Cipla is an Indian multinational pharmaceutical company. The company was incorporated in the year 1935. The founder is Khwaja Abdul Hamied. Cipla has its headquarters in Mumbai. The company has extended its business worldwide. The presence of this company is marked in Australia, Europe, Kenya, Malaysia, Morocco, Nepal, South Africa, Srilanka, Uganda, United Kingdom & USA.

The company was initially incorporated with the name ‘The Chemical, Industrial & Pharmaceutical Laboratories’. However, in the year 1984 on 20th July the company underwent a name change to “Cipla”. The products offered include Generics and Branded Generics, Specialty, Consumer Health and Over-The-Counter range. The mission of this company is to be “a leading global healthcare company which uses technology and innovation to meet the everyday needs of all patients.”

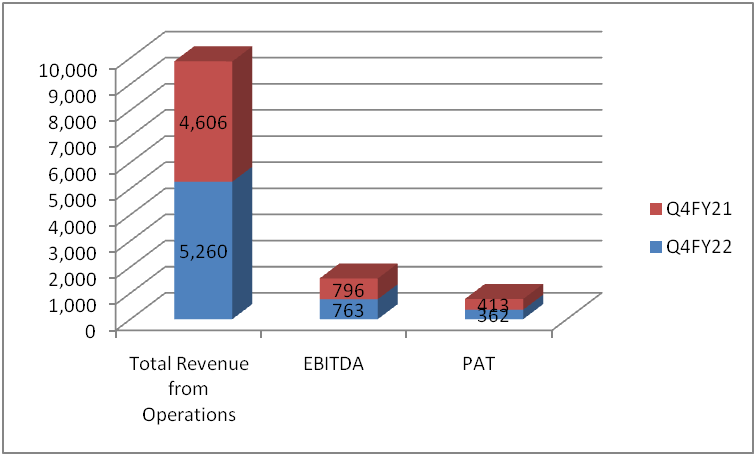

Financial Snapshots (In Rs Crores)

For Q4 FY 2022 revenue increased by 14% Y-oY to Rs. 5,260 crores. Total expenses increased 12.3% to Rs. 2,364 crore on a sequential basis. The employee cost for the quarter stood at Rs. 892 crore, which increased by 2.3%. R&D, regulatory, quality, manufacturing and sales promotion increased by 19.4% to Rs. 1,471 crore. Total R&D for the quarter is at 6.1% or Rs. 322 crore. Reported EBITDA for the quarter stood at Rs. 763 crore, or 14.5% of sales. Tax charge for the quarter stood at Rs. 71 crore. Profit after tax (PAT) is 6.9% of sales or Rs. 362 crore. The adjusted PAT, stood at Rs. 610 crore or 11% of sales. For FY 22 , Revenue increased by 14% Y-o-Y to Rs 21,763 crore. EBITDA margin stood at Rs 4,578 crore or 21.0% of Sales.

Business Portfolio

The portfolio of Cipla can broadly be classified into Cipla Therapies, Cipla Generics, OTC- Cipla Health, Cipla Diagnostics and API.

Cipla Diagnostics- Cipla Diagnostics worked very hard during COVID-19 pandemic. It distributed COVID-19 test kits across the nation through its established distribution capabilities. The test kit includes CIP Test, CIP test Plus& ViraGEN.

Cipla Therapies-Depending on the nature of the disease, Cipla has introduced ground breaking therapies for patients to give them a new beginning. It includes therapies for Oncology, Asthma, COPD& HIV.

API- Cipla has initiated API process development at three locations in India, with focus on organic chemistry, process engineering and analytical development at multiple locations. The API still have lots of product in their pipeline, which include Oncology, Hepatitis C, ARV, Diabetology, CVS, CNS, Respiratory.

Cipla Generics- It started business in the year 1999. It has achieved a milestone of 14 million. The focus of this product is to reach every household in India and serve the customers better. Cipla’s generics portfolio consists of medicines for acute and chronic therapies, anti-infectives, respiratory care, anti-ulcerate, cardio-Metabolic, pain & fever management, and vitamins & supplements.

OTC- Cipla Health- On the basis of market research, consumer preference Cipla has come forward with OTC products, which include Nicotex, Cofsils Lozenge, Cofsils Cough Drops, Cofsils Cough Syrup, Cofsils Experdine Gargle, MamaXpert, Prolyte Ors Unobiotics, Maxirich, Nicogum, CipHands, CLOCIP, Naselin, Cipladine.

Business Outlook-The Companyanticipates upcoming complex launches in the second half of this fiscal year. It wants to focus on respiratory filings and launches across geographies to accelerate our global lung leadership journey.Cipla is also gearing up for its new launches for FY23.It is working with USFDA on gAdvair. Initiated clinical trials on a respiratory asset.

SWOT Analysis

Strength- The company has a strong portfolio with diversified products which include generic, Consumer Health, Specialty and API. The company has expanded itself worldwide. Cipla has prioritized itself in new drug development. The products are well recognised by regulatory authorities of India, USA, Germany and the UK etc.

Weakness-Revenue is solely dependent on India. Rivalry from other pharmaceutical firms. The company has to incur a huge expense in R&D. It has a limited market share due to high competition from local as well as multinational pharmaceutical companies.

Opportunity- The company is constantly expanding in the domestic and international markets. It is focused on developing new products. It provides a wide range of ARV products for treatment of HIV for both children and adults. It should focus more on expansion especially in the emerging markets.

Threat- Different government policies impacting the business. Exchange fluctuation due to international operation. Intense competition due to the entrants of new pharmaceutical companies. The government has influence over pricing of a drug through national health organisations which is impacting the Pharma industry as a whole.

Industry Analysis– By 2023, the global pharmaceutical market is expected to exceed USD 1.5 Trillion. India has a key position in the global pharmaceutical industry. India is the world’s largest supplier of generics, accounting for 20% of global exports. Cipla is one of the pharmaceutical firms which has marked its presence within the Indian Pharmaceutical Industry. As of 2020 Cipla Limited had coverage of over 64 percent in the Indian pharmaceutical market. Cipla stands as the fourth-largest in the top ten list of Pharma companies in India. It has a debt Equity ratio of 0.23 and Price to book value of 2.20.

Comparative Study

| Companies | P/E ratio | EV/EBITDA | ROCE | ROE | Debt/Equity | Market Capitalization( RsCrore) |

| Cipla | 37.95 | 17.46 | 12.50% | 10.10% | 0.18 | 62,475 |

| Aurobindo Pharma | 15.77 | 9.69 | 18.80% | 18.50% | 0.33 | 46,916 |

| Lupin | 0 | 18.69 | 6% | -2.10% | 0.51 | 45,370 |

| Abott India | 52.83 | 34.99 | 36.50% | 27.10% | 0 | 34,675 |

From the investors perspective if we make a comparison between these pharmaceutical companies we will observe that though Cipla has more market capitalization, in terms of ROCE and ROE it will be less preferable. However the company maintains a healthy debt equity ratio still Abott India will be a better choice for any investor.

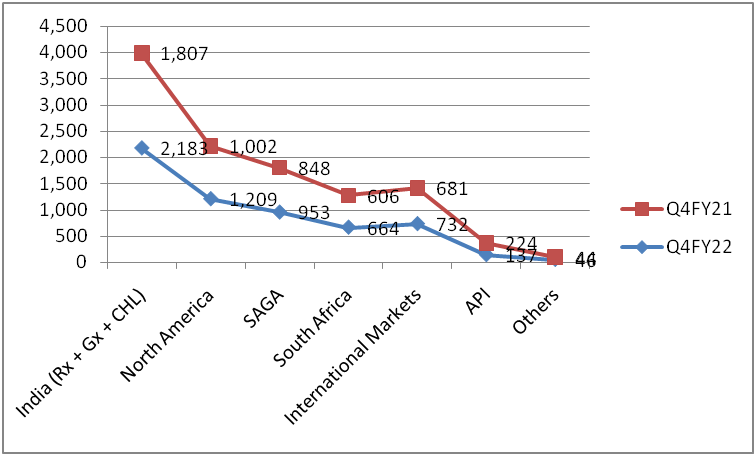

Segment Analysis(In INR Crores)

The business in India grew 21% Y-o-Y in branded prescription, trade generics and consumer health. The COVID portfolio grew 15% Y-o-Y basis. In case of SAGA region the business grew 8% on a YoY basis. This region has successfully maintained leadership positions in key therapy areas. In North America the revenue grew 17% Y-o-Y to $160 Million. The international market grew at a steady double-digit growth in secondary terms during the quarter. The API sector has declined to Rs 137 crores compared to the performance in the last quarter.