Being a global leader in IT services, digital, and business solutions, Tata Consultancy Services (NSE: TCS) aids clients in their business transformation. The company’s recent earnings report reflects strong profits and revenues, rising demand, and a robust cash position. Also, prudent cost management reflects operational efficiency. Additionally, to cater to the changing dynamics of the sector, TCS is on the path of aiding clients with solutions and expanding offerings in the software industry. Though competitive pressure and macro uncertainties loom, the company is focused on talent acquisition and retention to fulfill clients’ demands. Therefore, based on the company’s strong fundamentals, high returns, and long-term growth prospects, investors may build a position in the stock at the current level. Moreover, the company’s sound dividend policy makes it an attractive investment.

Overview

Headquartered in Mumbai, Tata Consultancy Services, an Indian multinational information technology services and consulting company, is a Large Cap company that operates in the IT Software sector. It is a part of the Tata Group and operates its business in 150 locations across 46 countries.

With a market capitalization of about Rs 11.23 lakh crore, TCS serves clients with IT services, consulting, and business solutions. As of September 30, 2022, the company has a workforce strength of over 616,000. It is listed both on the BSE (Bombay Stock Exchange) and the NSE (National Stock Exchange) in India.

Recent Share Price Insights

- With the current price of Rs 3,081, TCS depicts an upside potential of more than 30% compared to the high of its 52-week range of Rs 2,926.1 – Rs 4,043.

- The stock recorded a 3-year return of 54.49% as compared to the Nifty 100 return of 52.85%.

Financial Snapshot

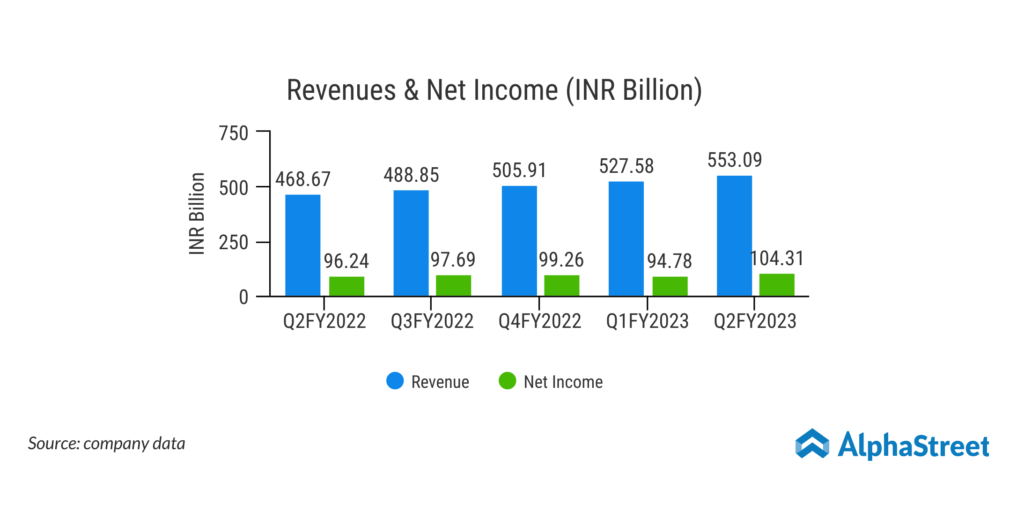

Recently, TCS reported revenues of Rs 55,309 crore in Q2 FY2022 (ended September 30), up 18% YoY driven by broad-based growth in all verticals. Revenues rose 15.4% YoY in constant currency terms.

Net profit attributable to shareholders came in at Rs 10,431 crore, up 8.4% on a YoY basis. Additionally, earnings per share (EPS) were Rs 28.51, up from Rs 26.02 in the prior-year quarter.

On a segment basis, growth was recorded in all segments. Banking Financial Services and Insurance, Manufacturing, Retail and Consumer Business, Communications, Media and Technology, and Life Sciences & Healthcare verticals grew 14%, 14%, 23%, 21%, and 21%, respectively.

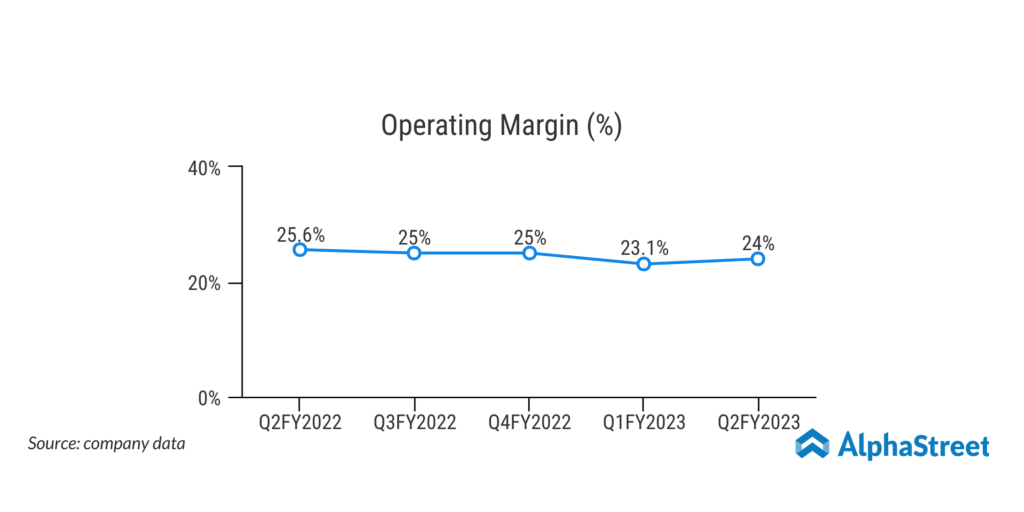

Total expenses stood at Rs 42,178 crore, up 20% YoY. The company depicted strong margins with net and operating margins at 18.9% and 24%, respectively, in Q2 FY2023.

As of September 30, 2022, total assets stood at Rs 1,48,173 crore compared to Rs 1,41,514 crore as of March 31, 2022. Cash and cash equivalents were Rs 5,834 crore, down 53% from the prior quarter. Operating cash flow came in at Rs 20,458 crore.

Commenting on the strong quarterly results, Rajesh Gopinathan, Chief Executive Officer and Managing Director of TCS said “Demand for our services continues to be very strong. We registered strong, profitable growth across all our industry verticals and in all our major markets. Our order book is holding up well, with a healthy mix of growth and transformation initiatives, cloud migration and outsourcing engagements.”

Looking forward, Samir Seksaria, Chief Financial Officer of TCS said, “We are steadily making our way towards achieving our operating margin priority for the year, aided by leverage from good growth, the flattening of the workforce pyramid, steadily improving productivity and currency support. Very importantly, the headwinds from the supply-side challenges are abating, so that sets us up well for the seasonally weak second half of the year.”

Analysts’ View Post Q2 Results

TCS reported upbeat Q2 results surpassing analysts’ expectations. However, some analysts remain skeptical about the company’s growth outlook due to a slowdown in deal conversion cycle indications on macroeconomic uncertainties.

Global brokerage Nomura analyst Abhishek Bhandari quoted, “There was no mega deal (>$500 million), had a few $400 million deals and most were small and mid-sized deals. TCS indicated that clients are taking longer than usual to close large deals given the macro uncertainty, leading to a lower proportion of qualified deals in the overall pipeline.”

Citi also reiterated a sell rating on TCS, while CLSA maintained an outperform rating with a target price of Rs 3,450.

On the flip side, Motilal Oswal said, “Given TCS’s size, order book, and exposure to long duration orders, and portfolio, it is well positioned to withstand the weakening macro environment and ride on the anticipated industry growth.”

From a valuation perspective, Mitul Shah, Head of research at Reliance Securities said, “We believe that IT Services would not remain immune to worsening global macros in terms of rising inflation, economic slowdown, currency headwinds and likely cut on spending. Revenue growth would taper down to a low double-digit in FY24E, while QoQ decline in order book, clear lower employee addition, higher attrition, and lower pricing power ahead would lead to valuation multiple contraction close to its historical averages. Therefore, at present, we have SELL rating on TCS.”

Factors to Consider

- Grabbing a high market share, TCS recorded strong revenue growth over the past five years with a CAGR of 10.2% in FY2022. The uptrend continued in the first six months of FY2023, which is expected to trend higher on strong demand.

- Earnings per share reflected an uptrend over the past five years with a CAGR of 9.2% in FY2022 riding on strong revenues. The rising trend continued in the first six months of FY2023. Continuation of such a trend will help the company to withstand economic downturns and macro uncertainties.

- Technology advancement is the key to success.

- Cost management reflects operational efficiency as margins recorded an uptrend over the past five years. The operating margin increased to 25.3% in FY2022 from 24.8% in FY2018. The uptrend continued in the recent quarters as well with some pressure in Q1.

- Sound dividend payouts and share buybacks over the last five years with an annual dividend yield of 1.4%.

- The company’s OCF and cash conversion remain strong. Remarkably, OCF to net profit ratio jumped to 104.2% in FY2022 from 97.1% in FY2018. The recent quarter recorded this ratio at 102.3%, reflecting the company’s prudent operational management.

- With the current LTM attrition at 21.5% in IT Services, the company depicts strong talent retention. The attrition is expected to reduce in the second half of FY2023.

- Despite strong demand from clients, signals of a slowdown in deal conversions, mainly in high-value, is a concern.

- Competitive pressure.

Recent Highlights

Recently, TCS Mobility Cloud Suite, a rich toolbox of cloud-enabled software, was launched by the company. It will aid automotive manufacturers and suppliers to readily adapt to changes in their industry and expand their ecosystems at a fast pace.

Also, TCS jointly with SIA Engineering Company (SIAEC) has launched SmartMx (Smart Maintenance). This is a part of the TCS Aviana suite. The new solution will help airlines and Maintenance, Repair, and Overhaul (MRO) service providers to improve their operations digitally. Notably, SIAEC is a major provider of aircraft MRO services in the Asia-Pacific.

Industry Analysis

The booming IT industry contributed 8% to India’s GDP in 2020, which is forecast to contribute 10% by 2025. On rising demand for talent and skill, top industry players in this well-diversified sector across retail, telecom, and BFSI, have created job opportunities in the sector to a high level. Remarkably, Indian IT firms, who have delivery centres internationally, are increasing strategic alliances between domestic and global players to serve clients with their solutions worldwide. Though the industry is facing some challenges due to global hues, India’s IT and business services market is expected to reach $19.93 billion by 2025.

Peer Comparison

In terms of market capitalization, TCS ranks much higher than its peers. Based on the dividend-yielding nature of the company and strong ROE, investors can consider TCS an attractive investment, despite it seeming overvalued at the current level compared to its industry peers.