Swan Energy Limited (SEL) was originally incorporated in 1909 as Swan Mills Ltd. (SML), a manufacturer and marketer of cotton and polyester textile products in India. Over the years, it diversified into Real estate and is developing a Floating Storage and Regasification Units -based liquid natural gas (LNG) import terminal at Jafrabad in Gujarat.

Financial Results:

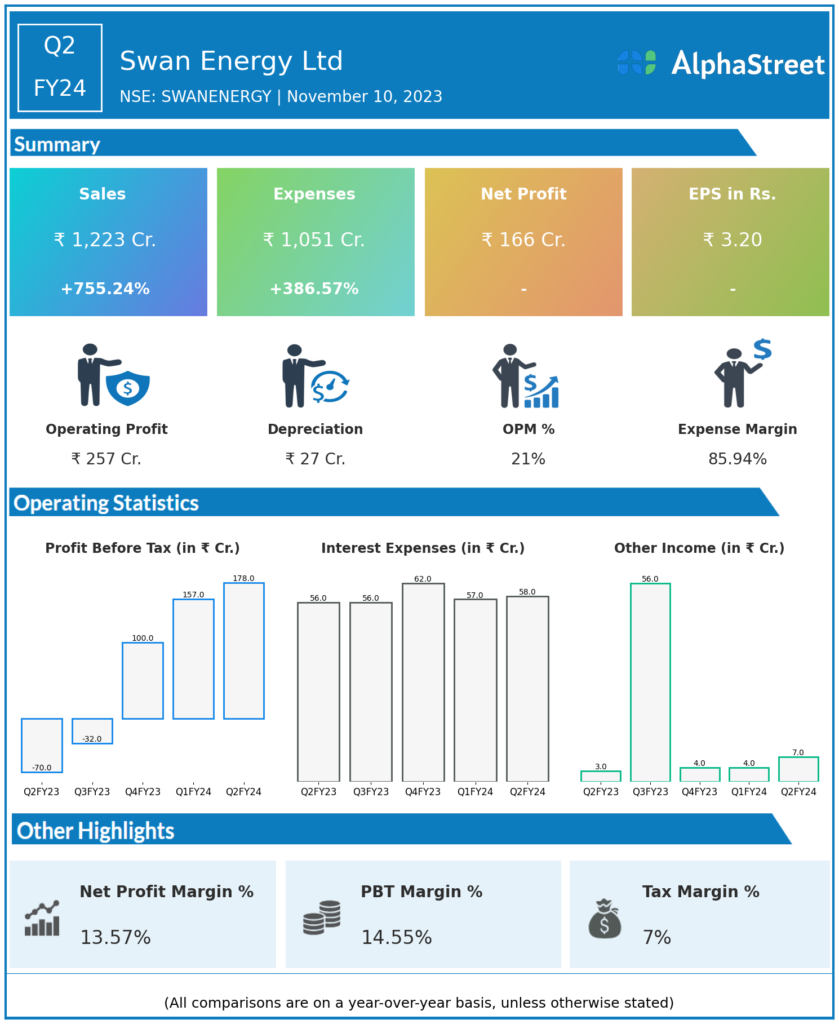

Swan Energy Ltd reported Revenues for Q2FY24 of ₹1,223.00 Crores up from ₹143.00 Crore year on year, a rise of 755.24%.

Total Expenses for Q2FY24 of ₹1,051.00 Crores up from ₹216.00 Crores year on year, a rise of 386.57%.

Consolidated Net Profit of ₹166.00 Crores from -₹58.00 Crores in the same quarter of the previous year.

The Earnings per Share is ₹3.20, from -₹1.21 in the same quarter of the previous year.

*It is important to note that the way the results have been accounted for are slightly different than the ones the companies may choose to publish.

*The presented data is automatically generated. It may occasionally generate incorrect information.