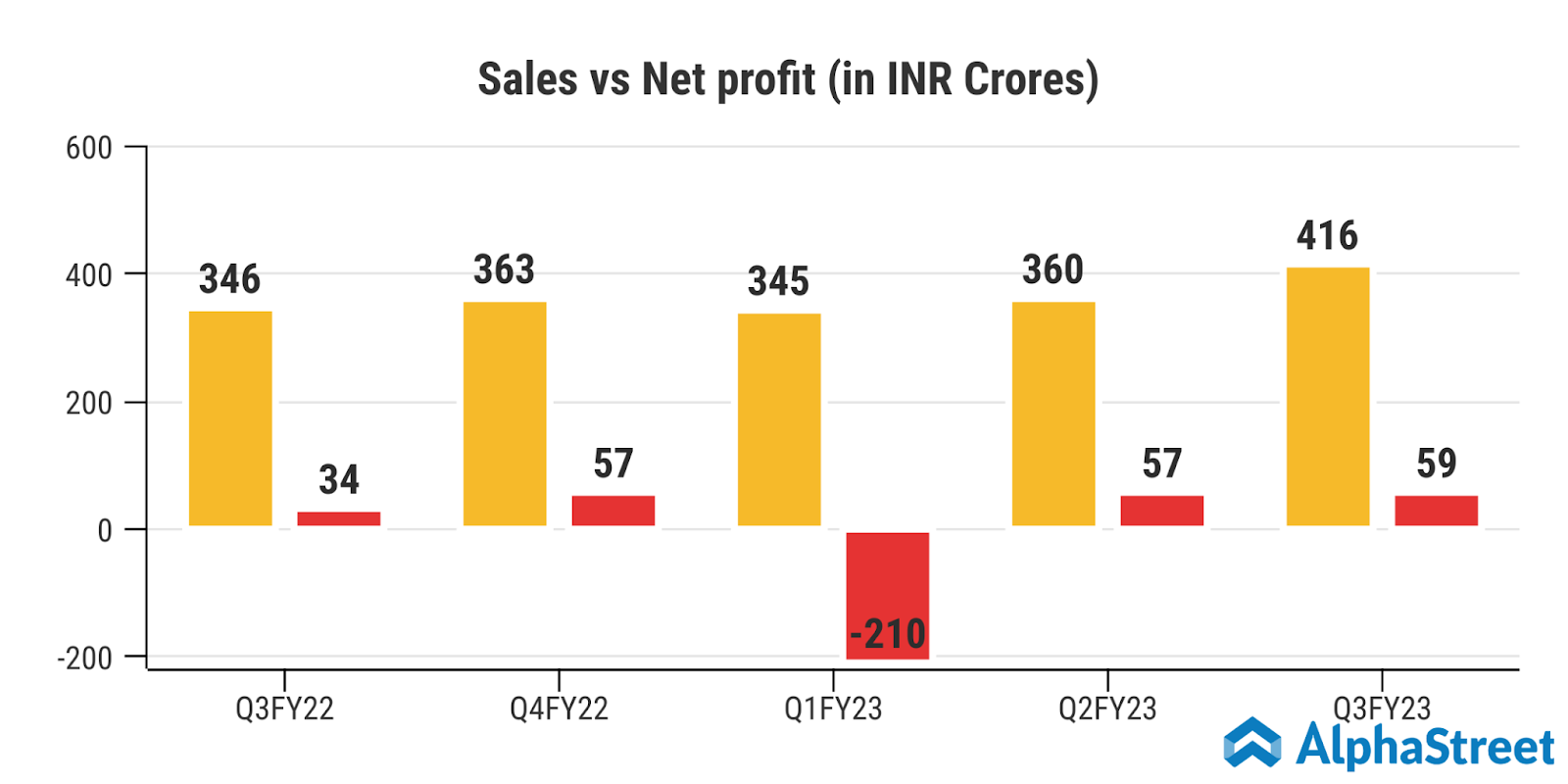

“Our primary focus during Q3FY23 was to stabilize our business, have growth and profitability back on track, and achieve guided growth. We are glad to announce that our performance for the quarter has marked significant improvement in financial and operational performance coupled with consistent improvement in asset quality, which helped us achieve our quarterly PAT of INR 55 crore, up by 35% on YoY basis.”

– Mr H.P. Singh, Chairman and Managing Director

Stock Data:

| Ticker | SATIN |

| Exchange | NSE and BSE |

| Industry | MICRO-FINANCE |

Price Performance:

| Last 5 days | +4.99% |

| YTD | -20.6% |

| Last 1 year | +10.8% |

Company Description:

Founded in 1990, Satin Creditcare Network Limited is a non-banking finance company (NBFC), licensed by the Reserve Bank of India. The company provides microcredit to economically active women in rural, semi-urban, and urban areas; loans for income generating purposes, such as agriculture, transportation, trading, and production related business activities; loans for water and sanitation facilities; and loans to merchants, retailer, wholesaler, manufacturing, service providers, salaried, self-employed professionals, and agri business. It also offers loans to self-employed professionals, and self-employed individuals/non individual entities; loans to corporate institutions and microfinance companies; financing for solar lamps, bicycles, and consumer durables; and housing finance products. Satin Creditcare Network Limited is a micro-finance institution (MFI) in the country with presence in 23 states and more than 82,000 villages.

Business Verticals:

The business is primarily based on the Joint Liability Group model, which allows the company to provide collateral-free, microcredit facilities to economically active women in both rural and semi-urban areas, who otherwise have limited access to mainstream financial service providers. It also offers loans to individual businesses and Micro, Small & Medium Enterprises (MSMEs); product financing for the purchase of solar lamps, as well as loans for the development of water connections and sanitation facilities.

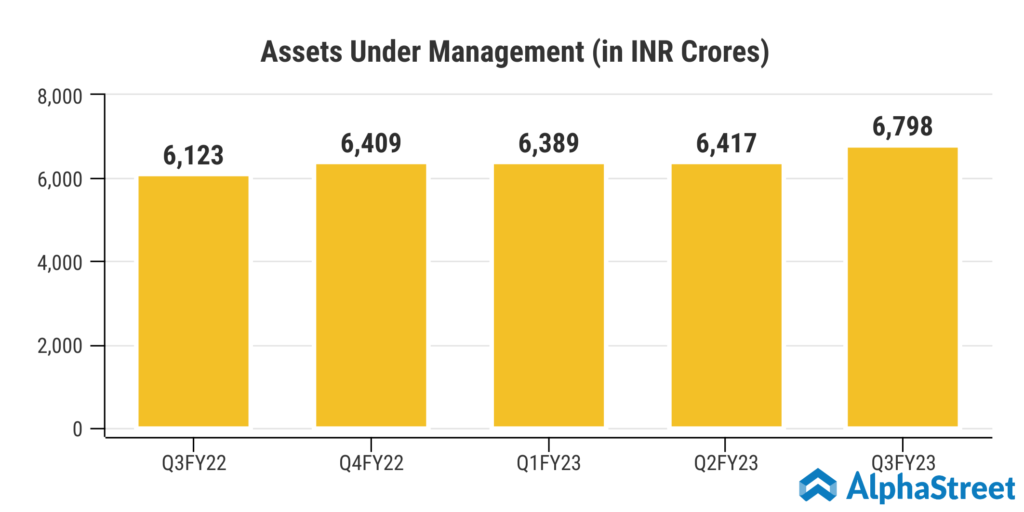

Currently, the company has a total of 31 Lacs+ active accounts to whom the company has disbursed loans to and the gross loan portfolio (GLP) stands at 7,650 crores.

Company’s Network:

SCNL is Headquartered in Gurugram, Haryana. Its operations are established across 23 states and union territories. The co. along with its 3 subsidiaries caters to 28 lakh customers through 1,214 branches and 30 lakh unique loan accounts.

Fundraising activities:

During FY22, the company delivered INR 225 Crores fundraising through the preferential allotment via the issue of equity shares and fully convertible warrants.

Pledged Shareholding:

The total promoter pledged shares stood at 2% in September 2022 compared to 44% in September 2018.

Financials:

What we like:

- Leading Microfinance company:

Satin Creditcare Network Limited has an established track record of operations of more than three decades in the finance industry and is among the largest players in the microfinance industry with a consolidated AUM of INR 7,569 crores as on June 30, 2022.

- Reducing dependence on any one state:

The company has been able to reduce revenue concentration across traditional areas. Since FY18, they have consciously brought down the share of the top 4 states from 68% to 54%. Likewise, their Average exposure per district also came down from 0.35% in 2017-18 to 0.25% in 2021-22. In accordance, the percentage of top districts to AUM came down from 19% to 14% for the corresponding period. By reducing their dependence, the company is reducing the risk of over exposure to any one state.

- The company is expanding its services:

Company is expanding into related businesses such as affordable housing finance, loans to individual businesses and MSME enterprises, etc. The company is expanding in these businesses through its wholly owned subsidiaries namely Taarashna Financial Services Ltd (TFSL), Satin Housing Finance Ltd (SHFL), and Satin Finserv Ltd.(SFL). During FY22, TFSL and SFL were merged together.

- The company leverages the use of technology:

The Company uses advanced technology for KYC, obtaining real-time user data through geo-tagging, cashless collections, digital payments, instant bank account verification, and more. By adopting digitalization, they have reduced the time taken for loan approvals and disbursements from 18 days to a few minutes. The company is also the first MFI to be certified with ISO 27001:2013.

- Diverse lending profile:

Satin Creditcare Network Ltd has a well-diversified funding profile comprising 59 active lenders as on June 30, 2022, with term loans from banks and non-banking financial companies (NBFCs)/financial institutions (FIs) accounting for ~44%, outstanding non-convertible debentures (NCDs) accounting for ~19% and securitization/assignment and other sources accounting for the balance (~37%) as on June 30, 2022.

Factors to consider:

- Competition from banks and fintech companies:

Banks and fintech players are targeting growth in the microfinance space as a part of retail outreach. This has led to competition intensifying in the microcredit space. However, large tech companies which have entered into the provision of financial services could potentially be another source of disruption to the financial services and poses systematic reach as stated by the RBI governor

- Over borrowing pattern:

Majority of borrowers depend on more than one lender such as local moneylenders, co-operatives, peers and relatives, and other informal financing channels. It is among the key reasons for loan defaults and thus, there is a need for stringent regulatory oversight.

- Political risk:

Microfinance comes under the purview of state governments. Since most of the rural MFI loans are given to economically backward strata of the society and also since they form a major chunk of voting population any impact on them can lead to heavy clamping down by the state govt. The AP microfinance crisis clearly shows how badly state government regulations can impact the industry in a state.

Industry Analysis:

The Indian microfinance industry plays a vital role in promoting inclusive growth by easing access to finance for those sections of the society underserved or unserved by formal banking channels. It has enabled last mile connectivity through its presence across India’s rural sector and serves as an effective channel for credit access to people from the low-income strata and those who are engaged in the informal sector.

MFIs are expected to witness a steady pick-up in loan disbursements driven by higher demand from low-income groups and small enterprises as they seek to reprise growth. ICRA expects the long-term outlook for the NBFC MFI industry to remain robust with near-term expectations of growth in Assets Under Management pegged at 18-22% during 2022-23. ICRA has revised the outlook for Non-Banking Financial Companies Microfinance Institutions (NBFC MFIs) from negative to stable with the expectation of steady growth in the Assets Under Management (AUM) and improvement in profitability.