Stock Data:

| Ticker | Care Ratings Limited |

| Exchange | BSE and NSE |

| Industry | Credit Rating Agency |

Price Performance:

| Last 5 days | -3.4% |

| YTD | -14.7% |

| Last 12 months | -18.99% |

Management Commentary:

India’s economy is recording relatively healthy growth even in midst of the global headwinds. However, we need to be cautious given the strong interlinkages of the Indian economy with the global economies. While the global demand is slowing down, the most crucial aspect would be for the domestic demand to continue recovering. With the deleveraging in the last few years and rising capacity utilisation level, we can expect the private capex cycle to pick up in the next few months.

– Mehul Pandya, MD & CEO, CARE Ratings Ltd

About CARE Ratings Ltd:

Established in 1993, CARE Ratings is a leading credit rating agency of India that enjoys over a 30% market share. The Company provides various credit ratings that helps corporates to raise capital for their various requirements and assists the investors to form an informed investment decision based on the credit risk and their own risk-return expectations.

Their ratings directly affect the interest rates that are being charged on bank loans or issued bonds. These ratings differ from AAA to BBB and even lower which directly affect the implied interest rates anywhere from 6 to 10 %. ‘AAA’ means a borrower can sufficiently repay its debt whereas ‘BBB’ means the company can barely make their timely payments. Better the rating – lower the interest rate on borrowings and vice versa. Being a full-service rating agency, CARE has developed various products apart from debt ratings such as Infra ratings, MFI Grading, Real Estate Star Rating, Edu-Grade, REIT Rating, RESCO Grading, ESCO Grading, IPO Grading, ITI Grading, Shipyard Grading etc.

Promoter’s Shareholding:

| Investors (in %) | June 21 | Sept 21 | Dec 21 | Mar 22 | June 22 | Sept 22 |

| FIIs | 23.52 | 21.13 | 23.18 | 25.74 | 17.47 | 18.14 |

| DIIs | 18.47 | 17.89 | 16.10 | 14.52 | 21.53 | 24.88 |

| Public | 58.01 | 60.98 | 60.72 | 59.74 | 61.00 | 56.99 |

Reason behind choosing this business:

Credit rating business has fantastic economics as they enjoy robust operating margins at 65% consistent and return on equity of about 30%. Return on capital employed is at an average of 30%. Though if you notice the P&L statements and balance sheets, you would find it declining due to the economic slowdown and less amount of debt being raised in the market. Interestingly, the business requires no debt. The only expense on their books is qualified personnel. Moreover, the company has been paying out half of their earnings through dividends with an average dividend payout ratio close to 50%. There are very few businesses on the planet that enjoy such good economics.

The sales growth has been low in recent years. The main driver for this business to grow is with increment in borrowed money. There are two major ways credit growth takes place – increased borrowing from banks and corporate debt i.e. issued bonds. Credit growth is also related to the GDP growth of the country. Statistics show that credit offtake is 1.5-1.7 times the GDP of the country. At the current GDP of ~8%, one can witness a 12-15% growth in the overall corporate debt issued in India.

An interesting caveat of this business is the contractual nature of rating assignments. Clients are required to continuously cooperate with the same rating agency for carrying out a review of ratings. Thus, they are required to pay a surveillance fee on an annual basis. Credit rating assigned correlates with the risk weightage to the bank loan and/or bonds issued. Higher the risk weightage – higher the interest rate and vice versa. In case of an unrated borrower, RBI had earlier stipulated a risk weightage of 100%, however for BB or lower rating, risk weightage was 150%. Hence many borrowers whose rating deteriorated from BBB to BB did not share information with the rating agency due to which their rating got suspended. Thus, they were classified as unrated and got better risk weightage of 100% as against 150%. Under the new rule from RBI – the corporates which got rating suspended would immediately carry risk weightage of 150-200% depending on the last rating. Hence there would be no incentive for the borrower to get the rating suspended. If anything, unrated borrowers will try to get rated to have lower interest and better incentives on their debt. Thus, recurring revenue is going nowhere!

Warren Buffet and other value investors often encourage us to find a business that has deep moats. Rating business is certainly one of them that imposes a high entry barrier which is the reputation of the established players. In India, there are only 3 main players CRISIL, CARE & ICRA that hold 95% market share. Not long ago, CARE became the second largest player surpassing ICRA. There are 3 more agencies that were formed recently but it will take a lot of time for them to gain such a big market share. Interestingly, CARE has the best margins among industry which is due to low employee costs and higher productivity per employee.

CARE Ratings Operational side:

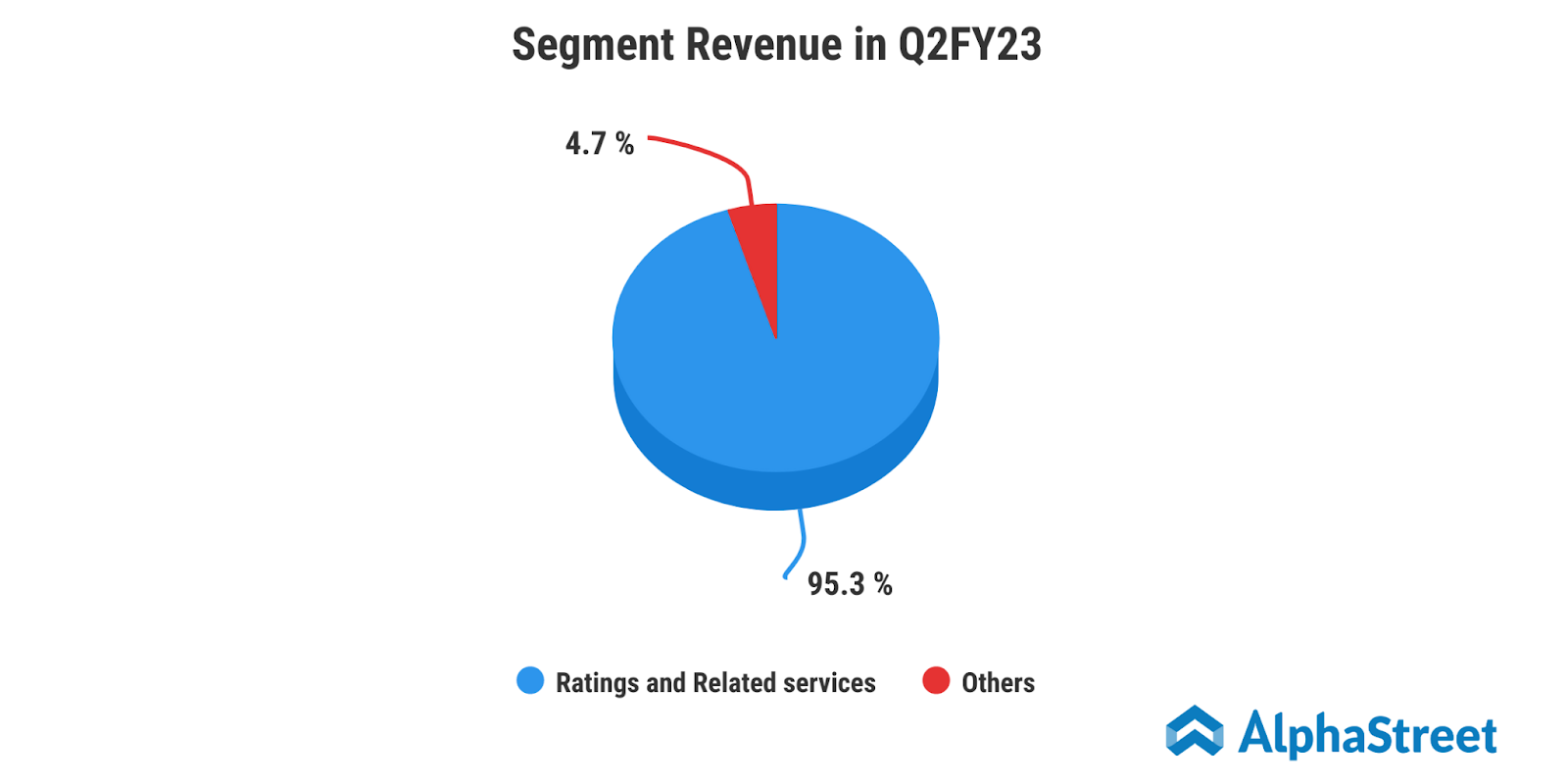

CARE Rating earns more than 95% of its revenue from rating business and has recently launched risk solutions and research subsidiaries to create organic growth. CARE Kalypto Risk technologies provide risk management solutions which are a niche financial area where the bank needs to spend significant funds to purchase the solution. CARE Advisory Research and Training Ltd works in research that supplements their rating business. People who register in CARE Advisory have to go through an established course which later assures them a job as well as quality personnel for CARE.

CARE Ratings (Africa) Private Limited (CRAF) is a subsidiary of CARE now operational and has also completed a few rating assignments. This venture aims to leverage opportunities in the African continent. CRAF has also got the recognition from Bank of Mauritius (BoM) as an External Credit Assessment Institution (ECAI) for all market segments w.e.f. May 9, 2016. Further, The African Development Bank has taken up close to 10% stake in CRAF

In 2017, CARE Ratings signed a MoU with Vishal Group Limited and Emerging Nepal Limited to start a credit rating agency in Nepal to be called CARE Ratings (Nepal) Limited with CARE as majority stakeholder. CARE owns a 10% stake in Malaysia’s leading credit rating agency, MARC. CARE also owns a 10% stake in ARC Ratings, a credit rating agency based out of Europe.

CARE has also entered into a technical tie-up with Japan Rating Company. The main purpose of JV is to develop a mutually beneficial relationship. CARE now has an alternative for the client who wants an international rating and does not want to go to two established players. Similarly, JRC would assist CARE in getting business from the investment happening through Japanese investors. CARE has consistently increased their market share for the last 10 years that can be seen below.

Competitive advantage:

- Monopoly: This is a high entry barrier business due to the reputation of existing established players as explained earlier.

- Robust nature of business: Rating agencies are not legally liable for their opinions and can change their ratings conveniently.

- Higher switching costs: Switching to another rating agency is a time-consuming process & costs additional money. An existing rating agency would have a thorough understanding of the business along with a detailed database of the company. This would save precious time/ effort for existing rating agency

- Network effect: Established players that provide quality service enjoy brand recognition and a strong industry network which attracts new borrowers.

- Consistency and credibility: Most corporate borrowers would desire consistency and comparability in credit opinions. Also, investors preference for CRA’s with a long-standing track record would ensure that newer players would take substantial time to gain investor confidence

India Macros

The growth of credit rating agencies is tied to credit offtake i.e. loans issued by banks and corporate debt (bond) issuances. Thus, it is important to know about macros of the Indian economy and developments around corporate debt to gauge the future growth for credit rating agencies.

The credit offtake has been slowing down since 2011 and hit a multi-year low in 2017 due to transformational changes in the last couple of years such as demonetization & GST. This figure has slumped in the last two years due to economic slowdown. These are actually beneficial changes for the long-term prospects of the economy and credit offtake is likely to pick up from here. India is on the verge of being a 5 trillion economy and this will only be possible due to an effective credit push.

The bank loan growth was subdued due to NPA issues for majority public-sector banks in India. The rating business in the last few years has been somewhat challenging considering that, as the market matures the volumes are dependent on what comes on the borrowing floor. When the economy does not grow at the desired rate, the level of borrowing slows down which then impacts the rating industry canvas. In the past, there was space to be sought on the bank loan rating piece when the Basel II approach was implemented in 2008. It was easy to grow business as there were many unrated companies. Progressively with time, as the backlog of unrated bank loans reduces, the overall mass of the rateable universe becomes dependent on growth in credit.

Currently the corporate debt market in India is only 15% as compared to 40-45% of developed countries. The bond market in India is still developing and there has been substantial growth noticed in recent years. Thanks to the Modi Government. It is showing signs of a higher growth trajectory with issuances being steady.

RBI in May 2016 issued new guidelines for banks whose exposures of specified borrowers over a specified limit would attract a higher capital risk weight than before. This would encourage such borrowers to approach the bond market for lower interest rates. Banks can subscribe to bonds (issued by corporates who have reached the NPLL.) and may help such issuers.

The latest regulatory framework for banks – Basel III allows banks to have their internal rating for loans. There was much news about this implementation taking away the rating agency’s business. However, RBI has clearly encouraged banks to use external ratings to measure the credit risks. Moreover, With the NPA issues in hand, banks will not want to be held accountable if a large loan goes bad.

Small & Medium Enterprises (SME) is a highly untapped market in India. The penetration level is less than 15% in this market. Although, CRISIL is the major shareholder of this market. CARE is all set to get more business from this growing sector. Also, Care’s approach to the SME business is based not just on getting more assignments but works on the assumption that they would become larger with time and be potential borrowers in the debt market.

Positive developments:

- The developments that augur well for the business have been the focus of the government and the regulators (SEBI and RBI) on deepening and development of the bond market.

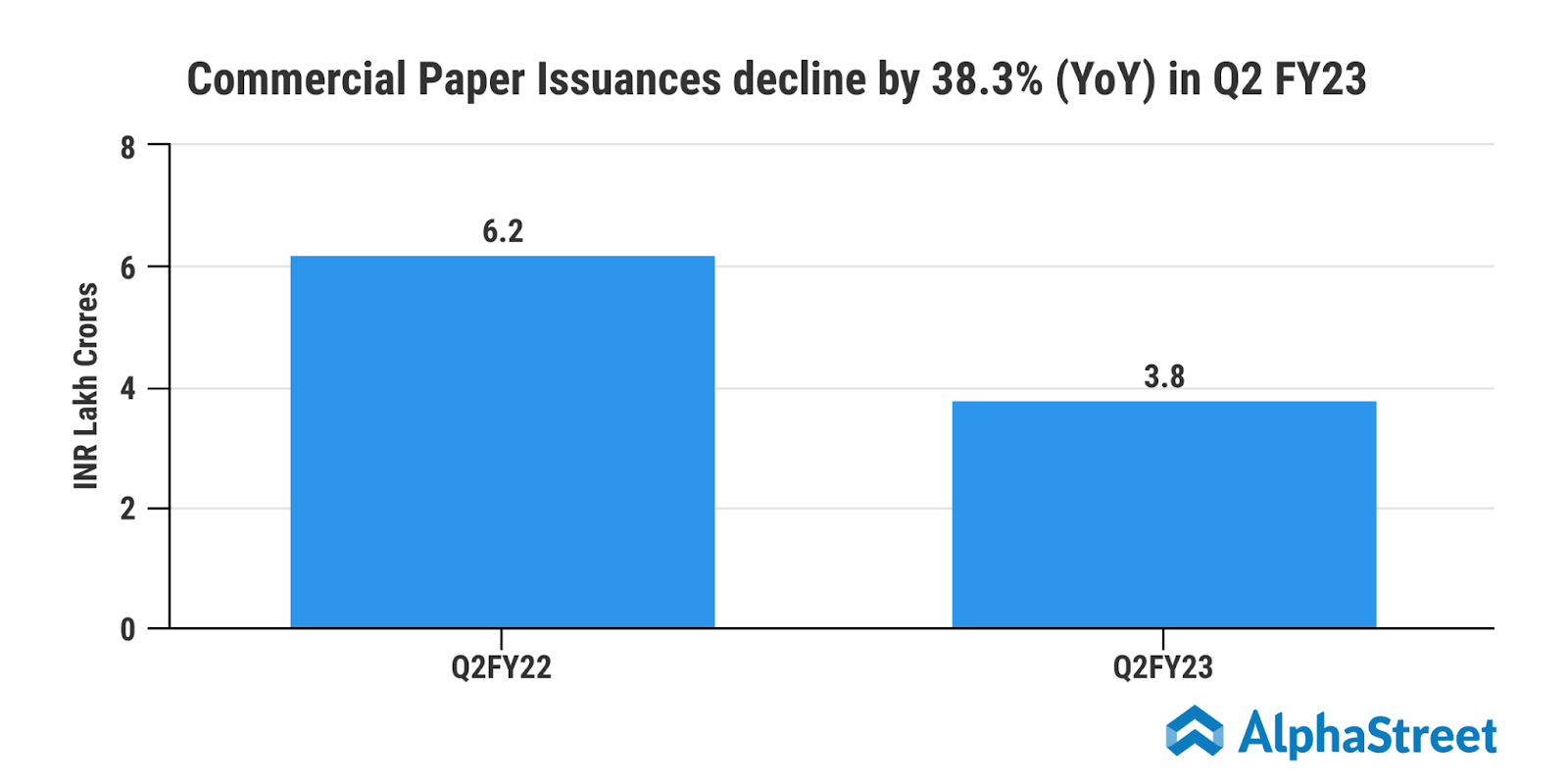

- The RBI has issued directives on Commercial Paper (CP) in August 2017 where if for a company, CP issuance during the year totaled Rs.1,000 crore or more in a given year, the issuer shall obtain credit rating for issuance of CPs from at least two CRAs registered with SEBI and should adopt the lower of the two ratings.

- The requirement of Independent Credit Evaluation (ICE) by Credit Rating Agencies (CRAs) for stressed assets that bring up a resolution plan, is a significant opportunity for CRA’s

- With increasing regulatory push for part financing, incremental borrowing, in case of large exposures through capital market financing, including bonds, augurs well for CRA’s.

- Rating requirements for Infrastructure Investment Trusts (InvITs) and Real Estate Investment Trusts (ReITs) are factors likely to deepen the domestic debt market.

Downside risks:

- Any economic slowdown in India may impact the volume of bank credit or debt securities issued in the domestic capital markets, and hence, have an adverse impact on CRA’s.

- Majority of Rating Agencies customers are NBFCs that are adversely hit during tight liquidity conditions.

- CRA’s are dependent on the condition of the financial markets in India. Any increase in interest rates, foreign exchange fluctuations, defaults by significant issuers/borrowers, may negatively impact the issuance of credit-sensitive products.

- The bank loan rating business may get impacted if there is a credit slowdown or change in rating related regulation resulting in transition to internal rating models for providing capital.

- The domestic debt capital market is skewed towards higher-category credit-ratings. This may continue to constrain the volume of issuance in the Indian debt market. However, to encourage raising funds from the bond market, the regulators may move from ‘AA’ to ‘A’ rating for investment eligibility.

- Currently, accessing overseas debt markets by certain Indian borrowers/issuers is regulated, and any change in the prevailing regulatory regime, liberalizing access to overseas markets for the raising of debt funds, may adversely impact the issuance of debt instruments in the domestic market.

- CRA’s business is largely dependent on the recognition of brand and reputation. In this regard, prominent investment-grade defaults, multi-notch downgrades or failure to appropriately assess the creditworthiness of instruments rated by CRA’s could negatively affect reputation and position as a quality credit rating agency. This, in turn, may adversely affect business, operations, and financial condition.

- Non-payment of fees by clients: In the event of downward revision in ratings, there would be a threat of non-cooperation of clients to continue with the rating exercise, which may result in loss of revenue. For new assignments, CRA collects initial fees in advance before rating is assigned and it does not carry the risk of non-payment of fees by clients. However, CRA’s are bound by regulations of carrying out reviews and surveillance in a timely fashion. This may, at times result in carrying out rating reviews without receipt of fees.

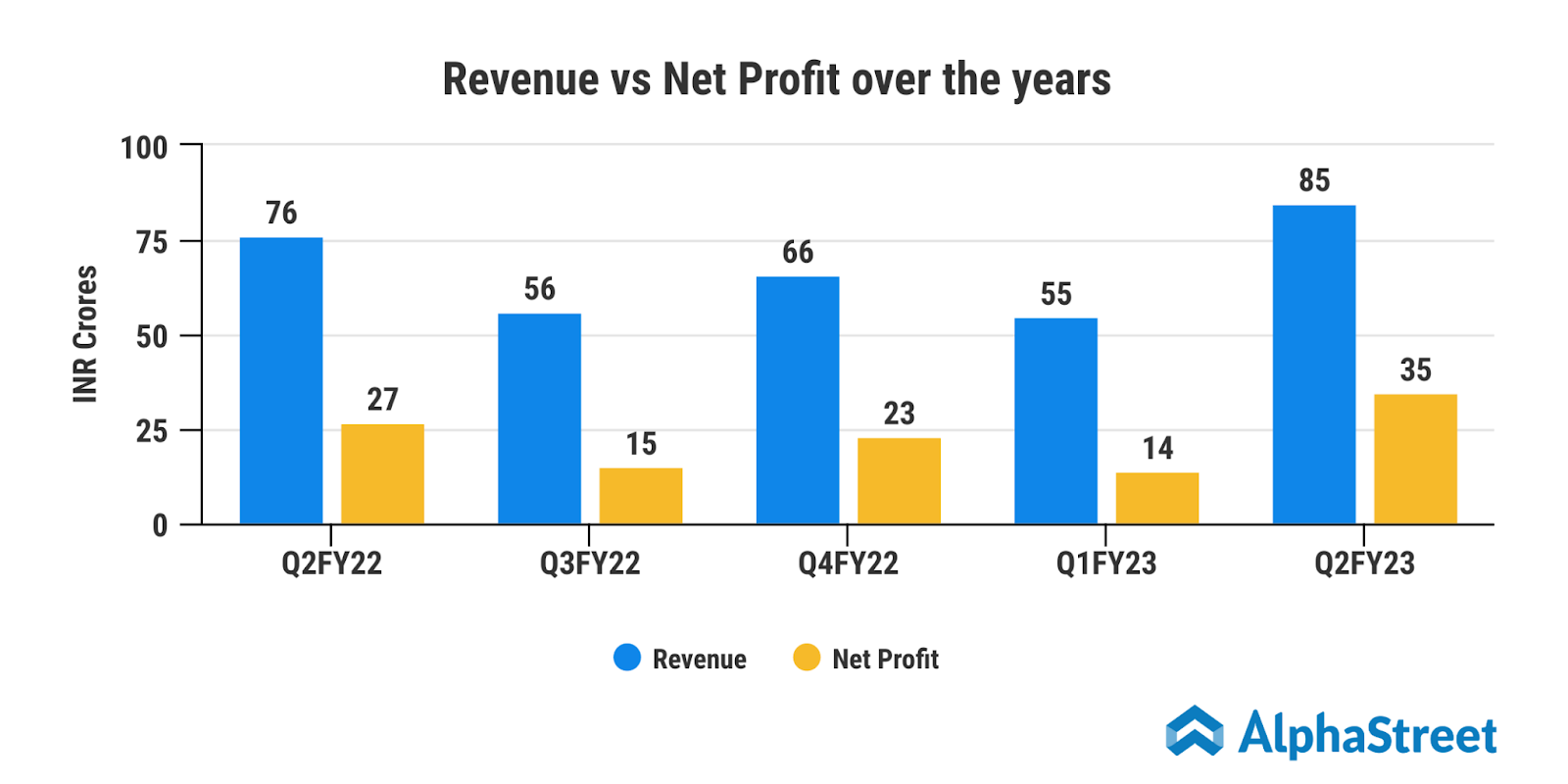

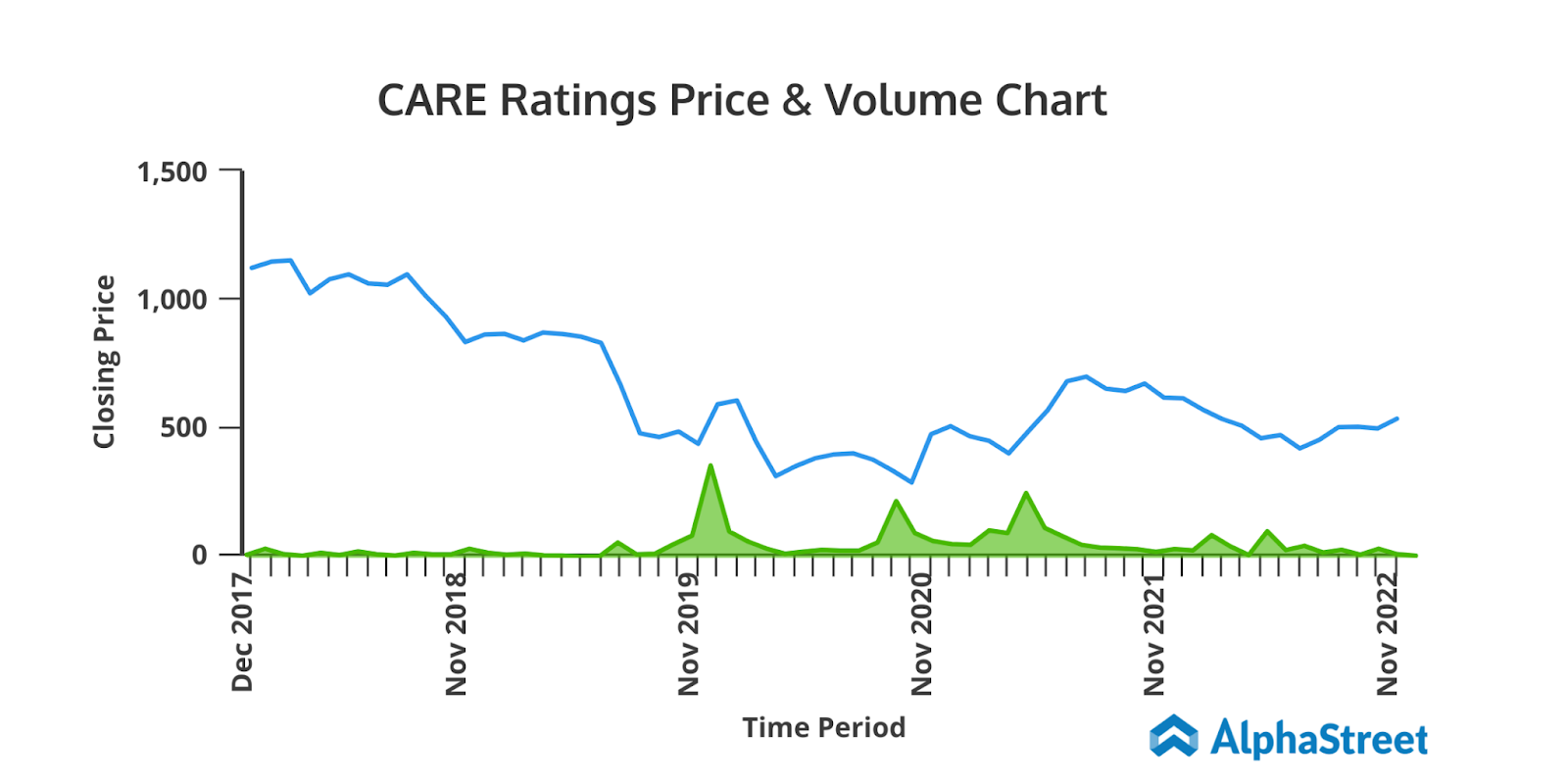

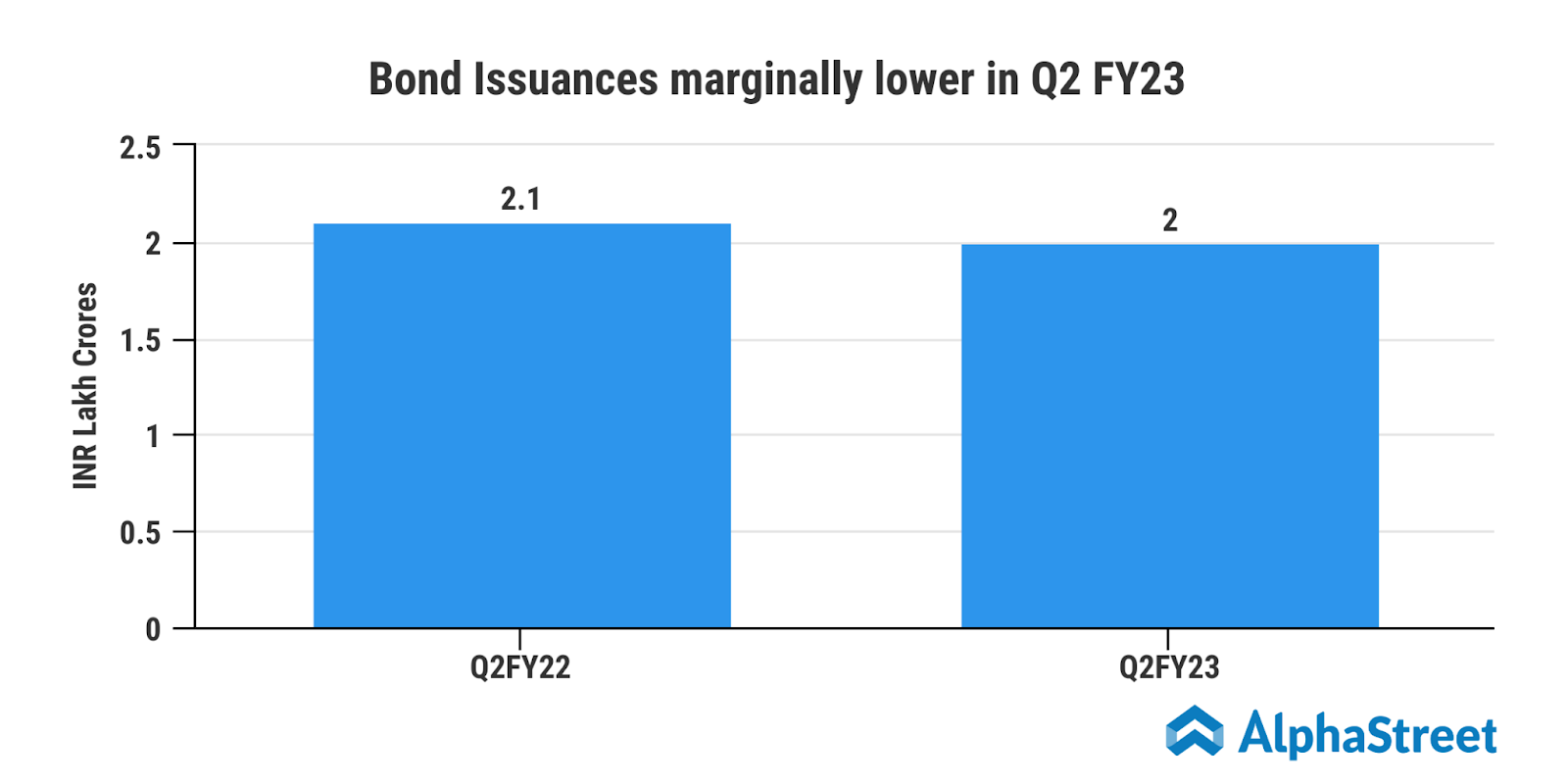

Charts: