“We performed remarkably well this quarter, despite the existence of macroeconomic challenges, our profitability clearly demonstrates our steady progress. CASA and CMS continue to outperform our expectations and we are very confident of this momentum to continue. This year, we also enhanced on our digital groundwork, the digital throughput gained traction and increased from 16% to nearly 23% between Q1FY23 and Q4FY23”

– Rishi Gupta, CEO & Managing Director

Stock data

| Ticker | FINOPB |

| Exchange | BSE and NSE |

| Industry | Banks |

Price Performance:

| Last 5 days | +1.89% |

| YTD | -12.56% |

| Last 1 year | -15.44% |

Company description:

Financial Inclusion Network Operations (“FINO”) is a growing fintech company offering a diverse range of financial products and services that are primarily digital and have a payments focus. It offers such products and services to the target market via a Pan-India distribution network.

Representative of Banks:

The Bank acts as a Business Correspondence (Bcs) of several Banks It had approximately 17,430 active BCs across India in FY21. BCs are generally retail agents engaged by it to provide banking products and services on behalf of other banks and at locations other than traditional branches. BCs are authorized to perform a variety of activities including collection of domestic and international remittances, CASA account opening functions, payments made via AePS, bill payments, and mobile recharge, among others.

Differentiated Business Model:

The company operates an asset-light business model that is underpinned by the phygital model i.e. Through the “phygital” delivery model merchant’s onboard customers and facilitate transactions, ensuring the network grows and products and services are more accessible to a broader range of customers throughout India.

High Reliance on Fee Income:

Fino Payments Bank principally relies on fee and commission-based income generated from their merchant network and other participants which accounted for 85% of the income generated by the company in FY22.

Pan India Presence:

The Bank has 13.7 lakh merchants (own and API) registered as of FY23. On March 31, 2022, the Bank had a nationwide distribution network and was present in 90% of India’s districts. It has 42 branch locations and 111 Customer Service Points.

Cross-selling of products:

Their merchants leverage the customer relationships within their respective communities to facilitate cross-selling other financial products and services such as third-party gold loans, insurance, bill payments and recharges.

High Concentration in North India:

A large number of its merchants are located in the states of Uttar Pradesh, Bihar, and Madhya Pradesh. As of June 2021, 46% of its merchants were present across these three states. It has a presence in 28 states/Union Territories (UTs) with Maharashtra accounting for the majority share of revenue followed by Uttar Pradesh and Bihar.

Strategic Investment:

The company has made a strategic investment worth 2.5 crores in Paysprint Private Limited, a fintech company offering next-generation APIs in the BFSI space, with the intention of building their digital ecosystem.

IPO Details:

In FY22, The co. successfully raised 1200 Cr through the IPO of which 300 Cr is a fresh issue and the remaining 900 Cr is an offer for sale.

• The fresh issue made by the company will be utilized for Augmenting Bank’s Tier – 1 capital base to meet its future capital requirements.

• To meet the expenses in relation to the offer.

Bonus Issue:

In July 2021, the co. had approved the allotment of 3.3 crores Bonus Equity Shares of the face value of Rs. 10 each in the ratio of 0.75:1.

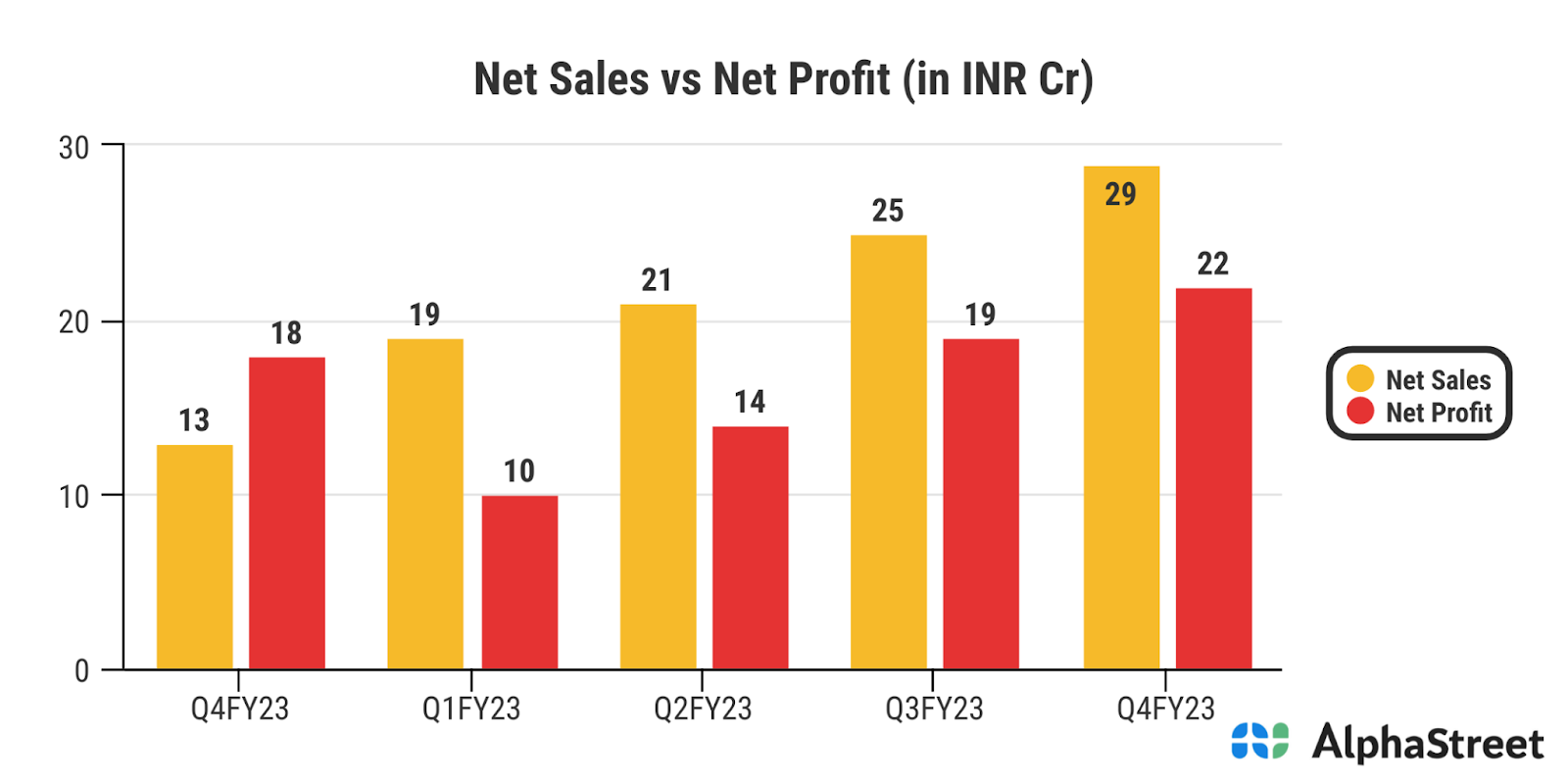

Financials:

What we like:

- Total customer base stands at 7.5mn and management aims at 20mn by FY26:

Sustained traction in new customer acquisition since the launch of CASA product in FY19 helped Fino build a strong 7.5mn ‘on us’ customer base. Hyper-local personalized service, extended banking hours and wide range of products have been the key enablers of faster adoption of the first-of-its-kind subscription-based CASA product. Company aims to reach a customer base of 20mn in the medium term and, to achieve this target, it is continuously expanding its merchant base. Total merchant base as of March 23 stood at 1.37mn, up 5% QoQ.

- Unique business model with strong merchant network:

Its merchant-led model is a capital light business strategy in respect of network expansion and except for referrals of third party loan providers, it does not offer any lending products and does not hold credit risk for loans. In addition, its well established technology platform and consistent investment in further improvements, allows it to service a wide pool of customers and cater to their diversified requirements. In addition, focus on and use of technology throughout its business assists in expanding its reach throughout India without incurring the relatively higher costs associated with traditional bricks and mortar branch presence. In addition to the merchant network which, as of March, 2023 was ~13.7 Lacs.

- Its tech savvy approach keeps it ahead of its competitors and pushes it to innovate:

Fino Payments bank has and will continue to invest into technology throughout its business. Its in-house technology expertise and culture of application-led innovation provides an attractive value proposition to its stakeholders. Currently, it is equipped with reporting process automation based processes at the back-end, SAS dashboards for analytics and demand forecasting, fraud risk management system for fraud detection, and other security systems and a network of servers. Since 2017, it has made significant investments in technology infrastructure, having designed and digitized large portions of its technology processes, risk management protocols, data analytics capabilities and honed its “phygital” approach.

- Increasing share of own banking channel revenue brings stability:

Fino’s gross revenue stood at Rs3.2bn in Q4FY23 vs Rs2.9bn in Q4FY22, implying growth of 13% YoY. During the past 12 months, management has incrementally focused on building a sustainable revenue stream led by its own banking channel. As a result, the share of its own banking channel revenue increased to 67% as of March 23.

Factors to consider:

- Increasing competition could result in higher merchant pay-outs, which in turn could dent margins.

- Faster adoption of UPI payments via feature phones could impact remittance volumes.

- This industry faces stiff competition from other fintech apps specially in MATM and AePS businesses.

- Any new payment mode that disrupts the currently existing digital modes may be a serious threat. The way UPI disrupted the whole payment system make this a serious risk.

- Any regulatory restriction putting a cap on the subscription charges on savings accounts or downward revision of interchange charges on MATM/AEPS may significantly affect the revenue of the payment banks.