Let’s start with a simple “What am I” type riddle – “Sometimes I stink. Sometimes I’m dirty. Yet everyone wants me.”

Now most of you might have thought about your favorite clothes or the loved ones but let’s cut it short – the correct answer is Money.

As we become mature, often an interesting question surrounds our mind as Why does a human civilization need a lot of money for? Well some do require it to fulfill their materialistic desires but a major chunk of the population need it to secure the future of their forthcoming generation. And thus in this pursuit, men buy land and women go for jewelries. But ever wondered that instead of dropping them a blessing, you are presenting them with a bane of illiquid assets, a lot of paperwork and of course who can forget the taxes! Well how about giving them an asset class that would yield much better returns and could be liquidated at a blink without much of a hassle.

Yes, we are talking about stocks and for this very purpose we have curated a list of top five stocks that you can present your future generation with. These stocks are selected on the basis of current valuation and analyzing the fundamentals. They represent various sectors that hold a good future and are on their path to create their own turnaround story.

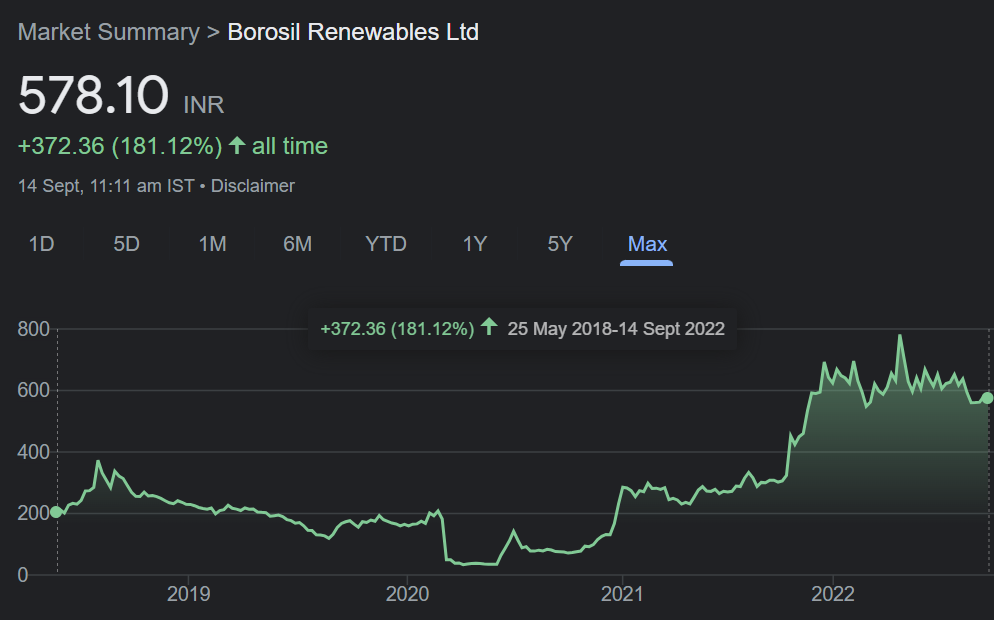

Borosil Renewables:

India is at the peak of solar revolution as the Union government intends to achieve 50% of its energy requirement from renewables by 2030. Borosil Renewables, being the only solar glass manufacturer in India with a market share of more than 40% attains a sweet opportunity to play the role of a big fish in this wide ocean. The company spotted the opportunity in the solar glass segment quite early and stationed its solar glass manufacturing facility in January 2010. Interestingly, the company supplies to 95% of the solar module manufacturers in India with no single customer being more than 3-5% of its total sales.

Considering the fact that switching suppliers in this niche requires testing and research, it will be difficult to break-in the Borosil’s market since they have always been in the learning phase for years. And new competitors will have to spend years learning the things that Borosil did in the past decade which gives the company, a bargaining power in hand.

Using relative and DCF valuation metrics we have come to the conclusion, the stock can witness a 20-25% upside till the next quarter results though in the long run, the stock can witness multiple folds given the economy shifting its gears towards solar energy.

CDSL:

Central Depository Services is the only listed entity of the two security depositories in India. The sector has been growing at a rapid pace ever since the Government made it mandatory for all securities trading to take place in the dematerialized (DEMAT) form. With the advent of Depository and Depository Participants like Zerodha, Upstox and Groww, it has become quite easy for retail investors to buy and sell shares online. As the Indian capital market is hugely underpenetrated with only 5% of the population holding DEMAT accounts, the number of retail participation will only go up which in turn would result in higher trading volumes and buoyant primary markets.

Further, the depository sector has a very strong entry barrier and being a platform driven business does not require much of CAPEX to operate. Unlike NSDL which focuses on FIIs and DIIs for its growth, CDSL is targeting retail investors which could translate into a network effect. And this growth can also be witnessed with numbers as the company has delivered an ROE of 17% and has compounded its profit by 15% over the period of 10 years. Astonishingly, being a completely debt free company, it has been generating robust ROCE consistently greater than the Cost of Capital over the past few years which results in positive cash flow. The company being the only listed player in this space could offer a scarcity premium to it going forward and at the present valuations is the best bet to buy.

Analyzing the past data trends, we can state that the company’s revenue is expected to be ~15% with an EBITDA margin of ~65% for FY24E. The revenue CAGR of 10% over FY22-24E assumes +36/0/2/-2% CAGR in issuer/transaction/IPO/KYC revenue. And hence, once can easily witness a more than 30% upside till the next quarter. For the long term, the stock is still trading at an effective valuation.

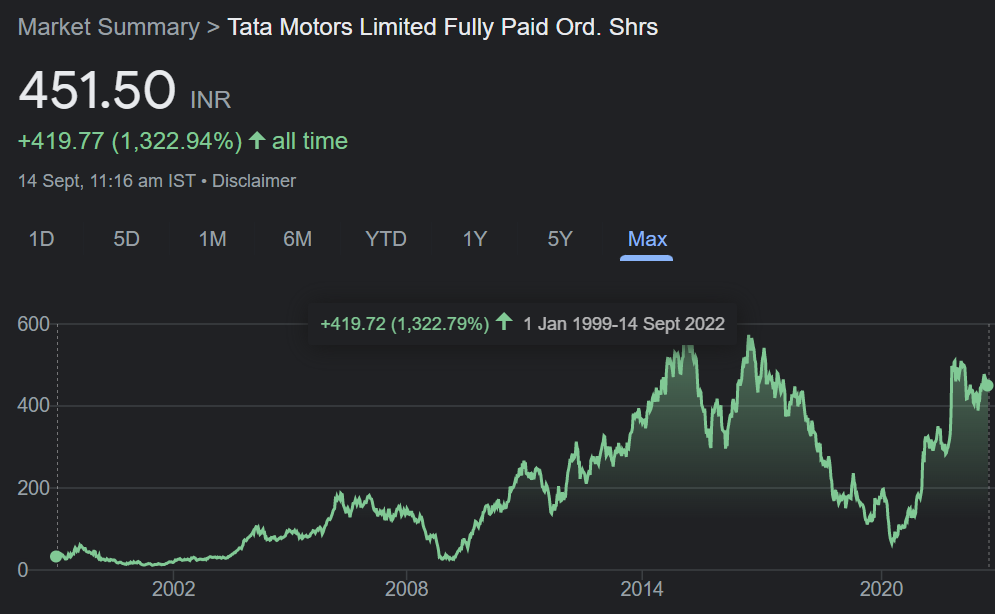

TATA Motors DVR:

TATA Motors is a leading global automobile manufacturer in India with a robust market share of more than 42% in the Commercial vehicle segment. With its subsidiary – Jaguar and Land Rover, TML has created news headlines in the global car market. And due to such international brands, the company has operations across the globe including UK, South Korea, Thailand and Spain.

TML has established an alliance with TATA chemicals, TATA Power and ELXSI to conquer the EV space in India. So, TATA chemicals on one hand is building energy storage systems for mobility and stationary charging facilities while on other hand TATA Power has already installed 170 charging stations in 20 cities across the country. Meanwhile TATA ELXSI is developing an IOT platform that would provide every automaker with a common stack.

With the market share of ~71% in the EV segment, the company has witnessed a whopping sales growth of 218% over the last year. No wonder, an early mover advantage in the EV segment in India has made the company regain its lost charm. The main concern for the company is its piling debt of 1.49 lakh crores which the company plans to resolve by 2025 (mentioned in the company’s annual report). With the ease of COVID norms and stabilization of the economy, the rampant sales of medium and heavy commercial vehicles would result in the positive financials of the company.

Using the SOTP valuation we came at an effective valuation of INR 646 per equity share which is trading again at a discount of ~40%. By witnessing the sales data trend of TATA motors, one can easily analyze the company on its turnaround phase and is beenficial to hold for long run.

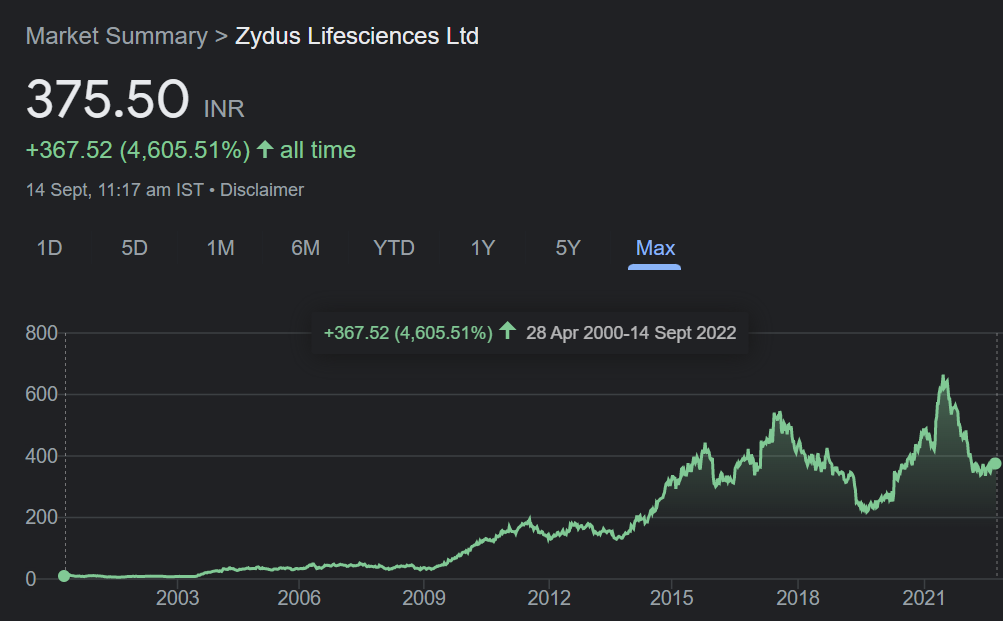

Cadila Healthcare (Zydus Lifesciences):

Being the fifth largest pharma company globally with nearly 70 years of business excellence, Cadila Healthcare has its presence across the pharmaceutical value chain of R&D, manufacturing, human and specialty formulations, APIs and consumer wellness products.

Not only this, but to cater the market completely, the company has a strong physician and retail network with established relations across India. Also, apart from core pharmaceuticals, it also has a consumer wellness division (Zydus Wellness) whose retail network was recently powered by the acquisition of Heinz India. With this strong network effect, Cadila can ensure the prompt availability of products.

Further, Cadila is the only Indian manufacturer of natural Streptokinase and Hyaluronic Acid products. While the former is used as a medication to clear clots in heart attack, lungs and arteries, the latter is used for skin treatment.

To shield its future, Cadila is planning to enter the complex injectables business in the US, a market poised to grow exponentially due to the rising threat of chronic diseases like diabetes. The global injectable business, which was a massive $483 billion market in

2019, is predicted to become thrice the size in less than a decade. Also, the company has significantly reduced its debts by more than INR 3000 Crores to nearly a fifth in just one year! This has helped the company improve its interest coverage ratio which has thus, contributed to its bottom line. Supported by robust financials Cadila has delivered a compounded profit growth of 12% and ROE of 22% over the period of last 10 years.

We value Zydus Lifesciences at INR 405 (base business of INR 381 at 16x P/E on FY24E EPS of INR 23.8 + NPV of INR 26.7 for gRevlimid opportunity). Though, this surely is a stock that you can hold in your portfolio if you are looking for a key player in the pharma sector at an undervalued cost for the long run.

Bharat Electronics:

This state-run defense equipment and electronics components manufacturer offers a direct play on India’s defense CAPEX. To boost its order inflows and revenues, the firm also takes contracts as a system integrator. Due to such a move, the order pipeline is expected to remain strong over the next few years.

The company has also piled itself into new ventures like Smart Cities and Homeland Security. With a robust balance sheet, near zero debt and a large stack of cash, cumulated with competitive advantages, the company is expected to drive higher profitability growth over the upcoming years.

Management has indicated revenue growth of ~15% with EBITDA margin of ~21-23% for FY23. Order inflow to come in at ~INR 200 Bn in FY23. Keeping the order book in mind we can expect an upside of 25-30% till the next quarter. Though defense as a sector holds a good potential in the future and hence we recommend you to bag this stock in your portfolio for future scenario.

Conclusion:

Though we have curated a list of fundamentally strong stocks, we hold conviction that these will generate multifold returns over the long run. However, investors need to be cautious and do their own research before investing.