Stock Data:

| Ticker | NSE: ICICIBANK |

| Exchange | NSE |

| Industry | BANKING |

Price Performance:

| Last 5 Days | +1.72 % |

| YTD | +7.47 % |

| Last 12 Months | +11.37% |

Company Description:

ICICI Bank, a leading financial institution based in India, stands as a prominent pillar in the country’s banking landscape. With a steadfast commitment to innovation and customer-centricity, the bank has firmly established itself as a key player in the financial sector. Leveraging its extensive network, ICICI Bank offers a comprehensive range of banking and financial solutions to a diverse clientele, including individuals, businesses, and corporations. The bank’s strategic focus on risk-calibrated core operating profit, coupled with its relentless pursuit of technological advancement, ensures it stays at the forefront of digital banking innovation.

Critical Success Factors:

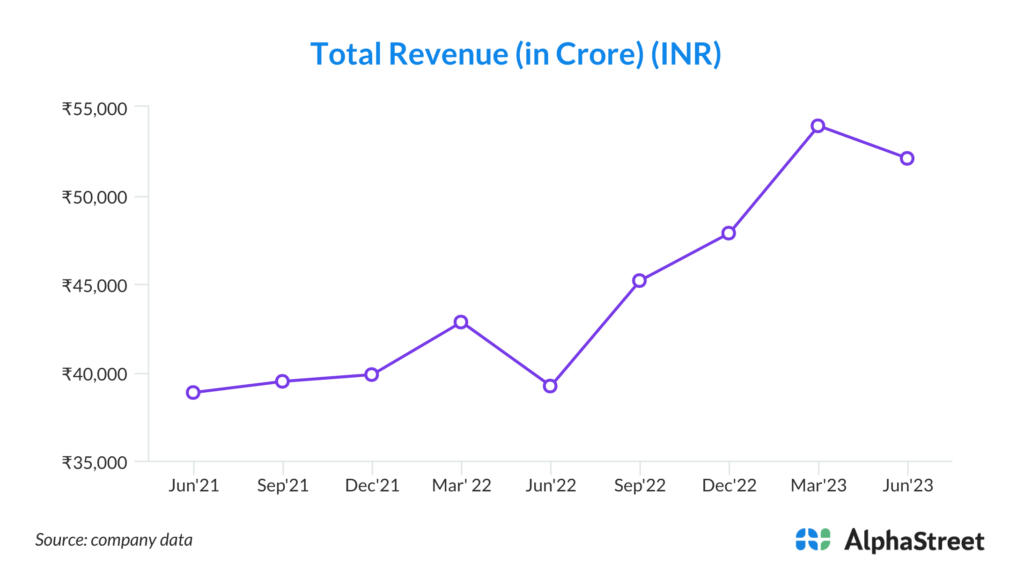

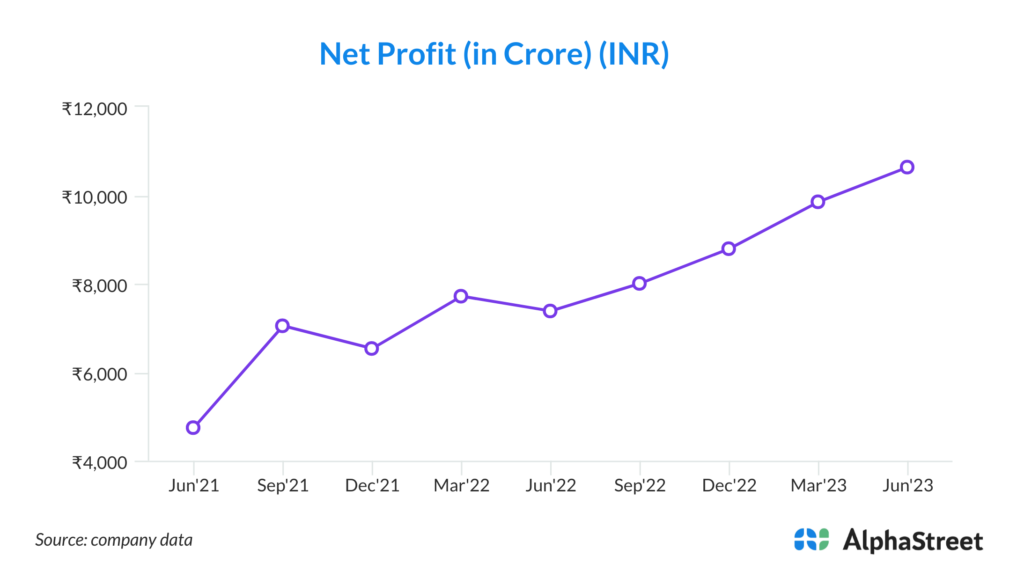

1. Robust Financial Performance: ICICI Bank has demonstrated impressive financial performance, with a consistent increase in key metrics such as profit after tax, core operating profit, and net interest income. The significant YoY growth in these areas indicates the bank’s strong operational efficiency and ability to generate substantial returns.

2. Asset Growth and Expansion: The bank’s consolidated assets have grown by 17.0% YoY, reflecting its successful efforts to expand its asset base. This growth indicates effective management of assets and a strategic approach to capturing opportunities in the market.

3. Strong Capital Position: ICICI Bank maintains a healthy capital adequacy ratio, with a total capital adequacy ratio of 17.47% and a Tier-1 capital adequacy ratio of 16.76%. This capital strength positions the bank well for future growth, risk management, and regulatory compliance.

4. Diversified Revenue Streams: The bank’s non-interest income, including fee income, has shown consistent growth. The fact that fees from retail, rural, business banking, and SME customers constitute about 78% of total fees underscores the bank’s ability to generate revenue from a diversified customer base.

5. Digital Innovation: ICICI Bank has made significant strides in enhancing its digital offerings and platforms. The creation of industry-specific digital solutions for corporate clients and the launch of various digital solutions for capital market participants showcase the bank’s commitment to leveraging technology to serve a wide range of customers efficiently.

6. Stable Asset Quality: The bank’s net NPA ratio of 0.48% on June 30, 2023, and a provision coverage ratio of 82.4% for non-performing assets indicate a well-managed and stable asset quality. This contributes to the bank’s overall financial stability and risk management practices.

Key Challenges:

1. Dependence on Economic Conditions: While ICICI Bank has showcased resilience in the face of volatile global conditions, its performance is still closely tied to the overall health of the Indian economy. Any significant downturn in economic growth could impact the bank’s asset quality, loan demand, and profitability.

2. Rapid Asset Growth and Quality: The bank’s aggressive asset growth might expose it to potential risks related to maintaining asset quality. Rapid expansion without adequate risk assessment and management could lead to an increase in non-performing assets, putting pressure on provisioning and profitability.

3. Interest Rate Sensitivity: The bank’s net interest margin (NIM) has fluctuated, indicating sensitivity to interest rate changes. The current and future changes in interest rates could impact the bank’s profitability, especially if loan yields do not adjust quickly enough in response to rising rates.

4. Dependence on Fee Income: While ICICI Bank has diversified its revenue streams with fee income from various customer segments, its reliance on fee income exposes it to changes in customer behavior, regulatory changes, or shifts in market conditions that could affect fee generation.

5. Digital Transformation Challenges: Although ICICI Bank has made strides in digital innovation, there are risks associated with the rapid adoption of digital platforms. Cybersecurity threats, technical glitches, or customer dissatisfaction with digital services could negatively impact the bank’s reputation and customer trust.

6. Regulatory and Compliance Risks: As ICICI Bank continues to expand and innovate, it faces an increased risk of regulatory scrutiny. Failure to comply with existing regulations or adapt to new regulatory requirements could lead to legal issues, financial penalties, and reputational damage.