“I am happy to report that our hospital business continued to deliver consistent performance in all key operational and financial parameters with surgery count and In-patient count (Including day care) grew by 19% and 15% Y-o-Y respectively in Q3 FY23. Hospital revenue and EBITDA also grew by 17.4% and 23.5% Yo-Y with robust EBITDA margin of 21.5% in Q3 FY23”.

– Mr Shanay Shah, President, Q3FY23 Concall

Stock Data:

| Ticker | SHALBY |

| Exchange | NSE and BSE |

| Industry | Healthcare |

Price Performance:

| Last 5 days | 10.9% |

| YTD | -4.2% |

| Last 1 year | 10.2% |

Company Description:

Shalby Ltd. is a leading chain of multispecialty hospitals and tertiary care centers in India. In the Hospital business, the company possesses 11 multispeciality hospitals with close to 2060+ beds. The company also operates in the knee and hip implant manufacturing business which is located in California, USA. Additionally, the company has forayed into the home care services segment to provide healthcare services to patients at the comfort of their own home.

Hospitals Portfolio:

Presently, the company operates 11 hospitals across India with a total bed capacity of ~2,100 beds. It also owns 50 outpatient clinics across 15 states in India and 5 OP clinics in African Countries. It undertook aggressive expansion and has operationalised 6 new hospitals since FY15. It also has 2 hospitals under construction.

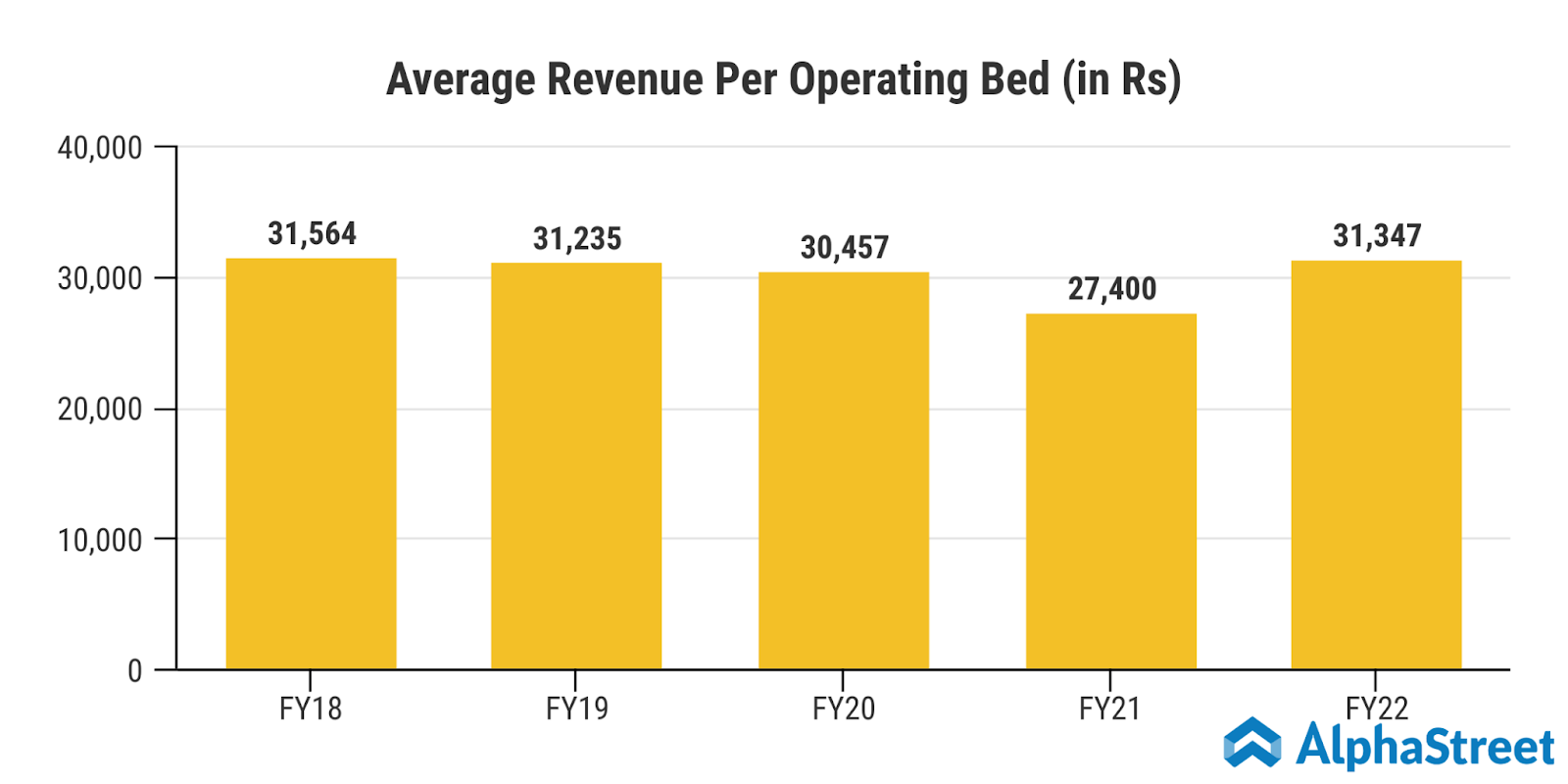

Occupancy Levels and Average Revenue Per Operating Bed:

Occupancy levels for FY19, 20, 21 are 37%, 38% and ~36% respectively. ARPOB also fell from ~30,500 in FY20 to 27,500 in FY21 primarily due to a fall in surgeries done by the company.

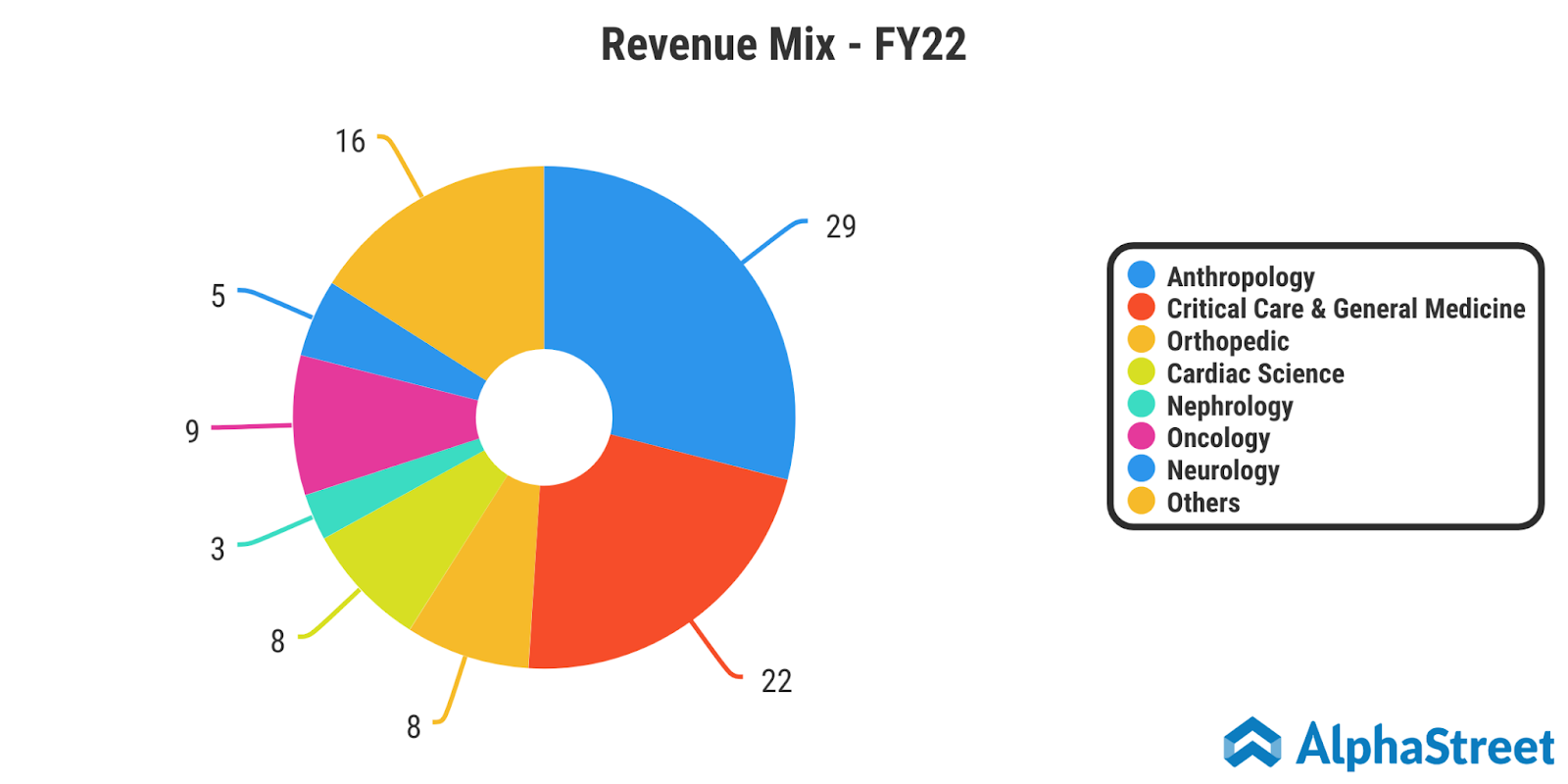

Diversification:

The company has been diversifying from its specialty field and non-arthroplasty (joint replacement) segment contributed ~55% of total revenues of the company in FY20.

The revenues from arthroplasty dropped to ~23% in FY21 primarily due to decrease in surgeries due to COVID-19.

Revenue Concentration from Flagship Hospital:

The company derives most of its revenues from its flagship hospital at SG Highway in Ahmedabad, Gujarat. It accounted for ~33% of total revenues of the company in FY20.

Acquisition of Implant Business in USA:

On May 21, the company acquired implant assets in the form of plant, property and equipment, inventory and patents from Consensus Orthopedics for INR ~80 crores. From this acquisition, the company has achieved backwards integration for its Arthroplasty business.

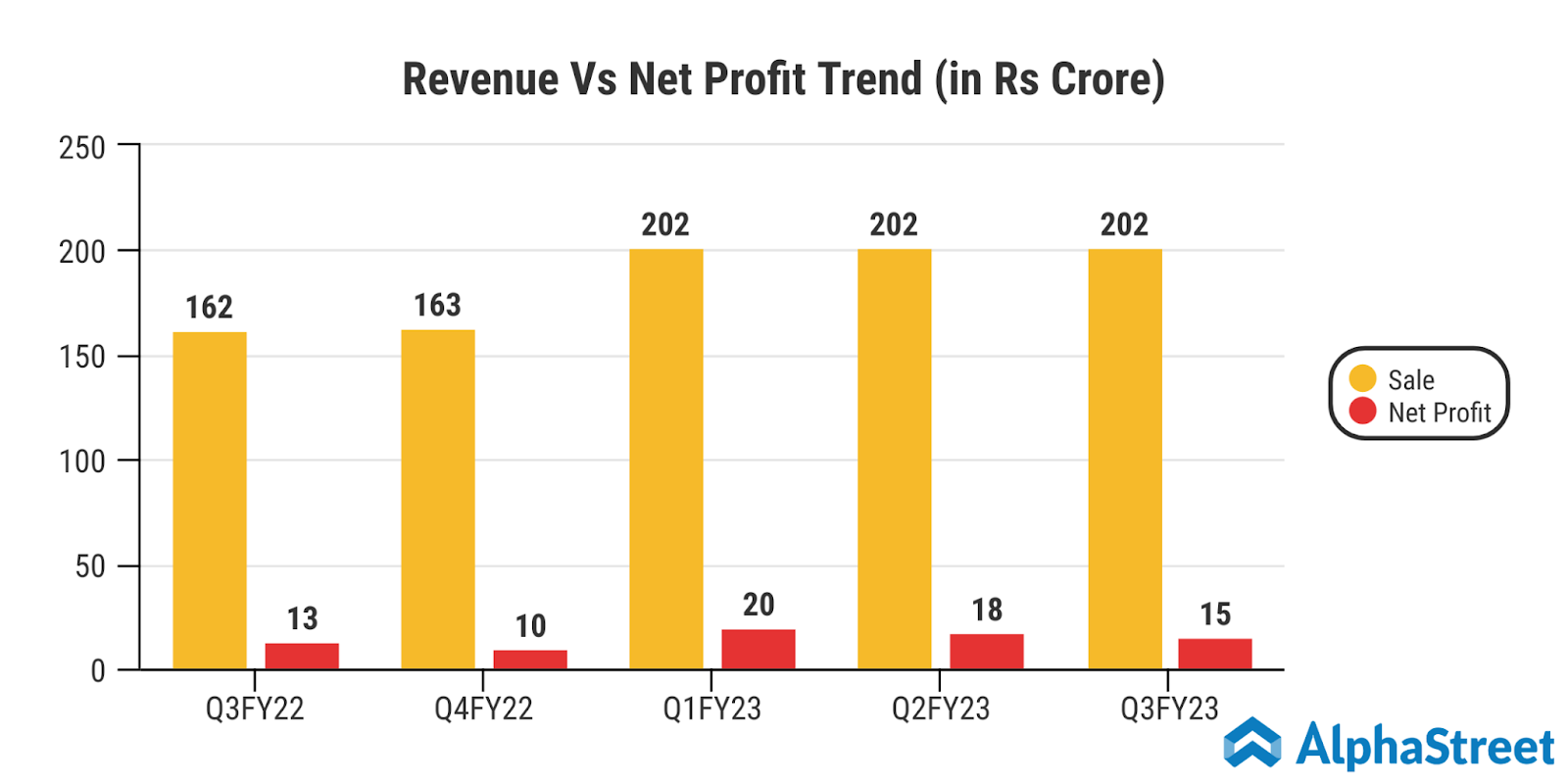

Financials:

What we like:

- Dominance in Arthroplasty & Implant Business:

Arthroplasty is an orthopedic surgical procedure to restore the function of a joint. The common type of Arthroplasty is hip, knee and shoulder replacement. Shalby Ltd. is the largest private player in the Arthroplasty segment in India with about 15% of the total market share.

To further increase the firm’s dominance in this segment, the company acquired an implant manufacturing business. Other than the fact that this move allows backwards integration of the Arthroplasty segment, the company majorly sells these manufactured goods in the USA where the margins for the goods are significantly higher than the Southeast Asian markets.

In the implants business, the company is looking to directly reach retailers rather than wholesalers to earn a higher margin. As operations in this segment increases, economies of scale would result in steady profitability in the business. Additionally, the backwards integration would benefit the hospital business as well.

- Asset Light Model (Strategy):

Shalby Ltd. has always followed an asset light model. In the hospital business, 4 of its 11 multispeciality hospitals are leased properties. This asset light strategy allows the company to diversify swiftly and expand aggressively.

In the Franchise business, the company is extending its management control over the franchised hospitals. By managing the hospitals, Shalby Ltd. will take a larger portion of the revenues for itself.

- Steady & Profitable Hospital Business:

A major profitability driver for the firm is its hospital business. This quarter, the average revenue per occupied bed (ARPOB) decreased but the occupancy rate as a whole has gone up to 50% in Q2FY23 from 43% in Q2FY22. The management estimated that by the end of this fiscal year (FY23), the occupancy will increase to 53% – 54% levels. This increasing trend in the occupancy rate will result in increasing revenues for Shalby Ltd.

- High Upside Potential with the Home Care Division:

The Shalby Homecare Services represents a small portion of the Shalby Ltd. group. However, it comes with great potential. Post the COVID 19 pandemic, there has been an increasing trend of homecare services. A key benefit of homecare services is that patients prefer to keep on working with the same entity if the need arises. So, the customer of the homecare services of Shalby Homecare Services is likely to use the Shalby Multispeciality Hospital for their additional medical needs. This characteristic might also stand as an obstacle for the firms in this segment to snatch market share from each other. Shalby Homecare Services has planned an impressive service offering which it wants to roll out eventually in the future.

Factors to consider:

- Loyalty among suppliers is low. Given the history of Shalby coming up with new innovations to drive down prices in the supply chain.

- Niche markets and local monopolies that companies such as Shalby are able to exploit are fast disappearing. The customer network that Shalby has promoted is proving less and less effective.

- Business Model of Shalby can be easily imitated by the competitors in the Healthcare Facilities industry. To overcome these challenges companyname needs to build a platform model that can integrate suppliers, vendors and end users.

- High turnover of employees at the lower levels is also a concern for the Shalby . It can lead to higher salaries to maintain the talent within the firm.

- High cost of replacing existing experts within the Shalby. Few employees are responsible for the Shelby’s knowledge base and replacing them will be extremely difficult in the present conditions.

Industry Analysis and Conclusion:

The demand for hospital services has consistently increased throughout the country, with every class of society expecting higher quality and standards of healthcare, resulting in the healthcare industry’s continuing growth. Due to increased occupancy, improved patient mobility as a result of “living with COVID-19” rules, and the resumption of non-COVID procedures, the hospital industry revenue is estimated to grow by 15% for FY 2021-22 according to CARE Rating Research. While in FY 2020-21, the hospitals reported modest revenue growth of 7%, mainly because lockdowns were imposed, this had an impact on patient mobility and delayed non-COVID procedures.

For the years FY 2022-23 and FY 2023-24, the occupancy rates are anticipated to return to pre-COVID levels at 64% and 65% respectively. The significant improvement in revenue is being driven by a higher occupancy rate, the release of postponed non-COVID surgeries, an increase in ARPOB, and increased bed capacity on the part of hospital chains. In FY 2022-23 and FY 2023-24, respectively, it is anticipated that growth in hospital revenue will return to pre-COVID levels of 10% to 12%.