Bosch Ltd has presence across automotive technology, industrial technology, consumer goods and energy and building technology. It manufactures and trades in products such as diesel and gasoline fuel injection systems, automotive aftermarket products, industrial equipment, electrical power tools, security systems and industrial and consumer energy products and solutions.

Financial Results:

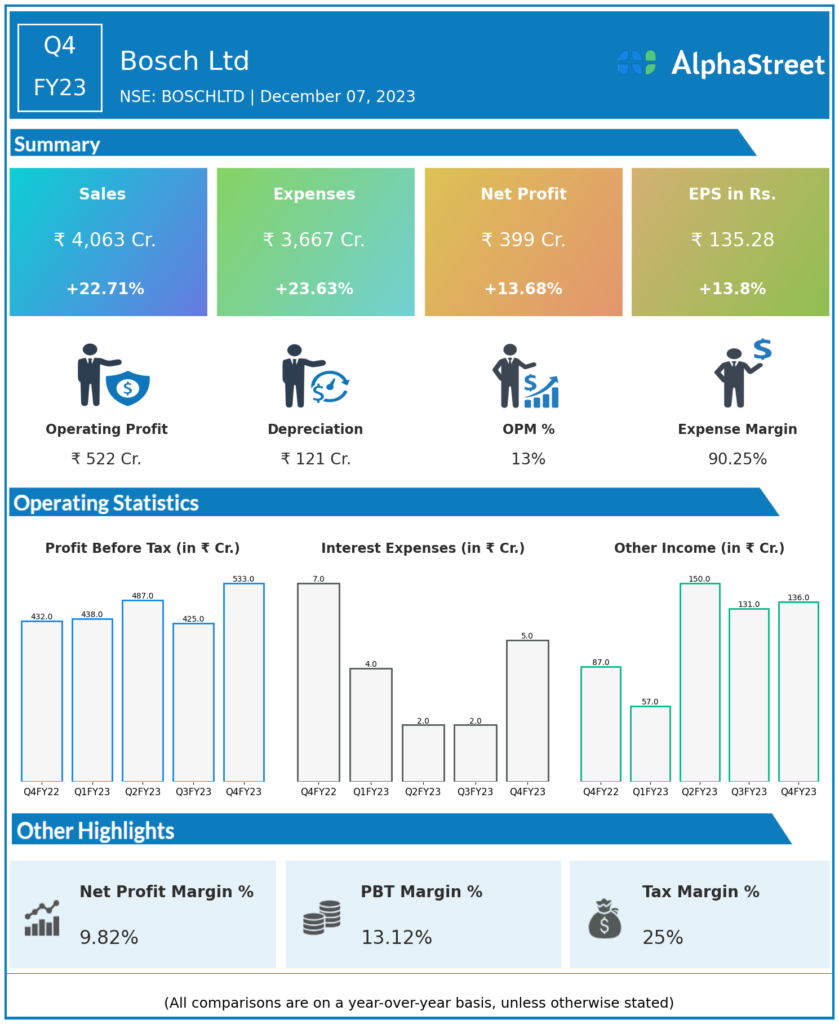

Bosch Ltd reported Revenues for Q4FY23 of ₹4,063.00 Crores up from ₹3,311.00 Crore year on year, a rise of 22.71%.

Total Expenses for Q4FY23 of ₹3,667.00 Crores up from ₹2,966.00 Crores year on year, a rise of 23.63%.

Consolidated Net Profit of ₹399.00 Crores up 13.68% from ₹351.00 Crores in the same quarter of the previous year.

The Earnings per Share is ₹135.28, up 13.80% from ₹118.87 in the same quarter of the previous year.

*It is important to note that the way the results have been accounted for are slightly different than the ones the companies may choose to publish.

*The presented data is automatically generated. It may occasionally generate incorrect information.