Company Description and Outlook:

Incorporated in the United Kingdom, Vedanta Resources Limited is engaged in exploring, extracting and processing minerals and oil & gas. The group participates in the exploration, production and sale of zinc, lead, silver, copper, aluminium, iron ore and oil & gas and has a presence across India, South Africa, Namibia, Ireland, Australia, Liberia and UAE. The Group is also in the business of commercial power generation, steel manufacturing and port operations in India and manufacturing of glass substrate in South Korea and Taiwan. Let’s have a look at the business vertical of the company:

- Zinc:

During FY22, Zinc International continued to ramp up production from its flagship project Gamsberg mine and achieved record production of 170 kilotons. Several milestone projects were completed including rougher cells commissioning at Gamsberg resulting in throughput increase. During FY22, total production stood at 2,23,000 tonnes, 10% higher y-o-y. This was primarily through ramp up and higher production in Gamsberg. At Black Mountain Mining (BMM), production was 52,000 tonnes, 9% lower y-o-y. This was mainly due to lower grades of zinc (2.1% vs 2.6%), lead (2.1% vs 2.3%), lower zinc recoveries (75.2% vs 80.2%) and lower lead recoveries (81.6% vs 81.8%) offset by 13.6% higher throughput.

Gamsberg’s production was at 170,000 tonnes as the operation continued to ramp up with improved performance during the current financial year. At Skorpion Zinc engagement with technical experts to explore opportunities of safely extracting the remaining ore is ongoing. The pit optimization work is complete. The business is in the process of evaluating options to restart mining.

While in Indian subcontinent, mine production progressively improved during the year with record ore production for the full year up 6% y-o-y to deliver a record 16.3 million Metric Ton, supported by strong production growth at Zawar mines, SK Mines and Rampura Agucha mine, which were up 12%, 8% and 6% respectively. Highest ever Mined metal production was up 5% y-o-y to 1,017 kilotons primarily on account of higher ore production & milling recovery partly offset by lower ore metal grade.

Outlook:

The immediate priority of the company is to ramp up the performance of their Gamsberg Plant at Designed capacity and simultaneously develop a debottlenecking plan to increase Plant capacity by 10% to 4.4Mt Ore throughput. Likewise, BMM continues to deliver stable Production performance and focus is to debottleneck its Ore volumes from 1.6Mt to 1.8Mt. Skorpion is expected to remain in Care and Maintenance for H1 FY23 while management is assessing feasible & safe mining methods to extract Ore from Pit 112.

In addition to above, the other priorities of the company includes:

- Completion of Magnetite project in H1 FY 2023.

- Commencement of construction activities of Gamsberg Phase 2 project with aim to start production in H2 FY2024.

- Continue to improvise Business case of Skorpion Refinery Conversion Project and Gamsberg Smelter Project through Government support, Capex and Opex reduction.

- Oil and Gas:

During FY22, Oil & Gas business delivered gross operated production of 161 Kilo barrels of oil equivalent per day(kboepd), down by 1% y-o-y, primarily driven by natural reservoir decline at the MBA fields. The decline was partially offset by addition of volumes from ramp up of gas volumes, commissioning of Aishwariya Barmer Hill facility, impact of polymer injection in Bhagyam and Aishwariya fields, new infill wells brought online in Mangala field and reduced operational downtime.

In Open Acreage Licensing Policy(OALP) blocks, seismic acquisition programs have been completed in Assam, Cambay, Rajasthan and Offshore region. As part of the 15 well drilling program, 11 wells have been drilled till date across basins. Of these, two hydrocarbon discoveries in Rajasthan (KW-2 Updip and Durga -1) and one in Cambay (Jaya-1) have been notified as oil and gas discoveries.

Outlook:

The company is very much committed to deliver their world class resources with ‘zero harm, zero waste and zero discharge:

- Infill projects across producing fields to add volume in near term.

- Unlock the potential of the exploration portfolio comprising of OALP and PSC blocks.

- Continue to operate at a low cost-base and generate free cash flow post-capex.

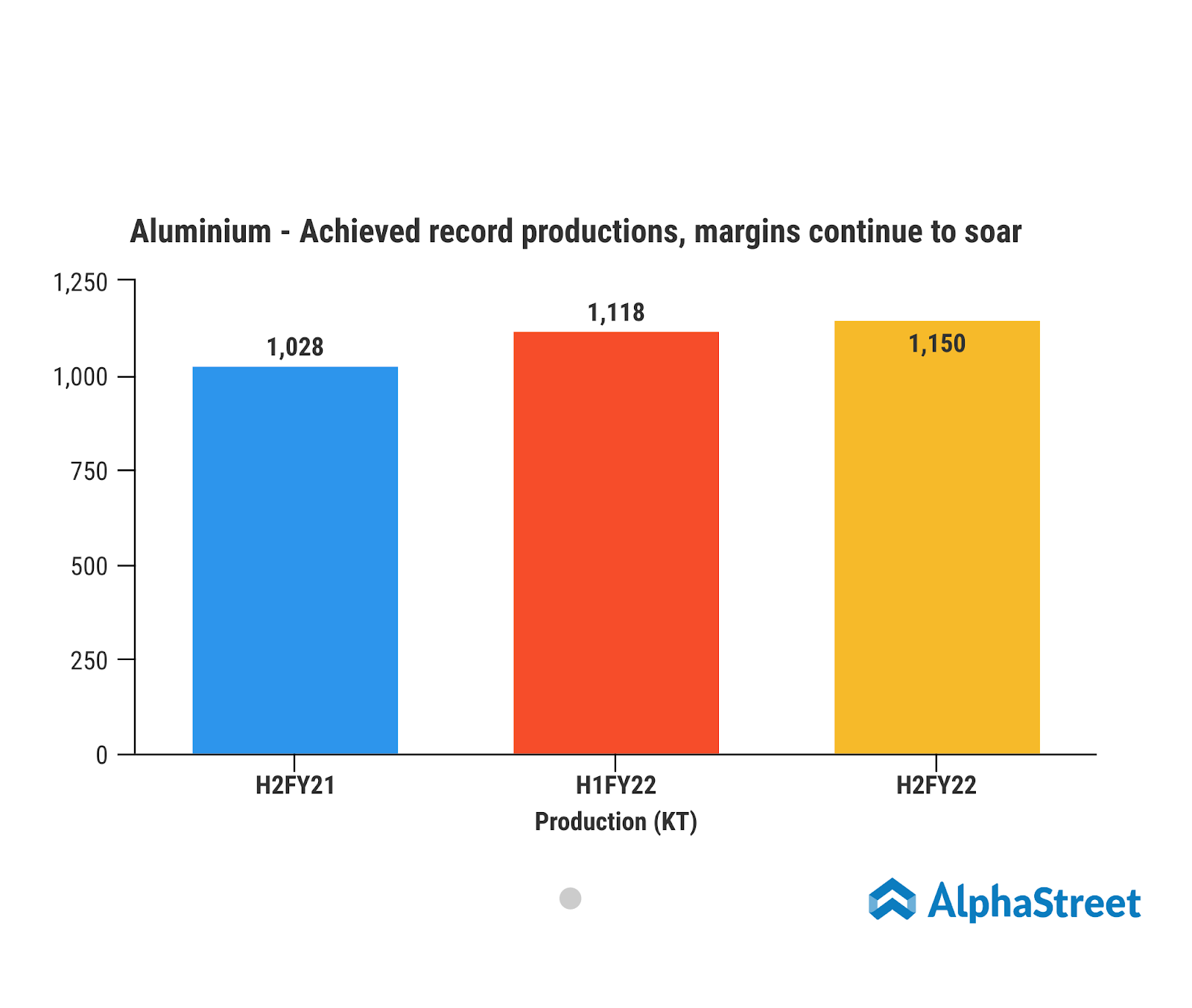

- Aluminium:

In FY22, the Aluminium smelters achieved India’s highest production of 2.27 million tonnes. It has been a remarkable year as the company inched towards their vision of 3 MTPA Aluminium. Though this year saw headwinds in cost due to rising commodity prices and the coal crisis, the group undertook several structural initiatives to make their business immune from market induced volatilities. These reforms coupled with continued focus on operational excellence, optimizing the company’s coal and bauxite mix, improved capacity utilization across refinery, smelter and power plant, will further help reduce the company’s cost in a sustainable manner and make the business more predictable. And improving the price realisation to improve profitability in a sustainable manner through a well structured PMO approach. The hot metal cost of production for FY2022 stood at US$ 1,858 per tonn. We also achieved record production of 1.97 million tonnes at the alumina refinery through continued debottlenecking.

During the year, the company launched their low carbon Aluminium brand, Restora, which is manufactured using Renewable energy through their two product lines – Restora and Restora Ultra. GHG emission intensity for these product lines are about half the global threshold for low carbon Aluminium. This is the company’s strong step towards their commitment to achieve GHG emission intensity reduction of 25% by 2030 and Net zero carbon by 2050. Restora Ultra is an ultra-low carbon Aluminium brand in collaboration with Runaya Refining.

Outlook:

With the primary Aluminium demand expected to increase and the ongoing geopolitical issues, the outlook for FY2023 is strong. European premiums are soaring while US premiums are supported by high demand and low stocks. The deficit is expected to intensify in 2022. India’s market is expected to have robust growth, supported primarily by growing industrial activity and government’s focus on infrastructure sector and domestic manufacturing in the country.

Several government initiatives (Make in India, Production-linked Incentive for domestic manufacturing, National Infrastructure Pipeline and National Rail Plan) will enhance Aluminium demand, going forward. Vedanta continues to expand its value-added product portfolio in line with evolving market demand, making it poised to grow in the Indian Aluminium market.

While the market remain bullish, the core priorities of the company include:

- Asset Optimisation: Deliver alumina and Aluminium production through structured asset optimisation framework

- Growth: Aluminium capacity expansion to 3 MTPA, Value added product capacity expansion to 90%, Alumina capacity expansion to 6 MTPA.

- Raw Material Security: Enhance bauxite and alumina security through LTCs and new

- mines auctions.

- Coal security: 100% operationalisation of Jamkhani, Radhikapur and Kuraloi coal block, improve linkage coal materialization.

- Power:

During FY22, the power sales were 11,872 million units, 5% higher y-o-y. Power sales at TSPL were 8,259 million units with 76% availability in FY22. At TSPL, the Power Purchase Agreement with the Punjab State Electricity Board compensates the company based on the availability of the plant. The 600MW Jharsuguda power plant operated at a lower plant load factor (PLF) of 53% in FY22. The 300 MW BALCO IPP operated at a PLF of 63% in FY2022. The MALCO plant continues to be under care and maintenance from 26 May 2017, due to low demand in Southern India.

During the current year, the company remained focused on maintaining the plant availability of TSPL and achieving higher plant load factors at the BALCO and Jharsuguda IPPs. The company’s priorities will be to:

- Resolve pending legal issues and recover aged power debtors.

- Achieve higher PLFs for the Jharsuguda and BALCO IPP.

- Improve power plant operating parameters to deliver higher PLFs/availability and reduce the non-coal cost.

- Ensuring safe operations, energy & carbon management.

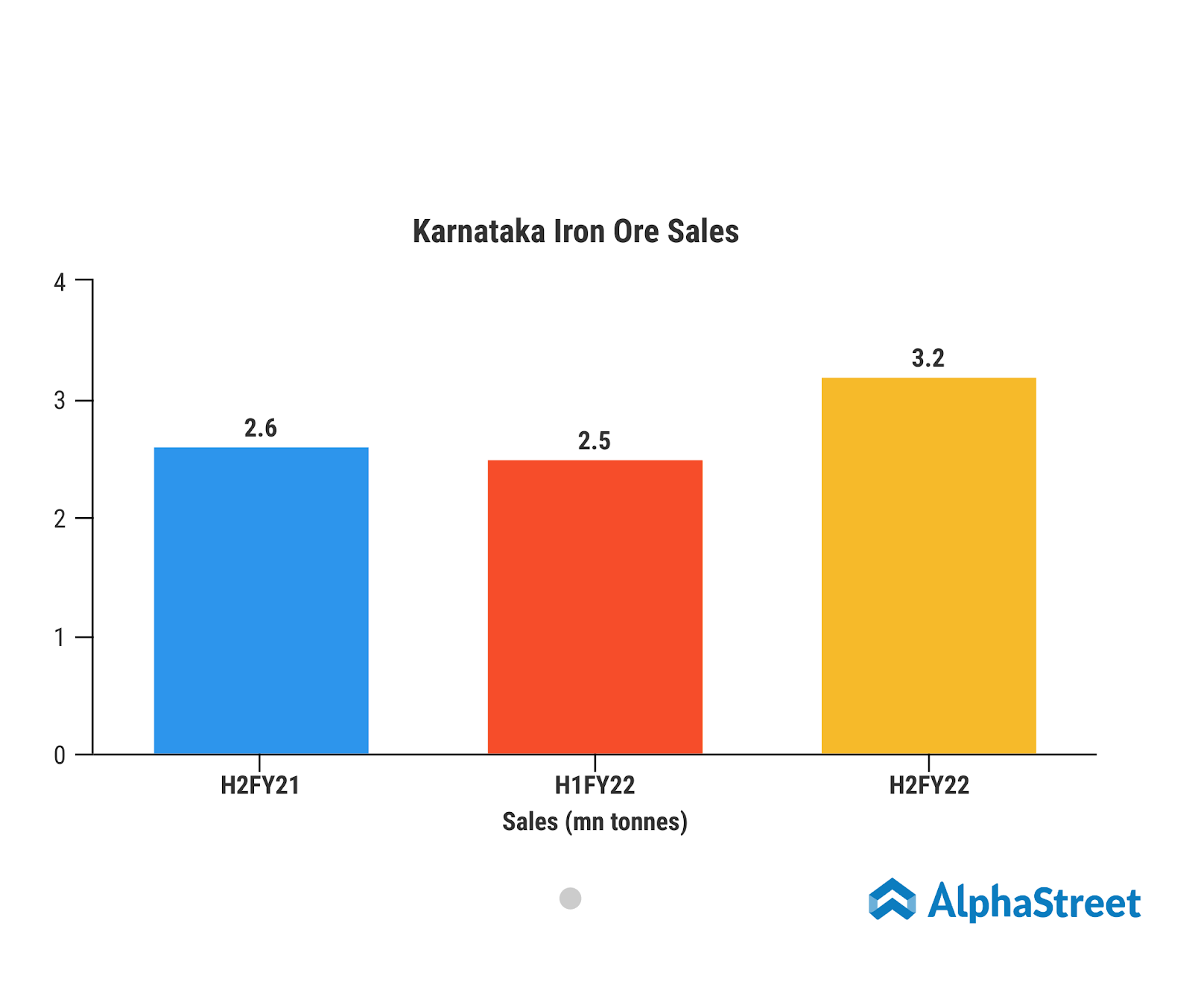

- Iron Ore:

Production of Crude ore at Karnataka stood at 5.60 net million tons. With the order of the Central Empowered Committee (Supreme Court appointed body) on 21st March’ 20, the company’s annual mining capacity has been increased up to 5.89 MTPA. In line with this the Govt. of Karnataka on Feb’2021 has allocated the production quantity of 5.60 wet million tons from FY2021 onwards to maintain the SC allocated district cap. Meanwhile, operations in Goa remained in suspension in FY2021 due to a state-wide directive from the Supreme Court. However, the group continues to engage with the Government to secure a resumption of mining operations.

Outlook:

The near-term priorities includes:

- Resume mining operations in Goa through continuous engagement with the government and the judiciary.

- Realign and revamp resources, assets, HEMM’s for starting the mine’s operation

- Grow the footprint in iron ore by continuing to participate in auctions across the country, including Jharkhand.

- Advocacy for removal of E-auction/trade barrier in Karnataka.

- Steel:

ESL is an integrated steel plant (ISP) in Bokaro, Jharkhand, with a design capacity of 2.5mtpa. Its current operating capacity is 1.5mtpa with a diversified product mix of Wire Rod, Rebar, DI Pipe and Pig Iron. This year the business has achieved the highest ever hot metal production of 1,355 KT, since acquisition. In FY22, ESL Steel Limited (ESL) has achieved the highest ever NSR during the year since acquisition resulting in a favorable EBITDA margin of US$74 per tonne.

Though there have been significant gains in the Sales & NSR front. However, operational inefficiencies, higher raw material prices of coking coal & other market factors resulted in higher cost of sales. The company is trying to stabilize their raw material prices. The company has acquired two iron ore mines to achieve raw material long term security & pricing stability.

During FY22, the company produced 1,260,000 tonnes of saleable product, higher by 6% y-o-y on account of increased availability of hot metal due to higher production. The priority remains to enhance production of value-added products (VAPs), i.e., TMT Bar, Wire Rod and DI Pipe. ESL maintained 78% of VAP sales, in line with priority.

Financial Snapshot:

Vedanta Resources recorded net revenue of $17.6 billion in FY22 as compared to $11.7 billion in FY21 depicting a growth of 50% YoY. This was primarily driven by higher commodity prices, higher volumes of Aluminum, Copper, Talwandi Sabo Power Limited(TSPL), Iron Ore Business(IOB) and Ferro Alloys Corporation Ltd(FACOR), increased premium at Aluminum and Hindustan Zinc Limited, rupee depreciation and partially offset by lower power sales at Vedanta Aluminum and Bharat Aluminum Company. While the company reported a net profit of $825 million which was up by 172% as compared to $303 million in FY21.

The company further reported an all time high consolidated EBITDA at $6.3 billion, 65% higher YoY (FY2021: $3.8 billion). The Group generated free cash flow (FCF) post-capex of $2.083 billion (FY2021: $1,253 million, when million is in 1000’s convert to billion), driven by strong cash flow from operations and lower sustaining and project capital expenditure.

The company also has a strong liquidity position with cash and cash equivalents of $4.4 billion. While the net debt to EBITDA has been lowest in the past 5 years at 1.9 times. Not only this but the company has delivered a total shareholder return of 269% in the last 10 years.

To know more about the company’s financials. Click Here

What we like:

- Experienced management team: The group is run by a strong management team with more than 30 years of experience and 76,000+ employees working for the same vision. The group has an Impeccable track record of honoring all capital market commitments and is also committed to prioritize deleveraging by $4 bn over 3 years.

- Strong Asset base: With a worldwide network of consumers, Vedanta has their mines and has built their manufacturing units not only in India but also abroad. This gives them access to consumers globally. Further, the company with its strong and dedicated customer relationship management has been able to attain a high level of customer satisfaction.

- Strong Financial Position: Automation of activities, successful marketing strategies for their products, success at execution of new products and highly skilled workforce has given Vedanta Resources a strong financial position in its industry.

- Future Driven: The company has partnered with ‘Foxconn’ to start Semiconductors production.This provides the group with large value creation potential as the semiconductor industry is pretty consolidated with very few players and the need for semiconductors is only going to rise in the future.

Factors to consider:

- Government Intervention: Any intervention by the Government in the mining business can cause operation inefficiency and affect the top line of the company.

- Organization Structure: The current and even the previous business model limits the expansion of new products and limits the growth of the company in different sectors.

- Vedanta had augmented large capacity through acquisitions and CAPEX, which was largely debt funded. Any measure by which the company fails to reduce the debt might affect the performance of the company.

Recent Concall Highlights:

- The company plans to infuse $687mn in new growth CAPEX projects in the Oil and gas segment, this includes $360mn to monetize 52.6 Million barrels of oil equivalent reserves and $327mn to grow resources.

- In the Aluminium space, the group plans to put $1.4 Bn growth CAPEX over the next 2 years. The vertical integration is focused to reduce market volatility impact and create value.

- While for its Zinc international business, the company plans to do a CAPEX of $466mn on the Gamsberg phase 2 project by 1HFY24. This includes constructing a new 4 MTPA Concentrator (200 kt MIC). They plan to commission it in 3QFY24.

- Another CAPEX investment of $348 mn is to be done in its ESL steel segment by end of FY23. This will also include doubling Hot Metal Capacity to 3.0 MTPA from 1.5 MTPA.

- The company aims to be a net carbon zero company by 2050 or sooner with 25% absolute GHG reduction by 2030.

- The company has partnered with ‘Foxconn’ to start Semiconductors production by the end of FY23.