Remsons Industries Limited was established in 1971. It manufactures auto components like auto control cables, Flexible shafts, Gear shift systems, push pull cables and parking brake mechanism. It exports majorly to UK, Europe, North American, Brazil, Mexico and SAARC countries

Financial Results:

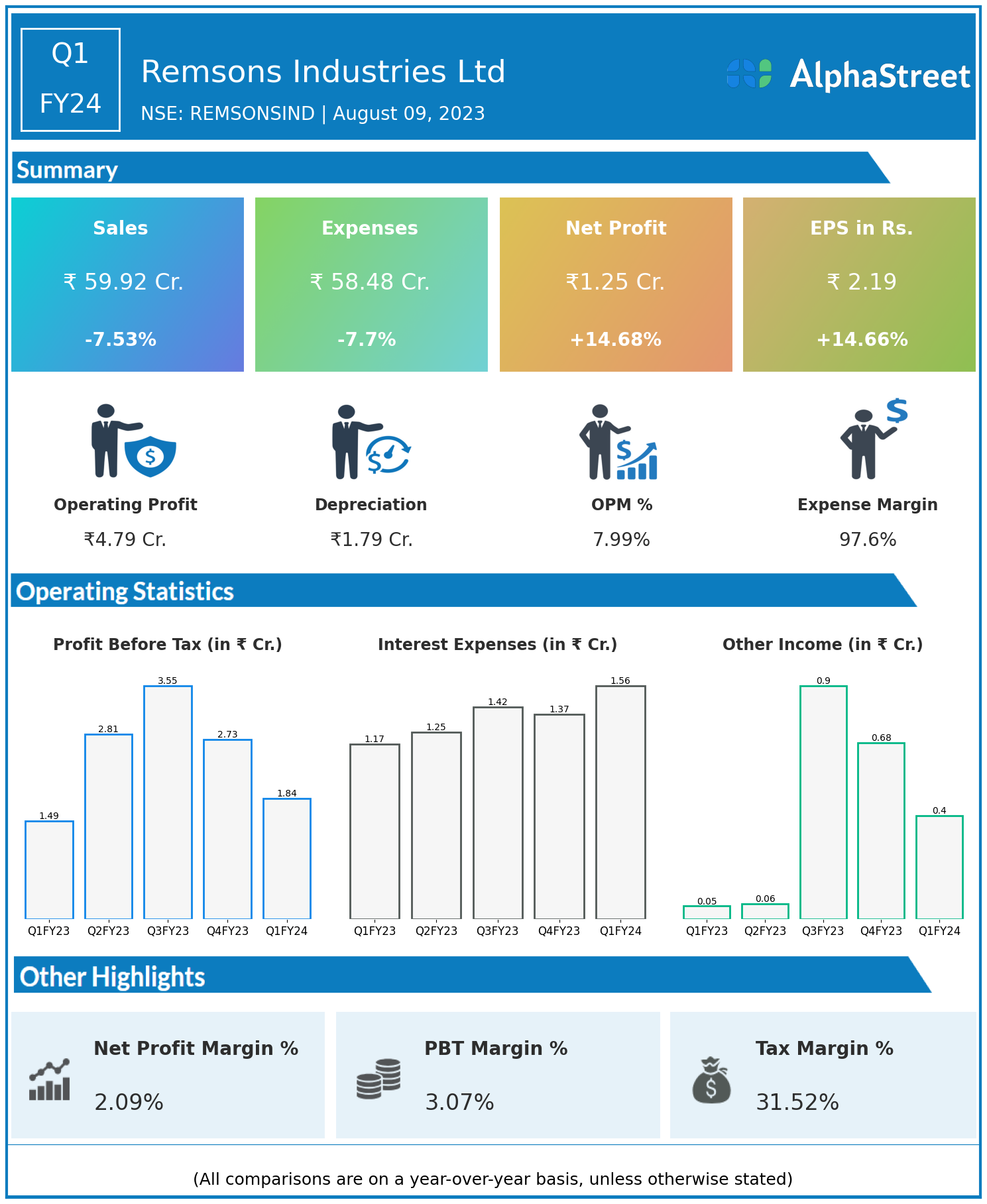

Remsons Industries Ltd reported Revenues for Q1FY24 of ₹59.92 Crores down from ₹64.80 Crore year on year, a fall of 7.53%.

Total Expenses for Q1FY24 of ₹58.48 Crores down from ₹63.36 Crores year on year, a fall of 7.7%.

Consolidated Net Profit of ₹1.25 Crores up 14.68% from ₹1.09 Crores in the same quarter of the previous year.

The Earnings per Share is ₹2.19, up 14.66% from ₹1.91 in the same quarter of the previous year.

*It is important to note that the way the results have been accounted for are slightly different than the ones the companies may choose to publish.

*The presented data is automatically generated. It may occasionally generate incorrect information.