“The Omnichannel strategy enables customers to move between online and offline and vice-versa in a frictionless manner. It has been a huge structural shift for your Company, which is now reinventing the way it does everything. The Omnichannel strategy has six domains: (i) Geographic expansion, (ii) Bajaj Finserv app, (iii) Bajaj Finserv website, (iv) Payments, (v) Productivity apps, and (vi) Customer data platform (CDP). During this year, your Company has significantly advanced on all of these. Once fully implemented, Omnichannel will make Bajaj Finance a truly customer-centric digital enterprise.”

Sanjiv Bajaj, Chairman

Stock data

| Ticker | BAJFINANCE |

| Exchange | BSE and NSE |

| Industry | Finance |

Price Performance:

| Last 5 days | +0.76% |

| YTD | +14.08% |

| Last 1 year | +1.22% |

Company description:

Bajaj Finance Limited is a prominent non-banking financial company (NBFC) in India, specializing in lending and allied financial services. Founded in 1987, the company is a subsidiary of Bajaj Finserv, one of India’s leading financial conglomerates. Bajaj Finance has earned a reputation for its diversified product portfolio, customer-centric approach, and strong digital presence.

Business Segments:

- Consumer Lending:

During FY22, BFL financed 12.7 Million customers and is one of the leading lenders of consumer electronics, furniture, and digital products. The company has issued ~30 Million Cards to finance over 13.1 Million purchases. Financing customers through EMI cards on online portals is one of the important businesses of the company and it showed a 48% growth versus the previous year. This segment accounted for 32% of the AUM of the company.

- Mortgages:

The segment offers Home loans, loans against properties, developer finance and lease rental discounting, and many more and the company has the right to the possession of the vehicles or the properties in case of default by the customer and the company sells those assets on an auction basis. This segment accounted for 31% of the AUM of the company.

- SME Lending:

Under this segment, the company offers secured and unsecured loans to small businesses. The business is present in over 1,500 locations in India to provide working capital loans and term facilities. SME Business loans AUM grew by 25% during FY22. This segment accounted for 13% of the AUM of the company.

- Rural Lending:

BFL started this initiative in the year 2013 and now is operational in 2,136 locations across 21 states and UTs. The segment had an AUM of 19,430 crores, an increase of 32% over the previous year. This segment accounted for 10% of the AUM of the company.

- Commercial Lending:

Under this segment, the company provides loans to auto component manufacturers and the light engineering industry, financial institutions, specialty chemical and pharma industry, and other midmarket companies. It recorded an AUM growth of 39% over FY21 to Rs. 11,498 crores. This segment accounted for 6% of the AUM of the company.

Business Model:

Bajaj Finance operates on a customer-centric business model with a strong focus on digital innovation. Its model can be summarized as follows:

- Customer-Centric Approach:

Bajaj Finance places the customer at the center of its operations. It aims to understand and meet the unique financial needs of each customer through a personalized approach.

- Digital Transformation:

The company has heavily invested in digital technology and offers online loan applications, approvals, and digital payment solutions. Its digital presence enhances convenience for customers.

- Risk Management:

Bajaj Finance maintains a robust risk management system to assess creditworthiness and mitigate lending risks. This approach ensures the company maintains a healthy loan portfolio.

- Cross-Selling:

The company leverages its diversified product portfolio to cross-sell financial products and services, deepening its customer relationships and expanding its market share.

Housing and Depository Business:

BFL also has its presence in the Housing Finance segment through its 100% subsidiary ‘Bajaj Housing Finance Ltd.’ which has an AUM of Rs. 53,322 crores. The company operates in the Depository business through Bajaj Financial Securities Ltd. and it acts as a stockbroker and depository participant.

Investment in BFS-D:

During FY22, the company along with Bajaj Finserv Ltd. made joint investments in the form of Equity shares and/or Convertible Loans or Security into Equity Shares for a sum of Rs. 283.16 crores. Out of this, investment in the equity share capital of BFS-Direct stands at Rs. 2.69 crores representing 19.90% of its capital. BFS-Direct is neither a subsidiary nor an associate of the Company.

Pan India Presence:

BFL has a total of 3,504 branches spread across India out of which 2,136 branches are based in Rural Areas and the rest from Urban areas. The company has an overall distribution network of 133,200+ active networks spread across India.

Competitive Cost of Funds

In Q1 of FY24, the cost of funds stood at 7.61% and the borrowing mix of the company was Banks: 47%, NHB: 7%, Money Markets: 34%, Assignment: 12%

Deposits:

The deposits book represented a growth of 19% y-o-y and currently contributes to 19% of the company’s consolidated borrowings as on 31st March 2022. Retail deposits contribute to 69% of total deposits, as against 73% in the previous fiscal.

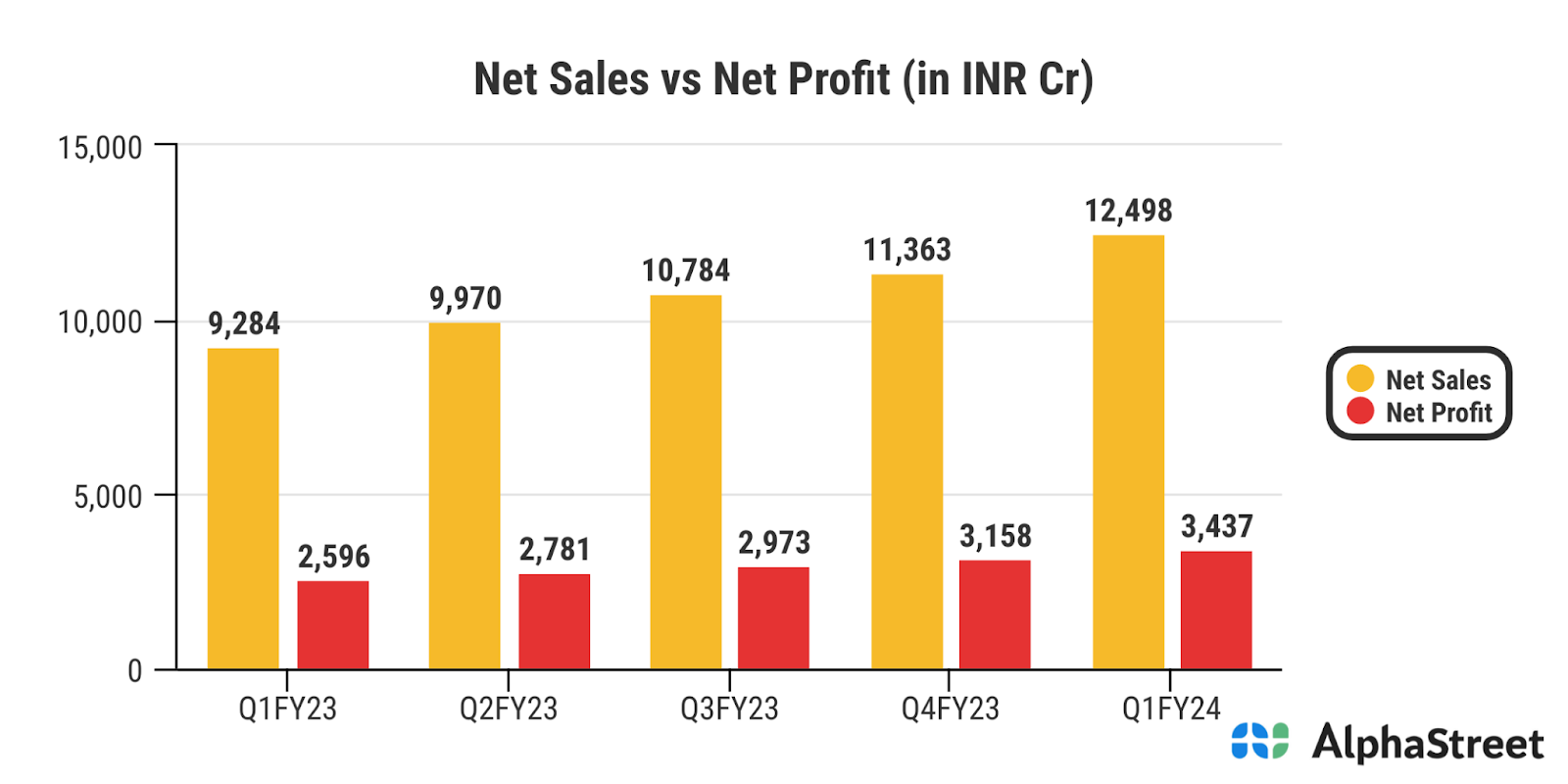

Financials:

What we like:

- Amongst Largest NBFCs in India:

Bajaj Finance (BFL) started its journey in the year 1987 as a vehicle financing company and now is one of the largest and most diversified NBFCs in India. During FY22, AUM increased by 29% to Rs. 197,452 crores.

- Largest Financier for Bajaj Auto:

The company financed the purchase of over 6,37,000 two-wheelers and about 72,000 three-wheelers in FY22 for Bajaj Auto Ltd. This constituted over 37% of domestic sales of Bajaj two-wheelers and 44% of domestic sales of Bajaj three-wheelers.

- Lowest NPA among the NBFCs:

Bajaj Finance has one of the lowest NPAs in the NBFC Industry and the company reported a Net NPA of 0.31% for Q1FY24. Provisioning coverage on stage 1 & 2 stood at 131 bps as of 30 June 2023

- Omni-channel transformation to become even more apparent:

The Omni-channel platform has provided a fully-integrated, seamless experience for customers to navigate between online and offline channels in a frictionless manner. In FY24, it will further accelerate the execution of its Omnichannel strategy and gain increased penetration across the country by opening additional 400-450 locations. With this transformation, BAF targets a substantial rise in business volumes, enriched customer experience, and a leaner cost structure. This should generate greater customer acquisition, higher customer loyalty, more profitable cross-selling, and better margins for each of its businesses. The company has made significant progress in multiple domains across its Omni-channel strategy.

- Customer franchise growing from strength to strength:

Overall customer franchise grew 20% YoY to ~69m. Of the total EMI card customers, 2% were financed across all sales finance categories (a sharp decline from ~44% in FY22) and 50–60% over the three years pre-COVID. Urban B2C AUM grew 30% YoY as against 27% in FY22. Consolidated AUM witnessed a robust growth of 25% YoY to INR2.47t and the proportion of unsecured loans declined to 42% (vs. ~43-44% over the prior two years).

- Distribution income, a key catalyst for healthy improvement in fees:

Services and administrative fees grew 34% YoY to ~INR 15.5b, with their contribution to overall fees coming down to 36% (vs. 38% in FY22). We believe this may be driven largely by a) much lower conversion fees (from term to hybrid flexi loans) than in FY22 and b) much lower penal interest charges (if any). Fees on value-added services grew 12% YoY. The contribution of fee and commission income to overall profitability remained high at 1.8% of average assets (up ~20bp YoY and on par with FY20 levels). Distribution fees, which increased 60% YoY, were driven by significant co-branded credit card usage (interchange fees), distribution of third-party products and incremental sourcing of credit cards. The number of EMI cards / co-branded credit cards outstanding grew at a rapid pace of 40%/24% YoY to ~42m/~3.5m.

Factors to consider:

- Economic downturns or adverse events can affect the quality of the company’s loan portfolio and result in non-performing assets (NPAs).

- The company is exposed to interest rate fluctuations, which can impact its net interest margins and profitability.

- Bajaj Finance faces competition from traditional banks, other NBFCs, and emerging fintech players, intensifying market rivalry.

Conclusion:

Bajaj Finance Limited has established itself as a formidable player in India’s financial services sector, with a diverse portfolio, a strong digital presence, and a customer-centric approach. While it benefits from market leadership and cross-selling opportunities, it also faces regulatory challenges and competition. Investors should carefully consider these factors, along with their investment objectives and risk tolerance, when evaluating Bajaj Finance as a potential investment opportunity. Staying informed about the company’s performance and industry dynamics is essential for making well-informed investment decisions.