Financial Results:

ICICI Bank Ltd. has expanded its loan portfolio by 22.7% YoY. This increase in total advances have contributed to the increased operating profit.

It is evident that part of the increase in profitability stems from the reduction of Provisions & Contingencies amount by 39.4%. That would explain why the YoY growth for Core Operating Profit is 23.6% whereas the YoY growth for Profit After Tax is 37.1%.

| ₹ Cr. | Q2FY23 | Q2FY22 | YoY% |

| Net interest income | 14,787 | 11,690 | 26.5% |

| Core operating income | 19,926 | 16,090 | 23.8% |

| Operating expenses | 8,161 | 6,572 | 24.2% |

| Core operating profit | 11,765 | 9,518 | 23.6% |

| Net provisions | 1,644 | 2,714 | (39.4%) |

| Profit after tax | 7,558 | 5,511 | 37.1% |

Key Ratios:

Net Interest Margin has increased on a YoY basis. That is supported by the fact that the return on average assets has also seen an increase. This showcases the reasoning behind the bank’s increased profitability.

However, the Cost of Deposits have seen an increase despite the fact that share of CASA Ratio has increased. Along with that, there seems to be a slight increase in the Cost to Income Ratio of the bank.

| Percent (%) | Q2FY23 | Q2FY22 |

| Net interest margin | 4.31 | 4 |

| Cost of deposits | 3.55 | 3.53 |

| Cost-to-income | 41.1 | 39.9 |

| Return on average assets | 2.06 | 1.79 |

| Standalone return on equity | 16.6 | 14.1 |

| Book value (₹) | 261.9 | 226.1 |

Growth in Loan Portfolio:

- Retail loans grew by 24.6% YoY

- Rural Loans grew by 11.7% YoY

- Business banking portfolio grew by 42.6% YoY

- SME portfolio grew by 26.5% YoY

- Domestic corporate portfolio grew by 23.1% YoY

There is a significant increase in advances made by the bank which has largely contributed to the increase in profitability of the bank. The bank has expanded its circle of operations by increasing its loan portfolio by 22.7%.

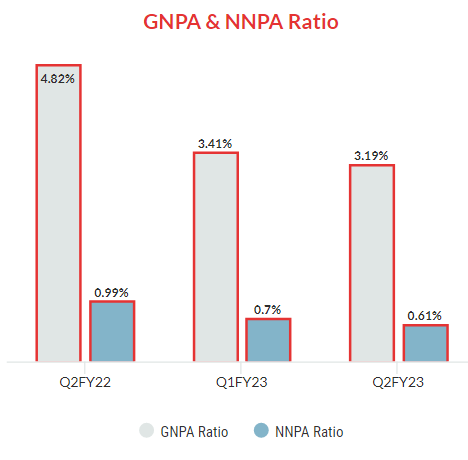

Asset Quality:

There seems to be an improvement in the asset quality of the firm. This is reflected by the reduction in the bank’s non performing assets. Both Gross Non Performing Assets (GNPA) as well as Net Non Performing Assets (NNPA) have reduced.

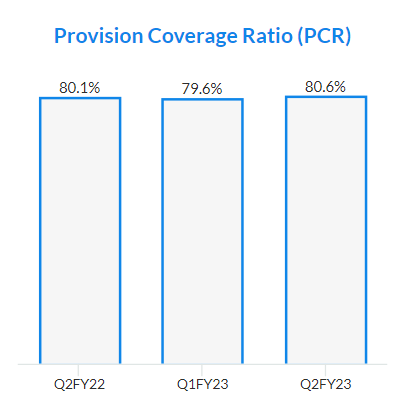

As discussed earlier the reduction in Provisions contributed to the profitability of the firm. Provision Coverage Ratio indicates that the reduction in the provision amount was made because of the improvement in asset quality and not for any other reason.

The high Provision Coverage Ratio despite the bank’s varying asset quality showcases the bank’s commitment to ensure the bank’s safety regardless of the ups and downs faced by economic conditions.