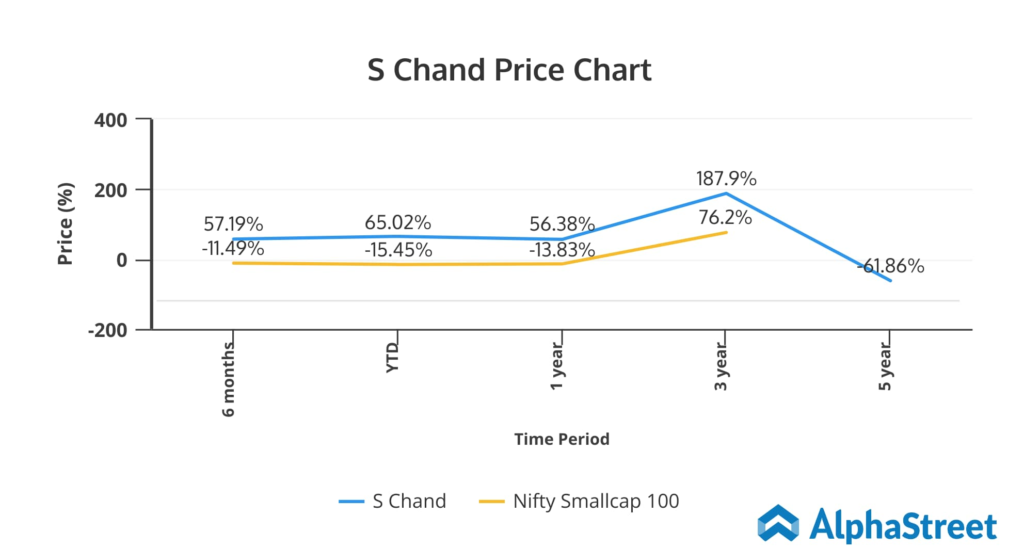

S Chand & Co Ltd (NSE: SCHAND) has outperformed its peers by providing a one-year return of around 58%, significantly up when compared to its peers such as Navneet Education Ltd (NSE: NAVNETEDUL) and Jagran Prakashan Ltd (NSE: JAGRAN), among others.

Also, the stock recorded a 3-year return of 187.9% as compared to the Nifty Smallcap 100 return of 76.2%.

Headquartered in New Delhi, the company is one of India’s oldest and largest publishing and education services companies. The company prints books for primary, secondary, and higher education sectors. This Smallcap company holds a market cap of about Rs 641.82 crore and is listed on both NSE and BSE.

Due to the pandemic, the publishing industry was marred to a large extent by the closure of schools, colleges, and other shutdowns. Post-pandemic, the reopening of schools and colleges, along with other institutions spurred demand strongly for the industry. As a result, S Chand has emerged triumphant with substantial quarterly numbers in Q1 FY2023 riding on a rise in sales coupled with higher profits on a year-over-year basis.

Factors to Consider

Operating revenues were almost three times of revenues recorded in the prior-year quarter. Also, the company returned to profits in FY2022 and in the first quarter reflecting positive EBITDA and the first-ever PAT in the company’s history in the quarter.

Though the hike in paper prices escalated costs, the company has maintained its margin levels prudently. Interestingly, S Chand recorded 6.5 times jump in operating cash flows in Q1 over the same period last year.

Looking forward to FY2023, the company has planned to mitigate the rise in paper prices through price hikes across its product portfolio, along with cost-effective measures, better realizations, and internal efficiencies. It forecast annual revenues of Rs 600 crores, reflecting a growth of 25%.

On the debt front, with the decreasing level, the company targets to be debt-free by Q4 FY2023. Also, total inventory levels are consistently decreasing, which mirrors a strong demand-supply balance.

The company is optimistic about its financials going forward. Additionally, the announcement of the National Curriculum Framework (NCF), expected this calendar year, is anticipated to boost the company’s revenue and profitability over the next two to three years.

Our View

In the evolving world, strong business momentum guided by new products, operational efficiency, robust sales, reduced debt, and strong cash flow, is likely to aid the company’s financials. As a result, based on the stock’s upside potential and returns, investors might consider the stock an attractive investment opportunity. Also, from a valuation perspective, based on a P/B ratio of 0.80, the stock seems currently undervalued compared to its industry peers.