in profitability to remain positive and consistent with FY22. Also, as per the management, all non ferrous metals expansion are projected to provide 8%-10% returns, while other segments such Plastics and Lithium Ion are expected to provide at least 15% returns in the future.

Investment Thesis

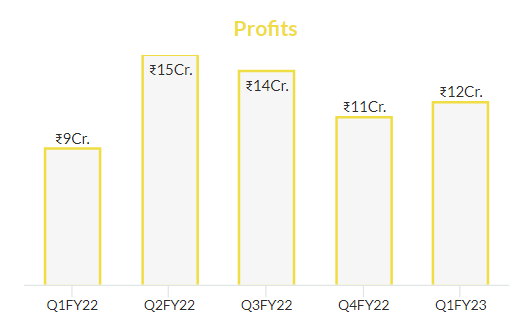

Stellar Results: Pondy Oxides opened the FY23 with a robust performance wherein the total income grew 49% to INR 364 crores in Q1 FY23 from INR 243.97 crores in Q1 FY22. Net profit jumped 35% to INR 11.59 crores. Sequentially, the net profit rose 9%. The interest cost for the company has reduced by over 7% on year resulting in an improved bottom line. Further, the EPS grew by 35% during the same period.

Improved Cost Efficiency: The company has further managed its expenses very well as the cost of raw materials consumed have gone down 16% from the last quarter. It has installed a new furnace in this quarter and added some smelting capacities. Further, a certain level of automation has been introduced at the plant level, which will further be studied and increased to attain a higher level of automation in the coming years translating to higher efficiencies.

Bonus Issue To Boost Liquidity: The company has recommended issue of bonus shares subject to the approval of shareholders in the ratio of 1: 1 i.e. one new bonus equity share of INR 10 each to be issued for every one existing equity share of INR 10- each held by the shareholders on the cut-off date of Sep. 14, 2022. With the issue of Bonus, the current number of shares will be double and with higher supply the liquidity is likely to improve.

Diversified Supply Base: The company has a diversified consumer base globally, the raw material procurement is largely inclined towards imports. On account of that, the firm has taken steps to increase the domestic supply base. The diversified consumer and supply base along with a diversified product portfolio works positively to reduce the risk associated with the business.

Recycling Initiatives: The company’s collaboration with Ace Green Recycling to set up a GHG emission-free battery recycling facility has progressed and is expected to be operating in Q3FY22. The management is confident in its venture into Recycled Plastics according to the perceived industry dynamics. The management believes that recycled plastics will see a significant rise as it will be mandated for companies to involve recycled plastic into their manufacturing process. In order to benefit from the aforementioned hypothesis, the company plans to invest around INR 30 crores in various stages in the Plastics segment. Along with that, the company will continue its growth plans in different products on the recycling front with a plan to invest around INR 40-50 crores on various other non-ferrous segments.

Margin Outlook: There has been an increasing trend of cost of additives and chemicals in Smelting like Coal, Soda Ash, Cast Iron and Furnace Oil, refining like caustic soda, sodium nitrate and RGS Powder), cost of utilities and has resulted in marginal decrease in gross margin levels to 11% vs 12.25% previous quarter which is in line with our current industrial benchmarks. We expect a correction in such costs in the coming quarters as part of the business cycle.

Company Description:

Incorporated in the year 1995 and headquartered in Chennai, Pondy Oxides and Chemicals is India’s leading non-ferrous recycling company and the largest secondary lead metal manufacturing company in India. The company recycles lead, copper, zinc and plastic in various forms.

The firm has established, POCL Future Tech Private Limited as a subsidiary business, and it will engage in business in areas such as plastics, where it will use its own and other industrial plastics, e-waste, lithium ion recycling, rubber, oil, glass, paper, and other value-added products.

Research Summary:

The revenue of the company has seen a drastic increase with the increased demand of Lead & other metal alloys. The lead metal’s increased demand comes mainly from the Automotive Industry. Along with that, lead as a base metal is used in various industries. So, essentially a boom in development will be largely reflected in the prices of lead. The company monitors its hedging strategies to protect itself from the volatile nature of the commodity market.

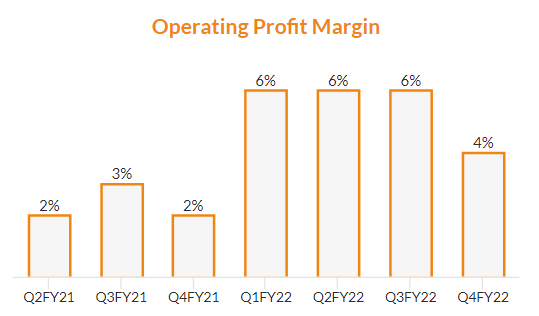

The company has indicated its expansion strategy into segments that provide higher margins which can be clearly observed with the increase in the Operating Profit margins of the firm. The firm has focused on value added segments and unique specialized alloys that provide the firm with higher margins.

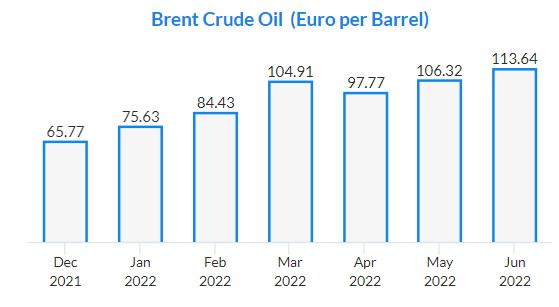

The recent increase in fuel prices and supply disruption have posed themselves as headwinds for the company. The Ukraine – Russia war has exacerbated these problems as observed with the sharp increase in the Brent Crude Oil.

There has been a rise in the cost of smelting and refining along with the rise in freight charges and fuel prices. This rise in various factors of production has impacted the profitability of the firm.

However, the long term prospects of the company seem to paint a brighter picture. The company has been consistently showcasing a rise in sales coupled with higher margins.

The company also provides exposure to a booming industry where the firm itself has positioned itself as one of the market leaders.