KPIT is a global technology company with software solutions that will help mobility leapfrog towards autonomous, clean, smart and connected future. With 10000+ Automobelievers across the globe, specializing in embedded software, AI & Digital solutions, KPIT enables customers accelerate implementation of next generation mobility technologies . With development centers in Europe, USA, Japan, China, Thailand and India

Financial Results:

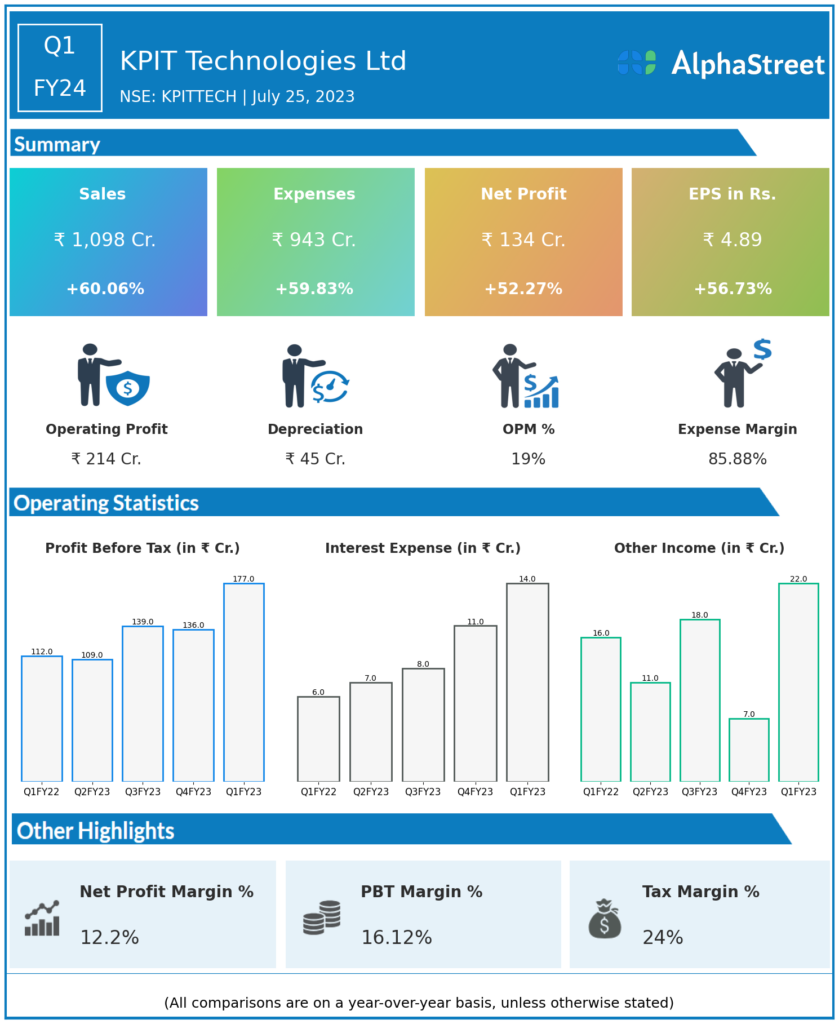

- KPIT Technologies Ltd reported Revenues for Q1FY24 of ₹1,098.00 Crores up from ₹686.00 Crore year on year, a rise of 60.06%.

- Total Expenses for Q1FY24 of ₹943.00 Crores up from ₹590.00 Crores year on year, a rise of 59.83%.

- Consolidated Net Profit of ₹134.00 Crores up 52.27% from ₹88.00 Crores in the same quarter of the previous year.

- The Earnings per Share is ₹4.89, up 56.73% from ₹3.12 in the same quarter of the previous year.

*It is important to note that the way the results have been accounted for are slightly different than the ones the companies may choose to publish.

*The presented data is automatically generated. It may occasionally generate incorrect information.