Central Depository Services Limited is a Market Infrastructure Institution (MII), part of the capital market structure, providing services to all market participants – exchanges, clearing corporations, depository participants (DPs), issuers and investors. It is a facilitator for holding of securities in the dematerialised form and an enabler for securities transactions.

Financial Results:

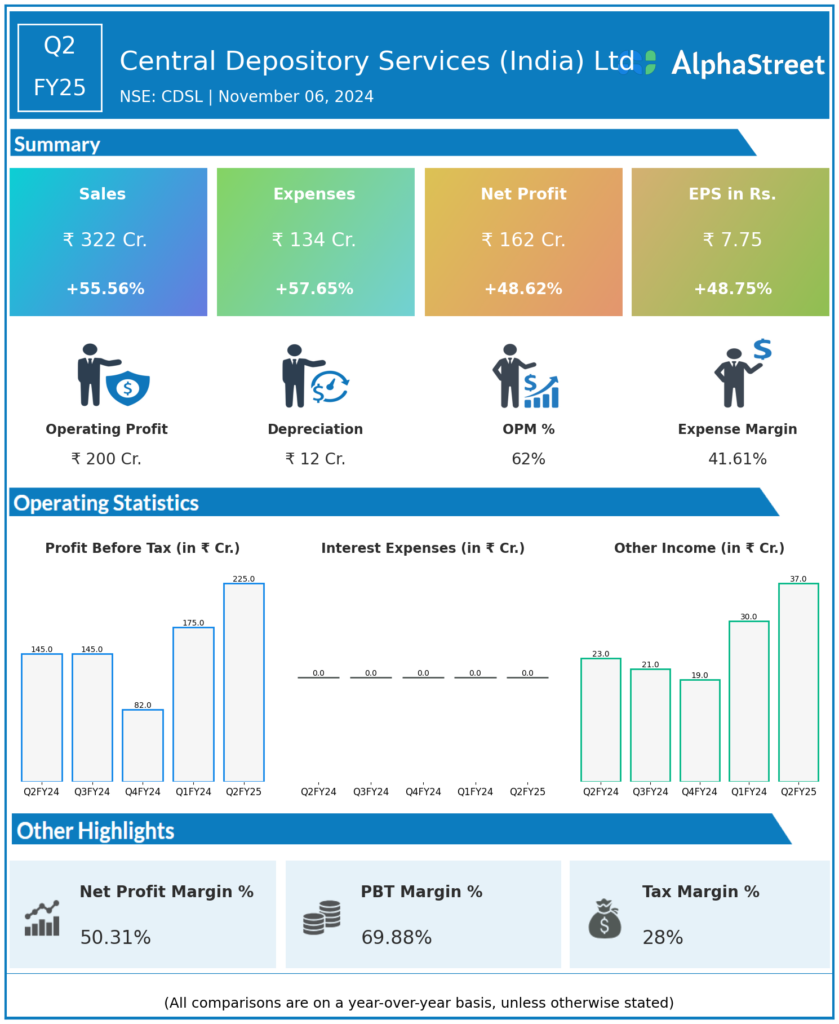

Central Depository Services (India) Ltd reported Revenues for Q2FY25 of ₹322.00 Crores up from ₹207.00 Crore year on year, a rise of 55.56%.

Total Expenses for Q2FY25 of ₹134.00 Crores up from ₹85.00 Crores year on year, a rise of 57.65%.

Consolidated Net Profit of ₹162.00 Crores up 48.62% from ₹109.00 Crores in the same quarter of the previous year.

The Earnings per Share is ₹7.75, up 48.75% from ₹5.21 in the same quarter of the previous year.