What’s your idea of a full day picnic or outing for an average middle class family? Infact, what are the entertainment options available for you on the platter on weekends?

I bet the first thing that would come to your mind would be to visit some mall and watch some movie followed by a sizzling dinner in the food court. Now that sounds awesome and this is what precisely everyone is doing nowadays apart from Netflix and chill. But there is not much decent content to watch with your family and honestly there is not much sightseeing that you could do. What else would you do? Well, frankly, there are not many options available that are exciting and affordable at the same time.

And this is precisely what got us to explore the amusement park space in India. An amusement park provides a great avenue for full-day entertainment for an entire family at an affordable price. Now, you must be wondering that this space is too big, right?

But the amusement park industry is too small with an estimation to be around Rs 4000 Crores and is expected to grow at a CAGR of 10-12% over the next 10 years. The Indian amusement industry consists of around 150 parks.

The sources of revenues for these parks are entry fees, food & beverages (F&B), retail products, sponsorship and advertisements, resorts and other miscellaneous rentals.

Surprisingly, in India major revenue for the parks is in the form of entry fees about 75-80%, F&B and merchandising contribute about 18-23% and resorts and other rentals about 2%. Parks globally receive 31-35% of their revenues from entry fees, 32-35% from F&B and 35-37% from the resort and other rentals. Indian parks have a lot of catching up to do in the F&B and resort rental space when compared to their global peers. Amusement parks in India charge either single entry fees at the gates, pay as you go option or separate fees for dry and wet rides or a combination of both.

One of the major drivers for amusement parks in India are the demographic advantages, so, 28.5% of the population lies in the age group of 0-15 years, 63.40% in the 15-59 and 8.10% lies in more than 60 years. Rising disposable income levels, increased spending on tourism and leisure activities & rising urbanization are the other factors that will lead to more people visiting amusement parks.

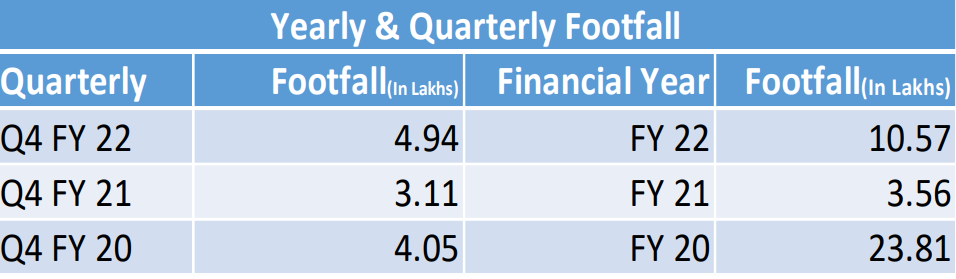

In terms of footfall, the Indian amusement space is quite undersized as compared to its global peers. The industry witnesses an annual footfall of around 5 – 6 Cr. The footfall depends primarily upon the size, location and offerings of the parks. As India experiences hot climates almost 7-8 months in a year, water parks are a popular format. Surprisingly, a majority of these 150 parks are run by some regional entrepreneurs and none of them holds an ambition to make it a professionally run business with multiple chains. As a result these parks lack proper sanitation, safety and regular updation of innovative rides to get repetitive footfalls.

The beginning and the growth:

The promoter of V Guard industries – Mr. Kochouseph Chittilappilly identified the above problems and started the first park in his hometown Kochi in 2000 by the name of Veegaland (now known as Wonderla). Wonderla Kochi is situated on 93.17 acres of land, and currently, only 28.75 acres is being occupied for 56+ water and land based rides. They also have 7 restaurants in Kochi.

The second park was set up in Bangalore in 2005 and is situated on 81.75 acres of land and currently, 39.2 acres is being occupied for more than 55 land and water rides plus the resort. They have 7 restaurants in the Bangalore park. The company has a resort in Bangalore. The resort was set up in March 2012 with 84 rooms with a capex of 28 Cr. The resort provides amenities like banquet halls, conference rooms, restaurants, gym to name a few. To offer customers an extended stay wherein they can enjoy the amusement park which in turn would also increase the customer spend, such resorts were opened.

The company came up with an IPO in 2014 to fund its third park in Hyderabad which was launched in April 2016. The park started generating revenues from Q1FY17 and the company has acquired 49.57 acres of the Hyderabad park for 25.47 Cr. The company has used only 27 acres for 42+ land and wet rides.

They have also acquired land for the Chennai park and they will be starting its development in FY23, which will take another 2-3 years to finish, for which Wonderla will be investing Rs 300 crore. Wonderla has recently announced the signing of an agreement with the Odisha government for the development of an amusement park project in Bhubaneshwar. They have leased a 50.63 acre land for 90 years in the village of Kumarbasta, Khorda district in Bhubaneswar, Odisha. Wonderla is planning for a 115-crore investment project based on an asset -light business model.

Now having known about the company, let’s see why they are so special.

Competitive advantages:

These moats help the company stay ahead of its competition and create a monopoly in its niche.

- High Entry Barriers:

As we know that the amusement park industry is capital intensive and companies that operate in this space need to spend a lot of upfront money for setting up new parks, spend for new rides every 2-3 years to attract customers and get repeat footfalls and spend money for maintenance every year. Hence, these factors make it very difficult to survive and thrive in this niche. Now many companies have set up their park as an early mover advantage but lets see how Wonderla tackles them:

Wonderla has established three parks in Kochi, Bangalore and Hyderabad which are already the prime cities of the South. If any competitor needs to set up parks in these locations then they would need to spend a lot of money on rides and equipment which Wonderla has already spent on those assets and they have been fully depreciated as well. Getting permission for an amusement park is very difficult since a lot of water gets wasted in such a process and this would again be a challenge for other competitors. Wonderla bought these land a long time back and since then the prices of land have appreciated and now the companies will have to pay much higher fees.

Even if one assumes that any company has deep pockets and is able to set up a park in one of these locations it will take a lot of time for the company to break even Wonderla and that company cannot price its tickets higher than the competition. So in total any competitor will have to 3-4x of Wonderla is spending in need to market itself.

Also, Wonderla Holidays has been very strategic in setting up its parks in good locations. Its latest park in Hyderabad, also does not have any major competition. The catchment area for such huge parks as Wonderla is in the range of 250-300 km. Further, the company is expanding itself in Chennai and Bhubaneswar which will make the company a complete Southern belt player.

- In-house manufacturing of rides:

At a point where other parks spend a lot of money in buying new rides, Wonderla has an in-house manufacturing facility in Kochi. The advantage of manufacturing the rides in-house is that if a company manufactures its own rides, the cost is 1/3rd the cost it would have to pay if it procured the rides from external vendors.

Not only this but the company is always on the lookout for developing innovative rides. The company sends its key staff to amusement parks across the world to observe new trends, this exercise helps them to conceptualize new innovative rides, thereby enhancing customer experience.

- Customer delight:

The company is aware of the fact that to attract footfalls and have repetitive customers, they need to be innovative and manufacture new rides. And for this reason, Wonderla introduces one new ride every 2-3 years in its parks and also sends its staff to parks across the world to observe trends.

As a result of these efforts, Wonderla parks in Bangalore, Kochi and Hyderabad were ranked at #3, #8 and #17 respectively in India by Tripadvisor. Surprisingly, Wonderla Bangalore is ranked 11th Best in Asia. These positive effects help the company create a network effect which attracts other customers to the park as well.

Further, Management is one of the biggest moat of the company. The management sells all packaged foods, aerated drinks in the park at MRP. This certainly tells you something about the management, they can easily sell these above MRP and no one can question them and people will pay up for these, as they do in the cinemas. However, the management has a policy of selling all the products at MRP.

What are the sources of growth?

- Rising footfalls:

The daily average footfalls at existing parks is ~3000 as of 30 March 2022, and before COVID it was close to ~6000, whereas the capacity is to entertain more than 12,000 guests daily. Since it is a fixed cost operation, this offers a huge potential for operating leverage. In the last 10 years, footfalls have been growing at a CAGR of 10%.

- Realization per visitor:

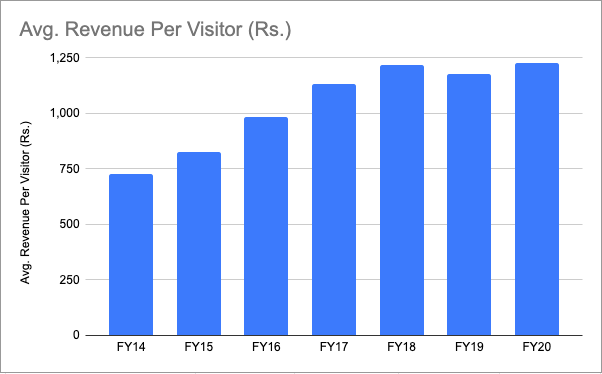

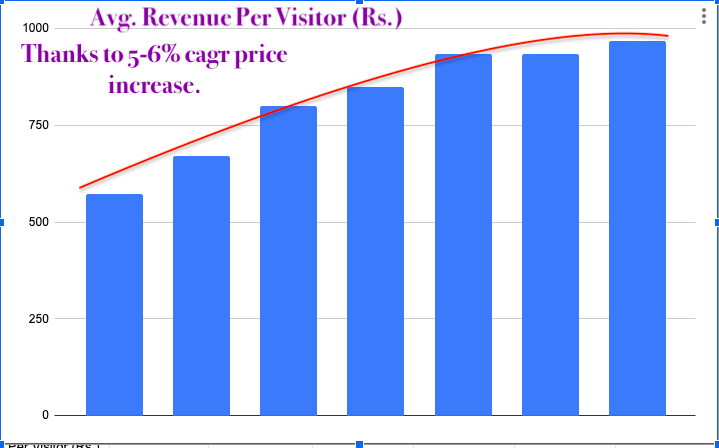

Wonderla Kochi park was launched with ticket prices at Rs 100 and Bangalore park at Rs 250, today these are at ~1000-1200, courtesy ~10% annual price hikes which wonderla has been taking. Going forward, even a 5-7% price hike will offer good operating leverage. In the last 10 years, realization per visitor has grown at a CAGR of 10%. Since Wonderla has a huge crowd daily in its parks, they have further introduced fast track bands which are charged at a higher price for fast entry into the rides.

- Sales-Mix:

By tapping other low hanging fruits like F&B and resorts to increase their contribution to revenue, Wonderla can soar its topline.

- New Parks:

The company intends to add a new park every 3 years which will help them improvise their topline by a huge margin. As discussed earlier, the company is planning to construct two new parks by 2025 for which the land has been acquired.

Why Adlabs Imagicaa failed to compete?

Adlabs Imagicaa was built on Mumbai-Pune expressway in 2012 at an investment of Rs 1600 Crores and this was a theme park not an amusement one. Now people in India don’t understand the difference between both the kinds of parks, for them both are the same. Whereas a theme park has slightly higher prices because of expenses and the experience it delivers. Keeping this in mind, Adlabs kept its price at Rs 3000 which is quite unaffordable for an average Indian. Also, Imagicaa is located at a prime location but the region receives rainfall for almost 4-5 months which results in a lost revenue. As a result, it failed to attract a huge crowd. On the other hand Wonderla does not spend more than 500 Crores on any park and does not consume the entire land at once. For instance, Wonderla’s investment in Hyderabad park was contained at Rs 250 Cr. This allows Wonderla to expand using internal accruals and without resorting to heavy debt. The management has guided to open one new park every 3-4 years using internal accruals.

By proper execution and addition of new parks, Wonderla will be able to create a monopoly in the amusement park industry in India.

But all that glitters is not gold:

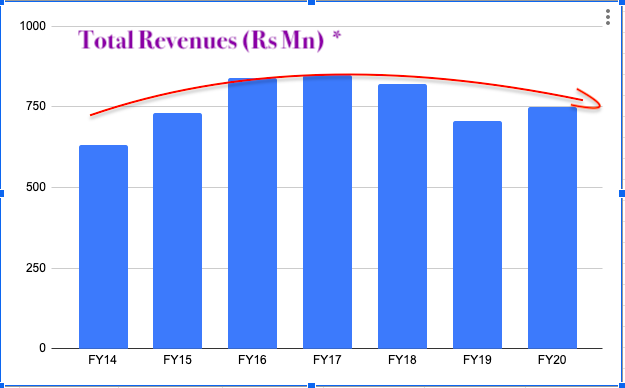

Till now the story might seem good but post IPO Wonderla existing parks reached the point of diminishing return. Let’s look at them one by one:

Bangalore-

The park has witnessed diminishing growth in revenue in the last 6-7 years and the number of visitors have actually declined. But thanks to some pricing power by which they experienced 5% increase yoy. By doing so their revenue didn’t de-grow as such but showed a decline in inflation terms.

Kochi:

Being the oldest, the same story follows in Kochi as well. It reached the point of diminishing return even earlier in point.

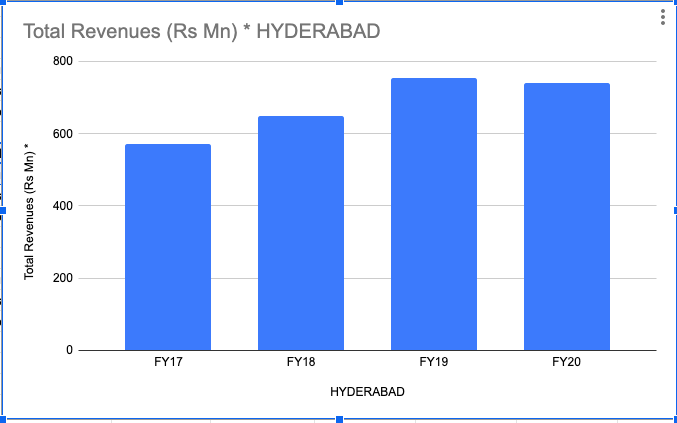

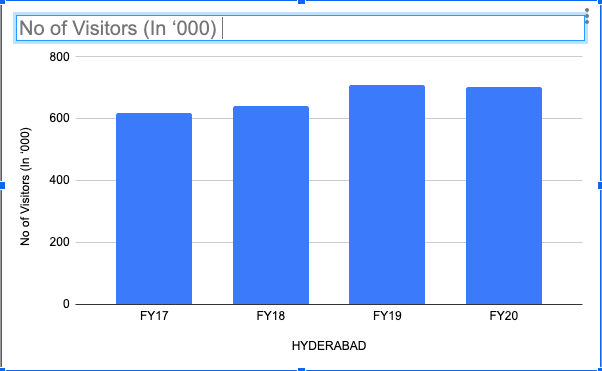

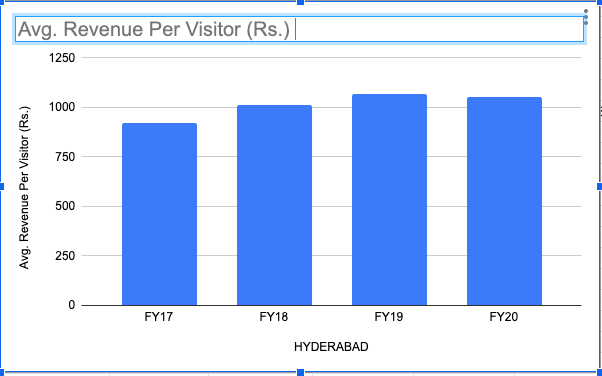

Hyderabad:

Though the Hyderabad graph looks as flattish as it could be.

Pre IPO, the company was growing at 25% CAGR with proven business model in two cities- Kochi & Bangalore and this fund was raised to open two more parks in Hyderabad & Chennai, then analysts extrapolated 4 parks cash flows = 2 more parks leads to 6 parks cash flows = 3 more parks so on.

But what is the reality?

They started building Hyderabad park in 2014, invested Rs 250 Crores and generated 57 Crores in revenue in FY17, then 64,75,72 Crores in the next 3 subsequent years. By proper planning in FY14 to FY20 they were able to earn capital they invested (Rs 250 Crores) in 7 years. Now that is 10% CAGR returns (revenue / invested capital), if you consider their 40% EBITDA margin then ROCE is going to look really bad. The real question is why in a country like India, the amusement parks are reaching out to the point of diminishing returns so early?

Now concalls are full of external reasoning like –

Extended Rains, floods in Kerala, Nipah Virus, Exams postponed for kids etc. every year something new. But there has to be something else causing footfalls to top out at around 10% of the city population. In our view, it is more to do with affordability than external factors, As going to the park with a family of 4 will cost you around 5000 in tickets + 2000 of food / travel etc.

One good thing about the Wonderla business is that it works and when something works you need to add leverage to it to maximize returns, which for some reason management is shying away from. Although they can build a park in 18 months but buying land, getting all approvals etc takes 2-3 years + 18 months to get the capex done (Eg- chennai) which really diminishes the returns for the shareholders. They can get land on long term lease rather than buying to maximize the returns for their shareholders & expand into few more many cities early as there is lag when they get approvals. so, by the time they get it they will have the cash reserve ready for expansion.

In all, if foot falls are going to remain the same in existing parks and new parks are going to show the same pattern of topping out at 10% of city population then this “land” is probably over valued even today. The growth comes from new parks & they have to keep building new parks every 2-3 years to make the business churn some profits.