Vedanta Ltd is a diversified natural resource group engaged in exploring, extracting and processing minerals and oil & gas. The group engages in the exploration, production and sale of zinc, lead, silver, copper, aluminium, iron ore and oil & gas. It has presence across India, South Africa, Namibia, Ireland, Liberia & UAE.

Its other businesses includes commercial power generation, steel manufacturing & port operations in India and manufacturing of glass substrate in South Korea and Taiwan.

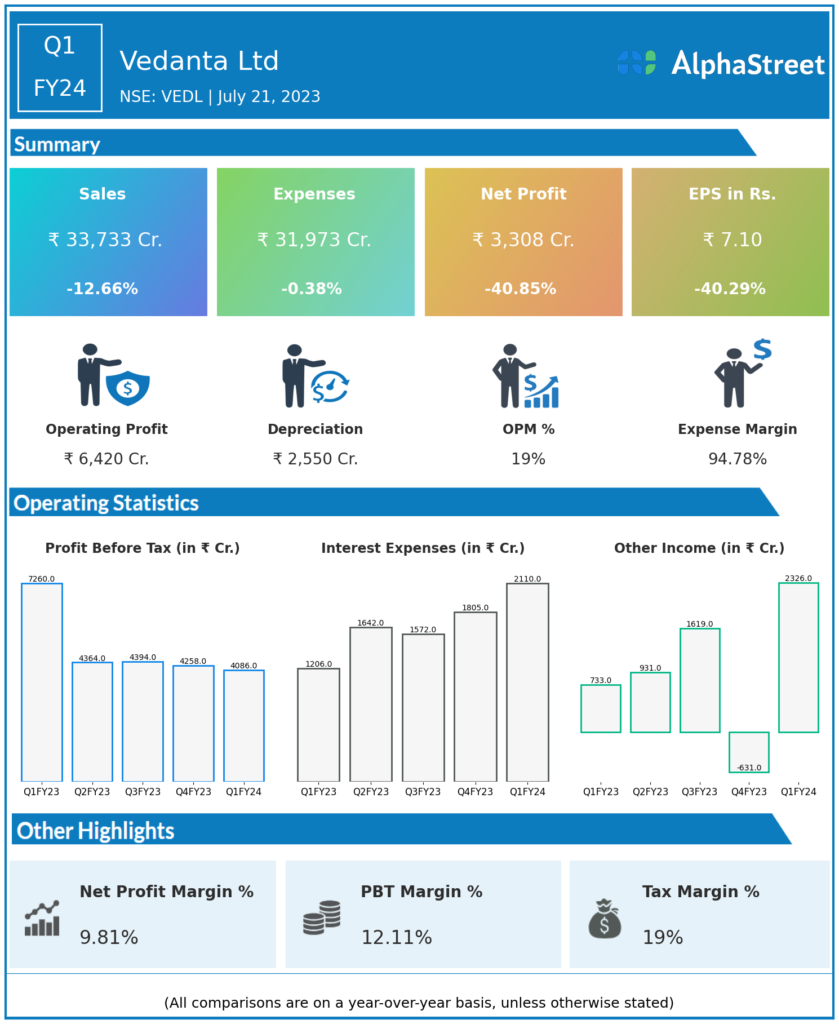

Financial Results:

Vedanta Ltd reported Revenues for Q1FY24 of ₹33,733.00 Crores down from ₹38,622.00 Crore year on year, a fall of 12.66%.

Total Expenses for Q1FY24 of ₹31,973.00 Crores down from ₹32,095.00 Crores year on year, a fall of 0.38%.

Consolidated Net Profit of ₹3,308.00 Crores down 40.85% from ₹5,593.00 Crores in the same quarter of the previous year.

The Earnings per Share is ₹7.10, down 40.29% from ₹11.89 in the same quarter of the previous year.

*It is important to note that the way the results have been accounted for are slightly different than the ones the companies may choose to publish.

*The presented data is automatically generated. It may occasionally generate incorrect information.