Schneider Electric Infrastructure (Ticker: SCHNEIDER), founded in 2011, designs and manufactures products used for the electricity network including transformers and controllers. The company has manufacturing facilities in Chennai, Kolkata, and Vadodara. The company also offers asset advisory and maintenance services, which accounts for 10% of total revenue.

Q1 Earnings

Schneider Electric Infrastructure Limited reported a net profit of 27 crores, up from 16 crores loss in the same quarter last year. Additionally, the business reported a double-digit, year-over-year sales growth of 28.9%. Sales increased to 371.5 crore from 288.2 crore as a result of increased power demand for electricity generation and distribution as well as demands in the mining, mineral, and metal segments. The EBITDA margin was 7.9%, compared to negative margins in the same quarter last year.

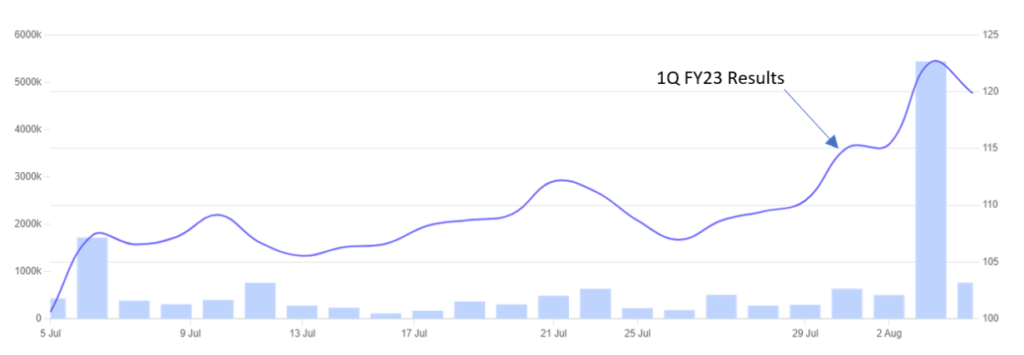

Price Performance

The company’s share price increased by more than 8% as a result of the company’s double-digit sales growth year over year. The volumes significantly increased on August 3rd, indicating that investors had a strong buy sentiment.

Last 5 Days: 2.5%

Last 1 month: 10.3%

Last 6 months: 11.5%

Strong demand in end markets

Power & Grid, Transportation, Minerals, Mining & Metals, and Oil & Gas are the company’s four most important segments, and they all are electro-intensive. The demand in the Power & Grid segment has a positive outlook owing to rising demand for electricity generation and distribution as India expands its digital footprint. The popularity of digital entertainment and education, as well as digital payments like UPI, will further boost demand for the company’s products in this segment.

The minerals, mining, and metals also stand to benefit from the positive trend in the construction sector, with housing construction and bookings rising from last month. Future orders should be solid as the capacities for steel and cement increase. For the next three to five years, we should continue to see investments in metros and airports because India trails behind in terms of transportation infrastructure. There have been numerous petrochemical facilities built in the Oil and Gas segment. However, compared to the other segments, the demand from the Oil & Gas segment is lower.

The company’s revenue in the upcoming quarters should be driven by its strong ability to meet these end-market demands.

Long Term strategy

The long-term strategy of SEIL is to focus more on services to generate recurring revenue and to become more digital by incorporating software products. Additionally, the business wants to accelerate its core markets, expand its coverage across the nation through licensee partner models, and bring green products to market.

As per the management, “Just to bring about a flavor of how we are going ahead and executing our strategy. Leading with software, I spoke about it as one of our key strategic priorities; we continue to stay invested here. Here is an example of an atomic R&D center in Vizag that we have just completed. It uses our EcoStruxure for grid platform, which is the EPAS platform to be able to provide instant fast load shedding to the customers. We work very intricately with the customer connecting all their medium voltage products and providing them with the relevant software interface to be able to take informed decisions.”

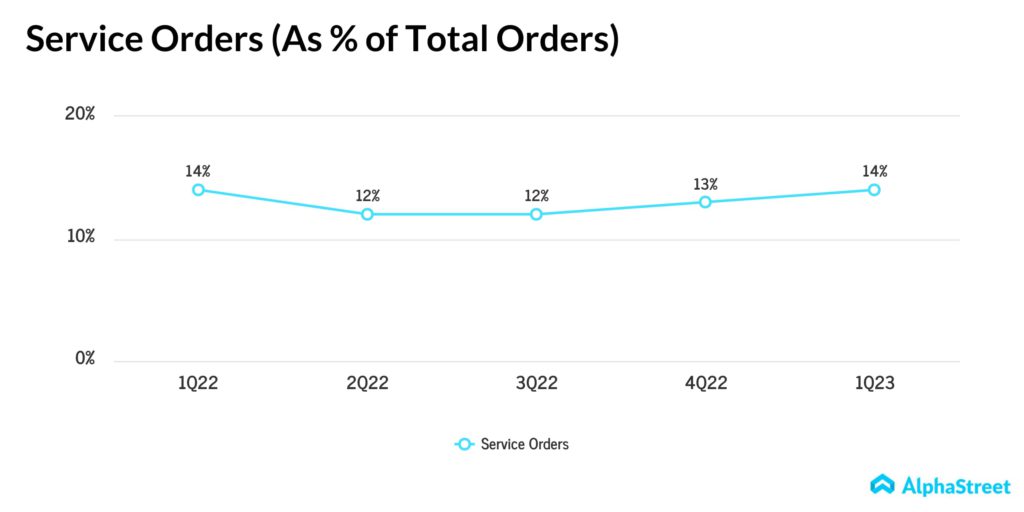

In terms of the service and recurring revenue, the company has already put it into practice by providing 24/7 monitoring and predictive maintenance to a leading government hospital chain, enabling them to make well-informed decisions. The graph below, however, shows that the contribution of services to total orders has not increased significantly. If the SEIL makes the necessary developments to this strategy, it ought to have a long-term beneficial effect on the expansion of the business.

Schneider Electric’s High Debt

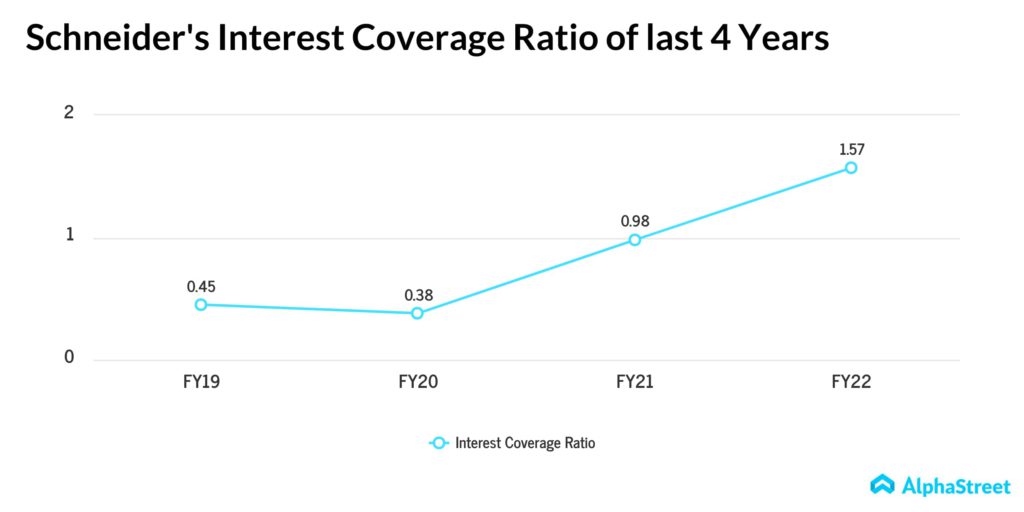

The company’s long-term debt increased by more than threefold between March 2018 and March 2022, from about 107 crore to 393 crore. However, from the below chart, it is clear that the company’s interest coverage ratio is getting better over time. Additionally, according to the management, no significant Capex has been decided upon as of yet. Over time, the amount of debt should decrease if the interest coverage ratio steadily improves and the company lowers borrowing for business expansion.

Our View

The company’s end markets are rapidly growing, which should in turn drive revenues. Additionally, SEIL is committed to their long-term plan, which will aid in the expansion of the business. Moreover, for the first time in the last four years, the interest coverage ratio exceeds 1. The continuous improvement in this ratio and no major Capex at this time should reduce the company’s debt burden.