“The Company’s plans, to be ready with emission efficient engines, to meet the BS VI.2 requirements applicable from 2023 onwards are well on track. The Company expects to have both Diesel and CNG variants of the appropriate engines, available to it to service various Vans, cross country vehicles and Bus platforms in time.”

– Board of Directors, Force Motors (Annual Report FY23)

Stock Data:

| Ticker | FORCEMOT |

| Exchange | BSE and NSE |

| Industry | Automobile |

Price Performance:

| Last 5 days | -4.4% |

| YTD | -21.73% |

| Last 1 year | +6.65% |

Company Description:

Established in 1958, Force motors is the flagship company of the Abhay Firodia group. The company is in the business of manufacturing fully vertically integrated small and light CVs, multi-utility vehicles, and agricultural tractors, which it supplies to various countries in the Middle East, Asia, Africa and Latin America.

Products:

The company manufactures engines, Transmission and axles, a range of small and light commercial vehicles (LCV), tractors and special utility vehicles (SUV). The major brands in its LCV and SUVs includes Trax, Traveller, Gurkha and Shaktiman while the brands in tractors include Orchard, Balwan, Abhiman and Sanman. The company’s Traveller and Trax brands are market leaders in their respective segments.

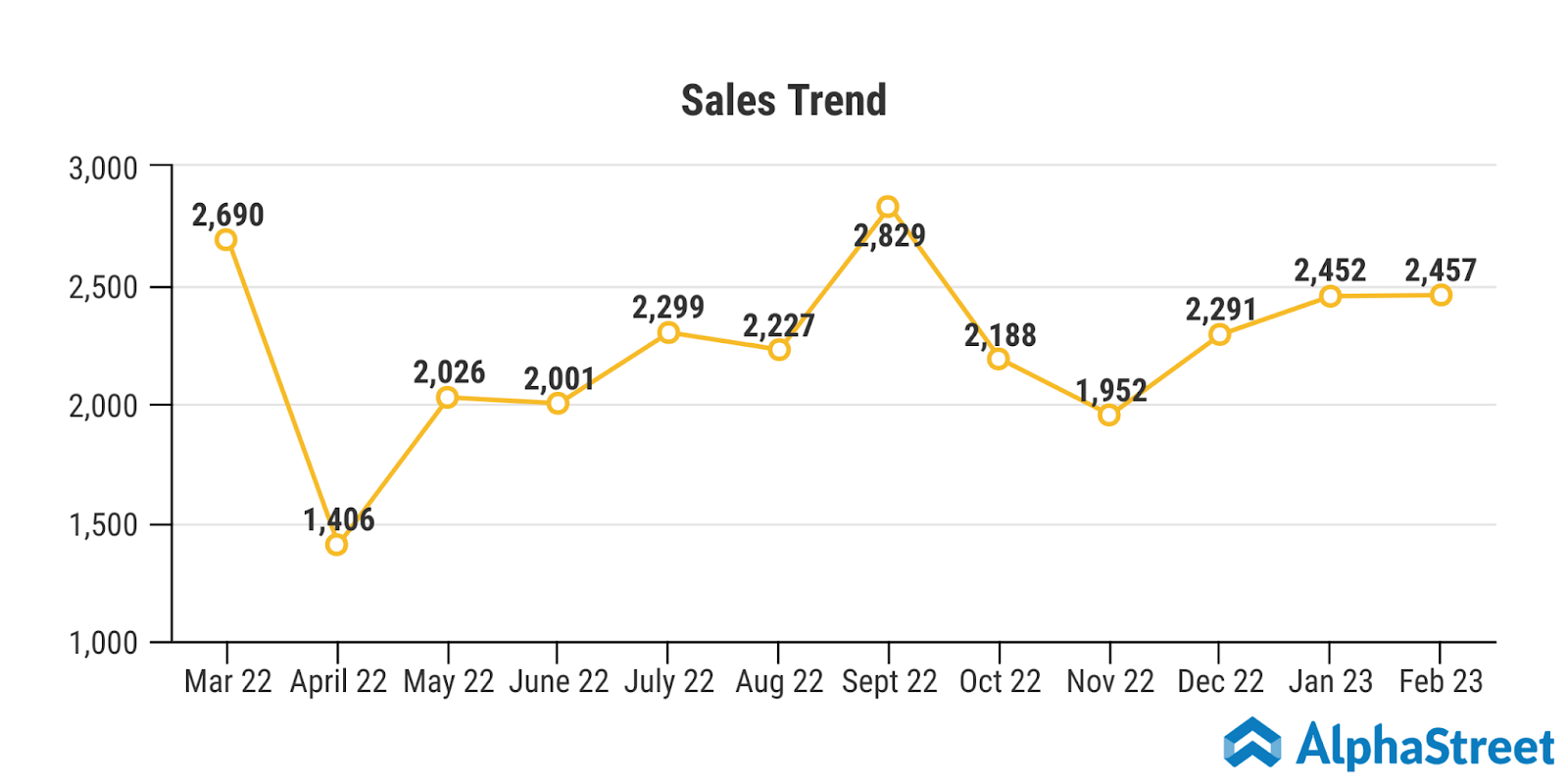

Sales Volume:

Post the launch of new products like Gurkha (5 seater) and Urbania, the sales volume increased by 18.5% in 2022 from the level of sales volume in 2021. In 2022, the company sold 24,351 units while that in 2021, the company sold 20,538 units.

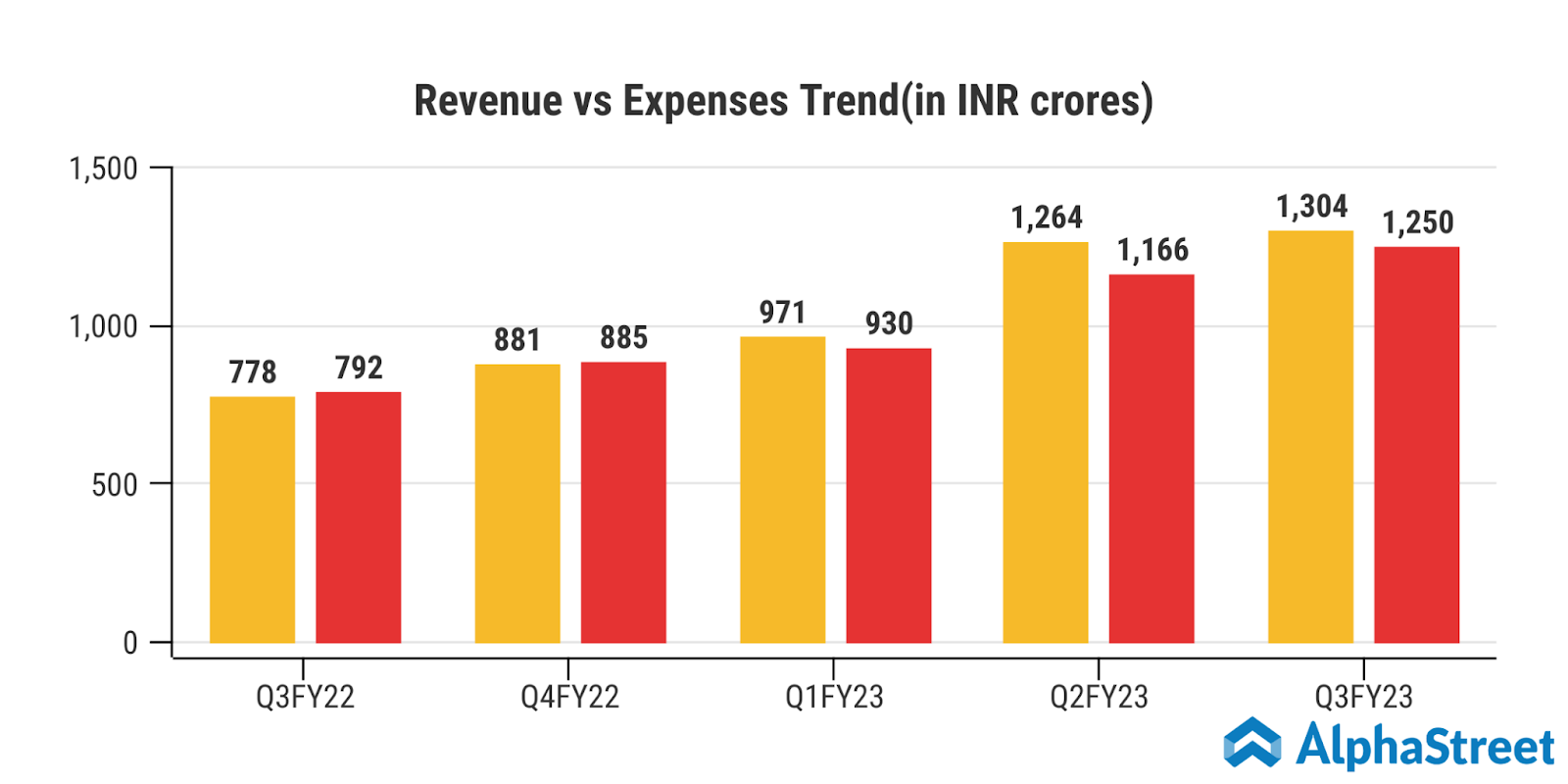

The demand for luxury cars(BMW, Mercedes) is rising thus Force is also showing improvement in its ancillary (engine) business. We can witness this as the topline increased QoQ in Q3 in spite of a fall in sales data by 10% QoQ).

Market Share:

The company’s market share of LCV in the passenger segment was 37.9% in FY20 while the market share of LCV in the school and ambulances segment was greater than 70% in FY20.

CAPEX Plans:

The company did an investment of over INR 1000 Cr and this was lined up for two models – Urbania (which is launched in Q3) and Traveller Electric variant (should be launched in FY24 hopefully). Urbania is a luxury-yet-affordable van and the company will be focusing on export markets with this model. Interestingly, here the margins might be superior to that of domestic exports.

What is good:

- Joint Venture with MTU (a subsidiary of rolls royce group):

The group entered into a joint venture with MTU Friedrichshafen GmbH (a company of the Rolls Royce Group) in FY18 to form Force MTU Power Systems Private Limited (FMTU) for engaging in the business of development, manufacture, and marketing of engines, engines for power generation, complete power generators and engines for various applications like Rail. Currently, it holds a 51% stake in FMTU, thus becoming a subsidiary of the Company.

This Joint Venture should cross sales of at least INR 300 – 400 Cr in FY24 with peak sales potential of INR 1000 Cr (Force has 51% stake in JV) – With increased localisation of RM content, EBITDA margins should be north of 14-15% in this business in a couple of years

- Collaboration with Mercedes and BMW will cater growth:

Force motors is the only company in the world that has collaboration with Mercedes and BMW to manufacture, assemble and test their engines. As the income group is rising and India is on its path to become a 5 trillion economy, the sales of such luxury cars is also increasing. This rise in sales can yield to the top line growth of the company.

- Electrification of vehicles will be a game changer:

The company will launch an electric version of its most coveted brand Traveler in FY24. This will help the company to benefit and improvise its margins due to reduced taxes on electric vehicles. This will also help the company gain a market share in foreign countries due to a limited availability of electric vehicles in more than 9 seaters segment.

What is bad:

- Apart from Traveller and Trax, no other brand has strong visibility among the customers.

- The company faces stiff competition from other brands like TATA, Eicher motors, Ashok leyland, Isuzu and Mahindra in the LCV segment.

- The company has faced many allegations from minority investors due to poor information disclosures. This can also be seen as the management does not conduct concalls, they further do not answer investor questions properly via mails.

- Increase in commodity prices can also hamper the growth of the company.

Conclusion and Industry Analysis:

A number of dramatic changes in the automotive world are happening. The pace of the change is much higher than was expected by most experts. Introduction of electrification of vehicles in India too is gaining traction at an impressive speed. While two wheelers, personal passenger cars etc. have seen impressive numbers of electric vehicles being demanded and produced, the change in commercial vehicles is significantly slower. However, availability of electric vehicles in the segment of Vans and Buses is inevitable and interesting.

However, extraordinarily high GST levels, particularly on the Van Segment of 10 to 13 seater vehicles, is an anomaly that defies logical explanation. Sadly, this fact which impinges on critical market segments such as Tours and Travels, School Buses, Business travel etc. has remained ignored by the Government. The collective impact of the GST and the State Government Taxes, aggregate to nearly 50% of the on road value of the vehicles. This, in most cases, is 5 times the earnings of the industry.

Though, the opportunity in India for successfully enlarging the Tour and Travel hospitality sector is a very substantial possibility to achieve high economic gains. The improving roadway infrastructure in India, the focus on connecting attractive pilgrimage centers, and tourist sites to the large and efficient grid of expressways and highways, will yield impressive results in the future. There is still a tendency to restrict Diesel vehicles in a number of inner cities even though they meet the mandated stringent regulations which are equal to internationally the best regulation. This is a damper on the image and sale of diesel passenger vehicles, particularly mass transport vehicles, such as Vans and Buses.