Key highlights from Tata Steel Ltd (TATASTEEL) Q3 FY22 Earnings Concall

Q&A Highlights:

- Amit Dixit of Edelweiss asked that in the long to medium term, what kind of sustainable EBITDA per tonne the company is looking from NINL and the reason for the seemingly aggressive bidding. T V Narendran MD replied that on NINL, the long-term EBITDA will depend on the steel prices and spreads. Look at the cost base and the size that it can come to, it can certainly produce long products at a much cheaper rate than Tata Steel Long Products is doing today.

- Amit Dixit of Edelweiss also asked about the coking coal costs incurred in Q3. Koushik Chatterjee CFO replied that the coal purchase cost in India in 2Q was about $167, which increased to about $269 in 3Q. And consumption cost, however, was about $230.

- Indrajit Agarwal of CLSA asked about working capital and how should it be looked at the unwinding of this working capital in the next few quarters. Koushik Chatterjee CFO replied that the company should come down to a more normalized level in the next couple of quarters because it’s seeing the volatility playing out over the next quarter or so because further coking coal price increase is expected in 4Q.

- Satyadeep Jain of AMBIT asked about capacity growth, where does capital return fit into capital allocation options looking beyond next year. Koushik Chatterjee CFO said that as for capital returns it’s very important for TATASTEEL, which is why internal capital is used to bring down the overall balance sheet risk significantly. And TATASTEEL certainly will be looking at higher return on invested capital going forward.

- Ritesh Shah of Investec enquired how should one look at the numbers on incremental capital allocation for Tata Steel Europe. Koushik Chatterjee CFO answered that the company is not going to allocate any capital into Tata Steel Europe or in Netherlands. Netherlands is self-sufficient. And the repair work for the blast furnace will also be funded internally over the next 2 or 3 years.

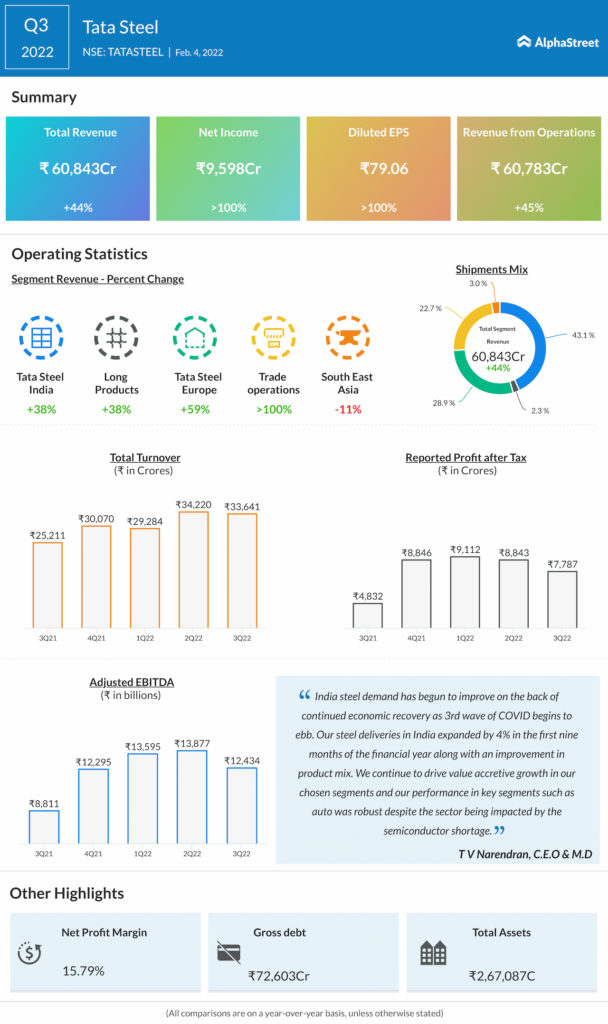

- Ritesh Shah of Investec asked about spreads for India and Europe, is the company confident of price increases to maintain similar levels of EBITDA given demand. T V Narendran MD said that as far as India, both Europe and India will see some impact of the input costs. The energy cost in Europe will be largely flat QonQ. As for realizations, in India there will be a QonQ reduction in the realization. And for margin, Europe seems positive, whereas in India, there would be a margin squeeze.

- Amit Murarka of Axis Capital asked about spot prices and general direction of realizations in Europe. T V Narendran MD replied that the spot market certainly is seeing a softening. But overall, TATASTEEL is guiding that 4Q22 will be about GBP15 to GBP20 per tonne higher than 3Q22. On realizations in Europe, TATASTEEL said that now the contracts signed are at higher than spot prices.

- Vishal Chandak with Motilal Oswal asked about what kind of capex the company is looking at Neelachal over the next 2 years’ time frame and the incremental capacities. Koushik Chatterjee CFO replied that first priority is to restart the current plant, which requires some amount of capex, which is going to cost a few hundred crores. So once it’s done, TATASTEEL is going to run the new plant on a parallel basis.

- Sahil Sanghvi of Monarch asked that considering the amount of acquisition, will it be all debt on the balance sheet or would TATASTEEL consider some rights issue also at Tata Steel Long Products. Koushik Chatterjee CFO replied that the company’s holding in Tata Steel Long Products is almost at the brink of the allowable level of 74.9%. So rights issue is not something that will come in very easily from SEBI perspective.

- Sahil Sanghvi of Monarch also asked that regarding the auto contracts when it comes to Tata Steel Long Products, has there been a revision and of what magnitude. T V Narendran MD replied that for H2 there’s been a revision of about INR6,000 for long products per tonne compared to the previous contracts.

- Samita Shah asked a chat question that on NINL in terms of funding the acquisition, the level of debt TATASTEEL will take and the way it will be funded. Koushik CFO said that the total enterprise value is INR12,100 crores, of which about INR 6,600 crores is going to go towards repayment for lenders, operational creators, employees etc. From a funding point of view, around 50% would be done through internal accruals of Tata Steel and 50% of bridge loans which the company will aim to prepay over the next few quarters.

- Samita Shah asked a chat question about the medium term pricing outlook on steel prices globally. T V Narendran MD said it believe that the steel prices going forward will be at a much higher level than seen in the last 10 years. It will continue to be volatile, as like last one year, but it will be volatile at a much higher level than seen in the last 10 years.