About Company:

Founded in 1984 and headquartered in Hyderabad, India, Dr Reddy’s Laboratories (DRL) is India’s second largest pharma company by global revenues. With more than ~20,000 employees, 1,200 scientists, 350 Ph.D.’s and an amazing portfolio, the company has been known for its mind-blowing R&D. DRL offers a portfolio of products and services, including Active Pharmaceutical Ingredients (APIs), Custom Pharmaceutical services (CPS), generics, biosimilars and differentiated formulations.

The company operates as an integrated pharmaceutical player worldwide and functions through three business verticals namely – Global Generics, Pharmaceutical Services and Active Ingredients (PSAI), and Proprietary Products.

1. Global Generics:

In this segment the company manufactures and markets prescription and Over-The-Counter (OTC) drugs under its brand name or as a generic finished dosage with therapeutic equivalence to branded formulations. To tap in the future opportunity, the company is also engaged in the biologics business. The company benefits from its expertise in active ingredients, product development skills, a keen understanding of regulations and intellectual property rights & streamlined supply chain.

Top revenue contributors of the segment are nervous system drugs (14%), gastrointestinal (13%) & anti-infective (10%). In FY22, the company filed 7 new ANDA’s with the US FDA.

2. Pharmaceutical Services and Active Ingredients (PSAI):

The company is one of the largest manufacturers of APIs in the world. It works with several leading generic formulation companies in bringing their molecules first to the market. Its API development also helps its own generics business to be cost competitive and get to the market faster than competitors. During FY22, the company filed 139 DMFs worldwide, including ten in the US.

Interestingly, the company has one of the largest custom pharmaceutical services (CPS) businesses in India. It offers end-to-end product development and manufacturing services and solutions to innovator companies. During FY21, the company sold the contract development and CDMO division of the CPS business of the company. Top revenue contributors in the PSAI segment are cardiovascular (25%), anti-infective (~18%), and pain management (14%).

3. Proprietary Products:

In this business vertical, the company focuses on the research, development, and manufacture of differentiated formulations for dermatology and neurology therapeutic areas and engages in developing therapies in the fields of oncology and inflammation.

The company’s wholly-owned subsidiary, Aurgene Discovery is a clinical-stage biotech company that is working on bringing novel therapeutics for the treatment of cancer and inflammation. It has fully integrated drug discovery and development infrastructure from drug discovery and development infrastructure from hit generation to clinical development.

Geographical Revenue Breakup:

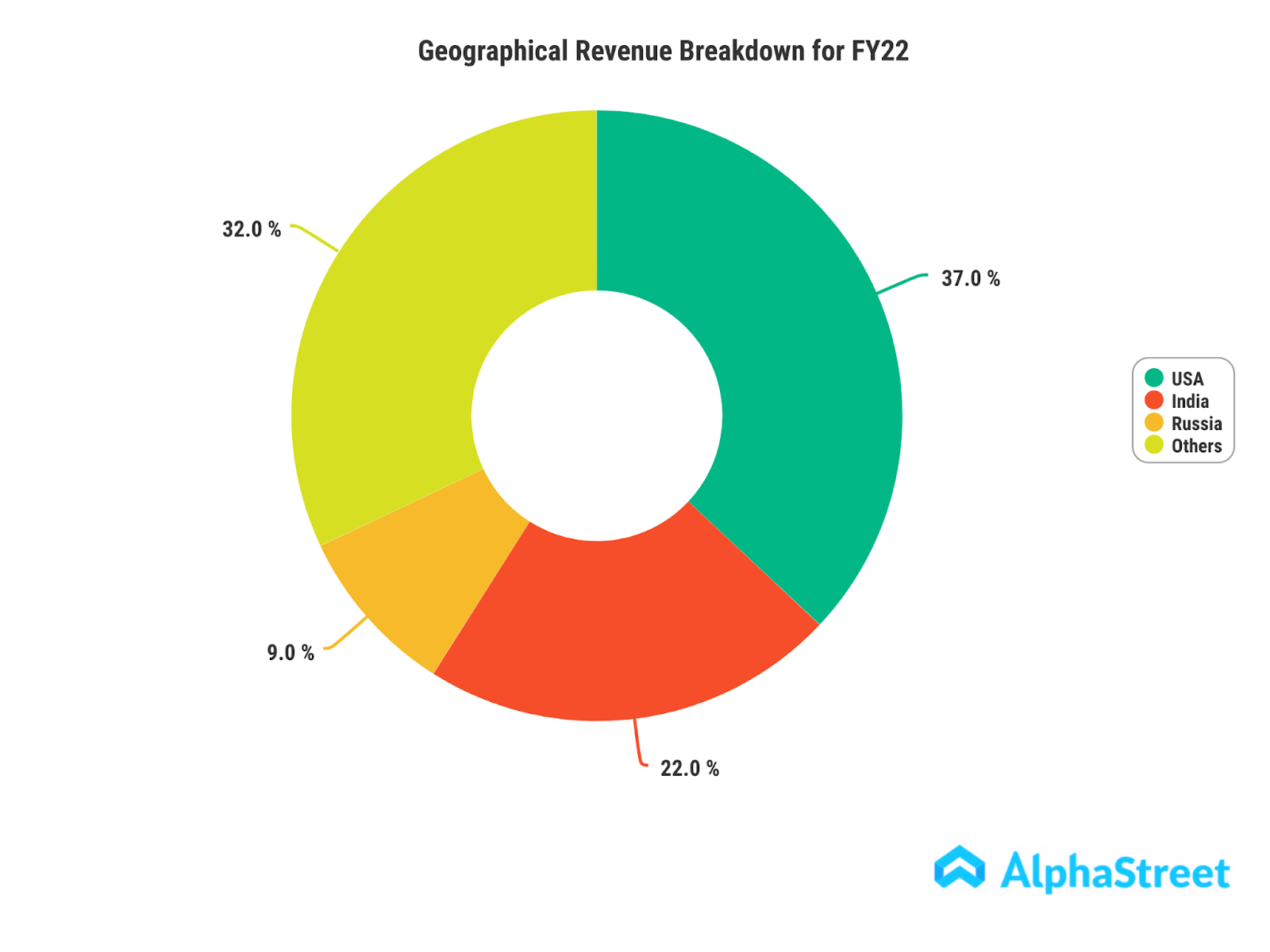

In FY22, USA accounted for 37% of revenues, followed by India (22%), Russia (9%), and others (32%).

Revenue Concentration:

Revenues from two customers of the Company’s Global Generics segment represent approximately 15% of the Company’s total revenues for the year ended 31 March 2022. This can be a good as well as bad point at the same time. If any of the customers walks away then the top line of the company will suffer.

R&D Capabilities:

The company has R&D operations through its 9 R&D facilities situated in India, the United Kingdom, Netherlands, and Malaysia. R&D used to be 5-7% of sales until FY13 which was then increased to 13% levels due to DRL’s foray into complex generics, new drug applications and biosimilar programs. The company’s R&D expenses as a percentage of total revenues has come down from 13% in FY18 to 8% in FY22.

Manufacturing Capabilities:

Presently, the company has 23 manufacturing facilities across the world. It has 9 manufacturing facilities for manufacturing APIs and 14 facilities to manufacture formulations. Its foreign manufacturing facilities are located in Mexico, United Kingdom, USA, and China.

Drugs for Covid-19

During FY21, the company partnered with various companies and organizations for the manufacturing of various Covid-19 treatment drugs such as Remdesivir, Avigan, Molnupiravir, Baricitinib, and various other crucial drugs used to treat COVID 19. During FY22, the company launched the Sputnik-V vaccine for COVID-19 in India.

Divestment

To focus on core business and growth brands, the company divested some brands belonging to Proprietary Products, DRL sold their US and Canada territory rights for ELYXYB (Celecoxib oral solution) to Bio-Delivery Sciences during FY2022, for a consideration of 110 crores.

Acquisition of product portfolio:

On June 24, 2022 – Dr. Reddy’s Laboratories along with its subsidiaries together announced that it has acquired a portfolio of branded and generic injectable products from Deer Park, Illinois, based on Eton Pharmaceuticals. With an upfront payment of $5 million in cash, plus contingent payments of up to $45 million. The acquisition supports Dr. Reddy’s efforts to accelerate and expand affordable medications for patients.

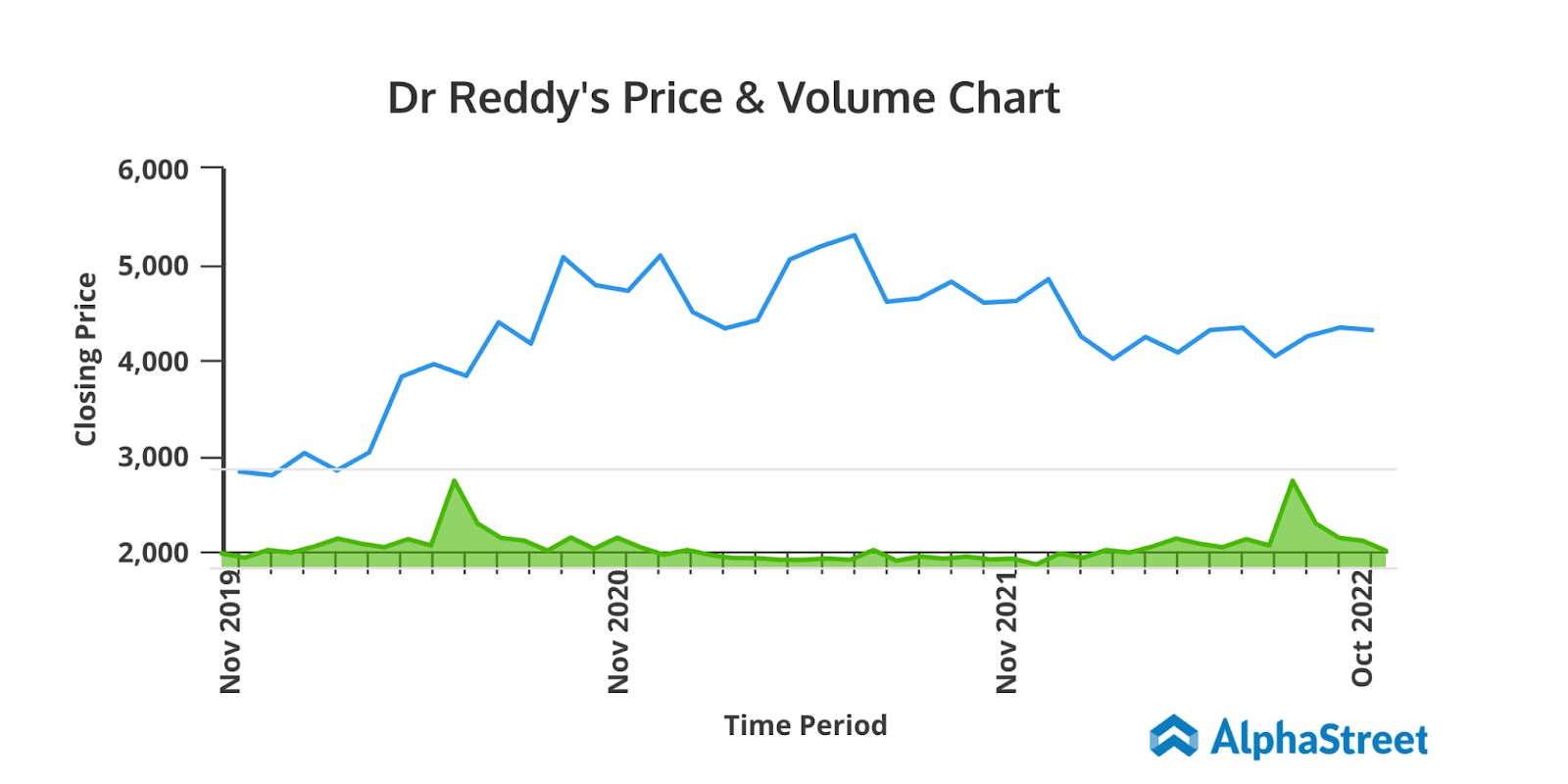

Share price insight:

- With the current price of INR 4,376 as of October 20, 2022, DRL is hovering in the mid range of its 52-week range of INR 3654 – INR 5010.

- The stock price has generated a CAGR of 19% over the period of last 3 years.

- The stock recorded a 5-year positive return of 81.21% as compared to the Nifty Pharma return of 40%.

Financial Snapshot:

| FY13 | FY14 | FY15 | FY16 | FY17 | FY18 | FY19 | FY20 | FY21 | FY22 | |

| Revenue | 11,833 | 13,415 | 15,023 | 15,568 | 14,196 | 14,281 | 15,448 | 17,517 | 19,048 | 21,545 |

| Expenses | 9,164 | 10,164 | 11,515 | 11,983 | 11,724 | 11,930 | 12,270 | 15,040 | 15,173 | 17,778 |

| Net profit | 1,527 | 1,963 | 2,336 | 2,131 | 1,292 | 947 | 1,950 | 2,026 | 1,952 | 2,182 |

| EPS | 89.9 | 115.41 | 137.13 | 124.88 | 77.96 | 57.07 | 117.42 | 121.92 | 117.35 | 131.14 |

The company has generated a sales growth of 12% CAGR over the period of 3 years while the profit growth has been 5% CAGR during the same period. But a trivial question arises as to why the company delivered a muted performance between FY15 to FY18?

The reason behind muted performance between FY15 to FY18?

During this period, the mainstay business of the company came under pressure, so DRL started focusing on creating a branded (specialty) portfolio of products in the USA. By doing so, DRL had stepped into an uncharted territory and faced high investments, long gestation periods, and challenges in gaining meaningful market share issues.

DRL was mainly facing two issues – Capital allocation and execution.

- Capital Allocation: Prior to FY18, the company was playing high risk and high reward kind of strategy. They did a significant chunk of capital allocation to the United States and were focused on relatively small numbers of assets with complex generics, specialty products and biosimilars. Unfortunately, this strategy yielded them more risk and very less rewards.

- Execution issues: During this moment, USFDA presented major compliance issues and all the pharma companies were not performing well.

So what changed after FY18?

DRL promoters (Reddy and Prasad) hired Erez Israeli in early 2018 as COO and Global Head of Generics & PSAI role. Israeli’s long stint of 23 years with Teva had prepared him well for the job at DRL. Since his joining, DRL has been on a transformational journey (almost 4 years now). Erez is promoted to CEO in mid 2019.

Now, here are the strategies implemented:

- Created more opportunities and addressed more potential space and value with less risk.

- Earlier it used to develop for the U.S, Now it has been developing for every country potentially in the world. For the same products, DRL has now, not one market, but more than one market.

- Synergy integration between its spaces: Earlier in API, the company had some third-party sales, some back integration, however relatively low level. Now after increasing the API capabilities, it focuses to get more third-party sales while increasing the backward integration (to safeguard and benefit from the changes in China)

- DRL had good specialty products, but did not have an adequate go-to-market in the United States. Now it gives these products to partners in return of upfront and royalty payments; low risk approach. Indirectly helped to pay most of the debt.

- Focused on being more efficient, better execution, got rid of stuff that it should not have been in and further changed the priorities.

Q1FY23 Results:

Revenues grew 6% YoY to INR 5233 crore, driven by 26% YoY growth in India to INR 1334 crore. Russia & Other CIS markets grew 4% YoY to INR 510 crore while Europe also grew 4% YoY to INR 414 crore. US markets grew by 2% YoY to INR 1781 crore while RoW markets de-grew 8% YoY to INR 390 crore. PSAI segment posted de-growth of 6% YoY to INR 709 crore. Revenues for Q1FY23 includes License fee and service income of INR 90.2 crore from sale of brands to JB Chemicals and INR 139.9 crore from sale of brands to Torrent Pharma. Gross margins declined 210 bps YoY to 63.5% and EBITDA margins improved 313 bps to 18%. Adjusted EBITDA margins for one-off divestment income was at 14.2%. Subsequently, EBITDA grew 28% YoY to INR 941 crore. PAT for the quarter was up 224% YoY to INR 1180 crore.

Factors to consider:

- Long gestation period on R&D Projects:

R&D projects involve longer development time and medium to high investment as is the norm in the vaccine and pharmaceutical industry. As a result of this, the present profitability is affected whereas the output may come in medium to long term future periods

- Adverse currency movements particularly in Emerging markets may affect the bottom line of the company.

- Regulatory developments might hamper the sale of the company’s products.

- In lieu of chasing the short term numbers, the company might lose its long term plot.

Recent Highlights:

- US business: Increased competition in key products like gSuboxone and price erosion of 7-8% led to decline. LAunched seven new products in this quarter and guided to launch 25 products in FY23.

- Europe: During Q1, a total of nine launches in various geographies. Gross margins were in-line with previous years.

- India: Adjusted for brand divestment in current quarter and Covid sales in Q1FY22, growth was in double digits but on adjusting for acquisitions, base business grew in single digits in Q1FY23. Company launched 5 products.

- Completion of FDA inspection at new sterile injectable facility will support further approval in the future.

- Domestic formulation growth was in single digit adjusted for brand divestment, Cidmus acquisition and COVID

- Margins should improve in coming quarters as revenues pick up and normalization of expenses

- gRevlimid launch in Sept 2022 with volume restrictions and will be across strengths

- Maintained guidance of achieving 25% OPM.

- Healthy cash inflow to be utilized for future business growth through inorganic opportunities

Key Triggers for future price performance:

- US pipeline: In near term, key launches in complex generics (guidance for 25 launches in FY23) is likely to weather persisting price erosion in US, along with additional impetus from gRevlimid in H2FY23. Structurally, 1) 40% of pipeline being injectable/sterile, 2) 25+ complex products and 3) Select Biosimilars and Complex generics bodes well for the US market.

- Emerging Markets & India: New launches to offset price erosion and loss in Covid opportunities. Domestically, ramp-up of acquired assets and faster integration to increase base business.

- Easing of volatility in currency for Russia-CIS market and possible gains from inventory normalization in H2FY23.

- Target to backward integrate 70% molecules to benefit gross margins in the medium term. Immediate focus on cost rationalization, on SG&A front and simultaneous launches across geographies

Industry Analysis:

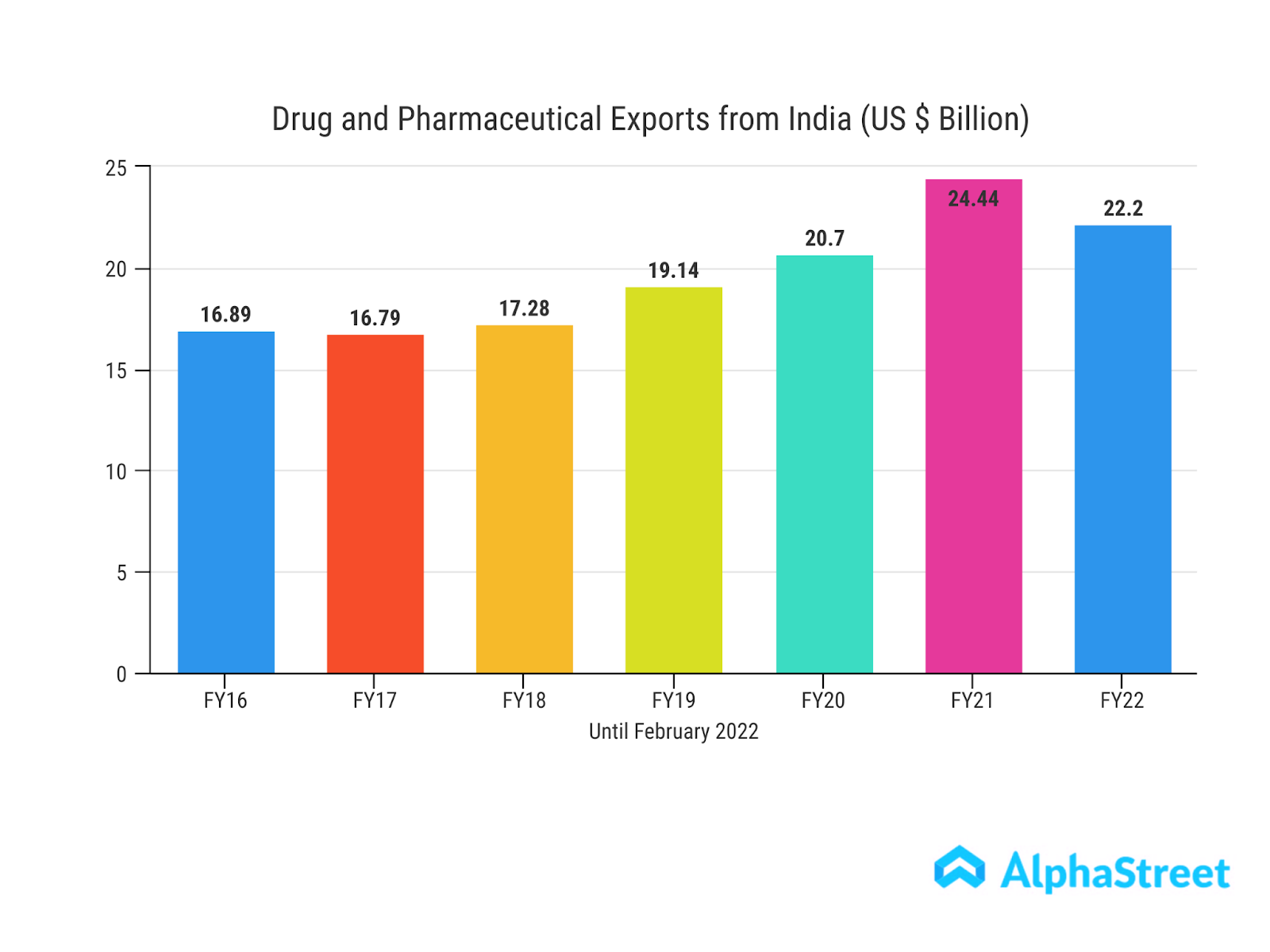

India enjoys a key position in the global pharmaceutical industry. It is the world’s largest supplier of generics, accounting for 20% of global exports and supplies over 40% of the demand for generic products in the US. India ranks 3rd worldwide for pharmaceutical production by volume and 14th by value. The country has an established domestic pharmaceutical industry, with a strong network of around 3,000 drug companies and ~10,500 manufacturing units. Indian pharmaceutical exports stood at US$ 24.44 billion in the financial year 2020-21 and US $22.21 billion in the financial year 2021-22 (until February 2022).

According to the Indian Economic Survey 2021, the domestic market is expected to grow 3 times in the next decade. India’s domestic pharmaceutical market stood at US$ 42.0 billion in 2021 and is likely to reach US$ 65.0 billion by 2024 and further expand to reach ~US$ 120.0 billion by 2030.

Currently, India is currently among the leading producers and suppliers of vaccines globally. It represents about 60% of the total vaccines supplied to UNICEF and over 50% of global demand for vaccines. The Indian vaccine market attained a value of ~INR 95.0 billion in 2020. The market is further expected to grow at a CAGR of 18% to reach a value of approximately INR 256.5 billion by 2026.

The future growth of the pharma industry will be mainly driven by areas like immunology, oncology, cardiology and neurology which are the fastest-growing therapeutic areas at present and will continue through 2026. The biologics market is growing at a significant rate and is expected to continue outstripping that of small molecules in the coming decade. The three largest biologic therapy areas include oncology, auto-immune and diabetes.

Further, an ageing population in many developed markets will create increasing demand for over-the-counter (OTC) medicines, generics and branded pharmaceutical products. In particular, demand for chronic disease medicines will grow in the mid and long-term. Pharmaceuticals demand in emerging markets is set to increase due to improvements in healthcare systems and growing disposable household incomes.