“After a few quarters of ongoing pressure on input costs, we have been able to expand our Gross & EBIDTA Margins delivering 20% EBIDTA growth. Our strategic investments and Dermicool acquisition have performed well and contributed to this growth. We will continue to make significant investment behind our core brands, innovations, channel expansions and digital optimizations which are expected to contribute immensely to future growth”

Mr. Harsha V Agarwal, Vice Chairman and Managing Director

Stock data

| Ticker | EMAMILTD |

| Exchange | BSE and NSE |

| Industry | FMCG |

Price Performance:

| Last 5 days | -3.72% |

| YTD | -11.88% |

| Last 1 year | -9% |

Company description:

Founded in 1974, Emami Limited is a leading Indian FMCG company. The company is engaged in manufacturing & marketing of personal care & healthcare products with an enviable portfolio of household brand names such as BoroPlus, Navratna, Fair and Handsome, Zandu Balm, Kesh King, Zandu Pancharishta, Mentho Plus Balm and others. The company is headquartered in Kolkata, India, and has a presence in over 60 countries worldwide.

Geographical segmentation:

The company derives ~80% of the revenue from domestic market and 16% from International markets (vs 15% in FY20)

Multi-location plants:

Emami has 7 manufacturing facilities across India and one in Bangladesh. They also have third-party manufacturing tie-ups in Sri Lanka, the Middle East, and Germany.

Launch of New products:

Company has launched 40+ products in FY21 and with new products contributing 4% of revenues. They have also forayed into the home hygiene segment by launching several range of products under the brand ‘EMASOL’ for Disinfectant Floor Cleaner, Disinfectant Toilet Cleaner, Disinfectant Bathroom Cleaner, Antibacterial Dish Wash Gel, and an All-Purpose Sanitizer.

Key Acquisitions:

Emami has made two significant acquisitions in its history, it acquired Zandu Pharmaceuticals Works Ltd, the heritage brand manufacturer of Zandu for 730 Crores in 2008 and In 2015, it acquired kesh king for 1651 Cr.

In 2018, the company acquired a stake in Helios Lifestyle Pvt Ltd (30%, increased to 48.5% in August 2021) and Brillare Science Pvt Ltd (26%, increased to 66.29% in November 2021) in order to foray into professional salons and online male grooming segments.

Advertisement Expenses:

Emami spent Rs. 523 Cr (15% of its total revenue) for Advertisement and Promotion of its product which is one of the highest in the industry. Emami has pioneered the concept of celebrity endorsing in India and There have been more than 60 Celebrities ranging from the film industry to the sports personalities endorsing its products.

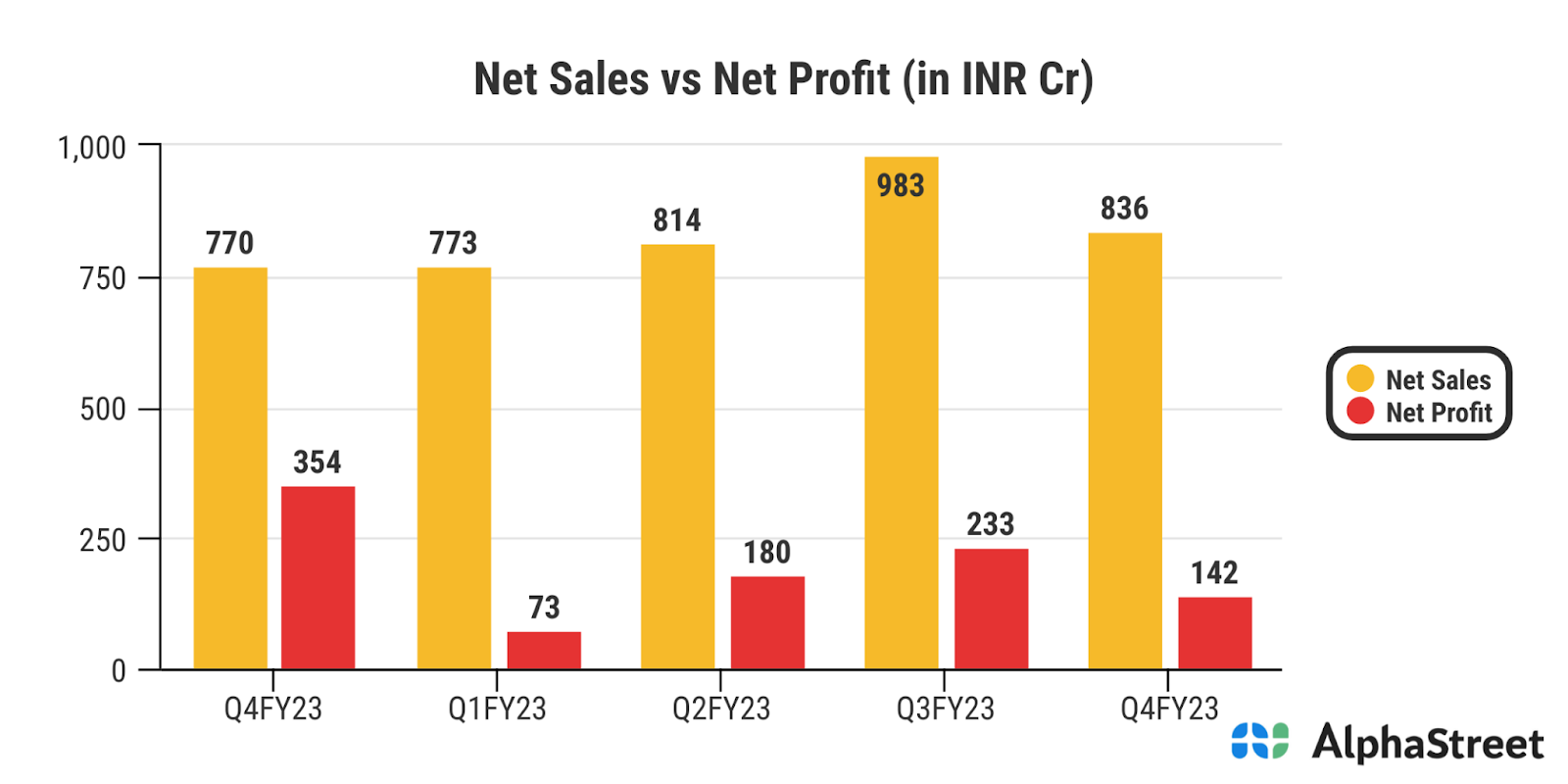

Financials:

What we like:

- Emami group is the parent company:

Emami was founded by two childhood friends in the 1970s and now the Emami group has grown to be one of the most successful business groups with its presence in diversified sectors such as FMCG, newsprint manufacturing and packaging boards, edible oil and biodiesel, real estate, hospitals, ballpoint tip manufacturing, retail, pharmacy chain and contemporary art. Certainly Emami Ltd is a part of that group and having a strong backing makes it a prominent player in the space.

- Leadership in Niche segments:

Emami is one of the leading companies in the personal and healthcare segment with leadership in the niche Ayurvedic segment. The Company has a portfolio of 300+ products based on ayurvedic formulations.

- Portfolio of Strong brands:

The Company offers a consumer portfolio of more than 9 brands and 13 sub-brands. The brands of Emami are a combination of the ancient Ayurvedic and modern science and 5 out of the 9 brands have been maintaining leadership across various segments.

| Brand | Category Size (in ₹ Cr) | Market Share |

| Navratna Cool Oil | 965 | 66% |

| Boroplus antiseptic cream | 681 | 68% |

| Fair and Handsome cream | 256 | 64% |

| Zandu and MenthoPlus Balms | 1515 | 55% |

| KeshKing Ayurvedic Oil | 922 | 29% |

| Dermi Cool | NA | 45% |

- Strong Distribution Network:

The Company employs more than 3800+ people, reaches out to 45 lakh plus retail outlets through a network of over 4600+ distributors and has invested in 7 plants, 4 regional offices, 1 overseas unit, 7 overseas subsidiaries, 24 distribution centers and 2 Associates across India.

The products of the company are sold in 60 countries across the globe and they have deep penetration across rural areas and their presence spread across 20,000+ Villages in India. They have more than 4600+ Distributors and their products are available in more than 4.9+ Mn outlets. The company claims that more than 150 of their products are sold every second in India.

- Strategic presence helps the company expand its reach:

The Company’s facilities are strategically proximate to resource points, consumption markets and locations, enjoying multi-year fiscal incentives. The Company has its own overseas manufacturing facility in Bangladesh and manufacturing tie-ups with contract manufacturing units in Sri Lanka, Germany, Thailand and UAE. The extension of manufacturing partnerships in UAE and Thailand has widened its flexibility to supply global pockets of emerging demand.

Factors to consider:

- The company has delivered a poor sales growth of 5.11% over the past five years. The sales growth in recent years seem low, so growth is slow.

- Diversification of the group in unrelated business like Realty, Hospital, which they are looking to dispose off. Though these don’t fall into Emami FMCG umbrella, it deviates the focus of the promoters from the core money making business. The promoter group also owns Emami East Bengal FC.

- High Promoter pledge: The promoter’s shareholding stays consistent around the 54% mark, but the promoters have pledged their shares.

Pre-2020, the promoters of the group had sold the cement business to Nirma group at a valuation of Rs 5,500 crore which helped them to reduce the ratio of pledge to around 45 per cent from 89.24 per cent earlier. In 2020, the promoter pledge was around 54%. The promoters had publicly declared that they wanted to reduce their pledge by selling some of the group’s non-core assets. This was visible in their pledge reduction to around 36%. However in the recent quarter, the promoter pledge has once again increased by 4% to 40% levels.

- Volatility in profit margin: Mentha oil and polymers, comprising half of the company’s raw materials, are crude-linked, exposing their prices to volatility making profit margins volatile.