Larsen & Toubro Limited (NSE: LT) is one of India’s largest companies operating in the Technology, Engineering, Construction, and Manufacturing industry. L&T is a market leader in almost every industry it competes in. The company’s technological prowess is a strategic mix of internal R&D and the knowledge of its joint venture partners. In Q2 FY23, the company improved in almost all major business segments.

L&T’s Financial Performance in Q2FY23

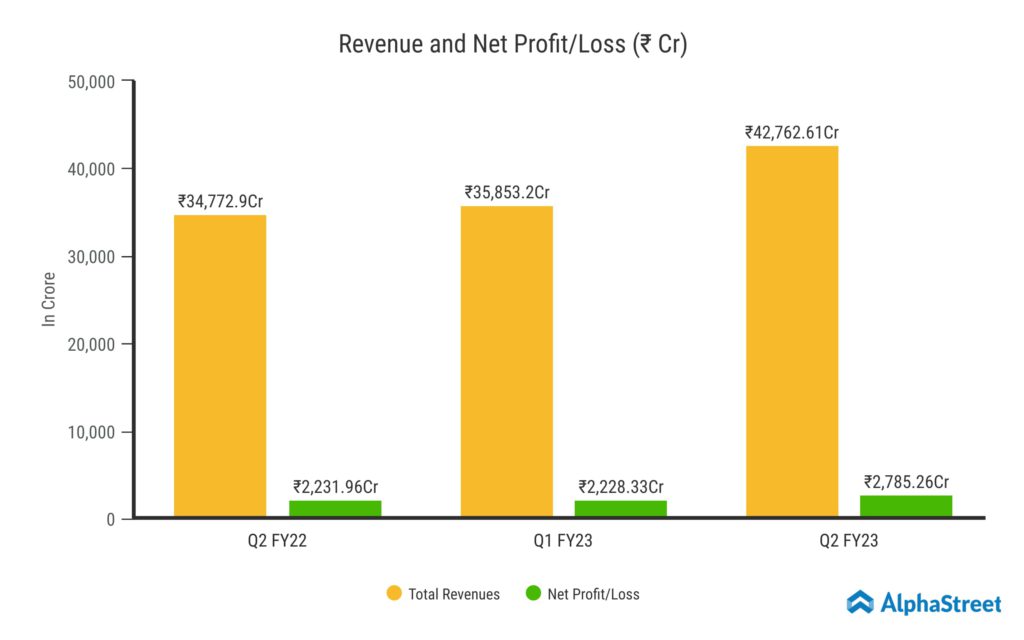

Larsen & Toubro Limited reported Revenue from Operations for Q2 FY23 of ₹42,762.61 Crore up from ₹34,772.9 Crore year on year, a growth of 24.7%. The Revenue was driven by Infrastructure segment which surged by 38.9% up to ₹18,476.45 Crore. Consolidated Net Profit of ₹2,785.26 Crore, up 25% from ₹2,231.96 Crore in the same quarter of the previous year. The Earnings per Share is ₹15.85 for this quarter. As of September 2022, L&T’s order book is at a record high of ₹3.72 trillion, of which 72% was domestic and 28% was foreign.

Order Inflows for L&T in Infrastructure Segment

In Q2 FY23, Revenues for the Infrastructure segment reached ₹193.7 billion, up 39% from the previous year. It was due to the combination of a large opening order book and improved customer collections during the quarter. However, this segment’s EBITDA margin fell 170 basis points to 6.6% in this quarter. The current high energy prices, higher percentage of cost jobs along with cost pressures in certain jobs impacted the margins. The procurement orders were placed before the correction happened in the commodity prices, which increased the input costs to some extent.

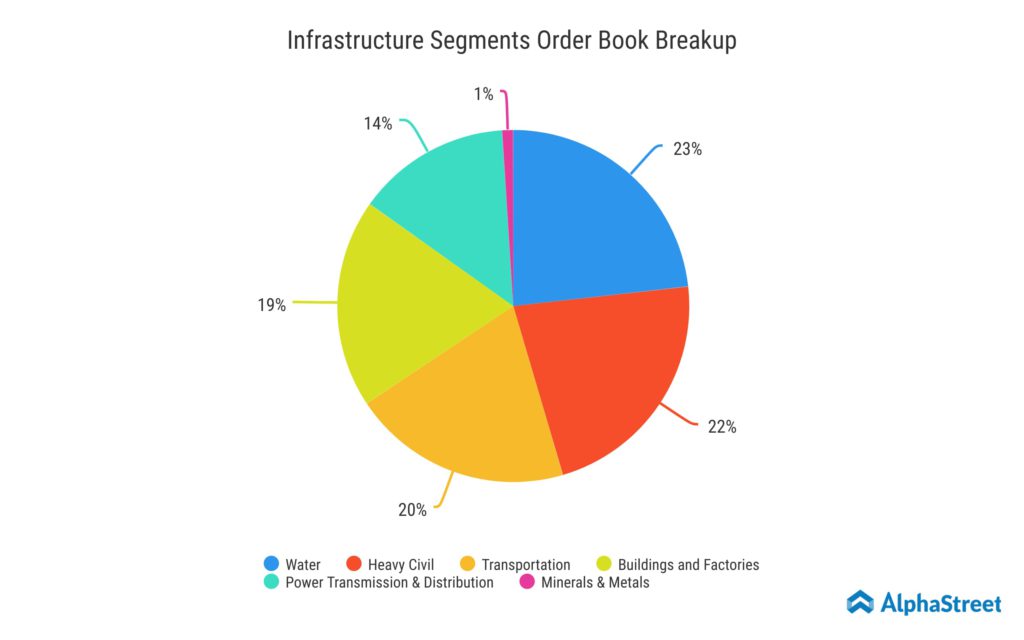

In Q2, the Infrastructure segment received orders worth ₹251 billion, a significant increase of 107% from Q2 of the previous year. This quarter’s order inflows are evenly distributed across a number of sub-segments.

Decline in L&T’s Energy & Hi-Tech Manufacturing Segment

In this quarter, the Revenue for the Energy Project segment dropped by 7% to ₹55.9 billion. The decline in revenue was caused by the segment’s depleting order book. However, this segment’s EBITDA margin increased to 8.5% for Q2 FY23 from 6.6% for the same quarter last year. As of September 22, the Energy segment’s order book totalled ₹689 billion, with 54% of that amount coming from international customers, who are primarily in the hydrocarbon industry. This segment accounts for 13% of the company’s total revenue. Decline in its revenue should pullback the top line growth.

For Q2 FY23, the Hi-Tech Manufacturing segment’s Revenue decreased by 1% to 14.6 billion. Lower international orders caused the segment’s revenue to plunge. For International orders for this quarter is ₹3.2 Billion compared to ₹4.1 Billion for the same quarter previous year. While defense ordering was subdued in this quarter, heavy engineering saw multiple order wins.

Updates in IT TS & Financial Services Segment

The Revenues for IT & TS segment in Q2 FY’23 is at ₹101.5 billion registered a growth of 29% over the corresponding quarter of the previous year. This increase was due to the continuing growth momentum for in demand for technology-focused offerings. However, the EBITDA margins in this segment was shrunk by increase in wage costs, which were partly offset by favourable movement in the dollar-rupee and other improved operational efficiencies. According to the management, the merger of LTI and Mindtree, two of its subsidiaries, should be finished before the end of this year.

Meanwhile, the Finance segment posted a growth in Revenue of 6% up to ₹31.5 billion in this quarter. During Q2 FY23, the Net Interest Margins were improved along with improved fees, lower credit costs, better asset quality and a thrust towards retailization of the book. As of September 22, the share of retail in the overall book is at 58%.

Improvement in L&T’s Development Project Segment

The Revenues for this segment is at ₹17 billion, with a growth rate of 24% from ₹13.8 billion in same quarter previous year. This segment currently includes the Hyderabad Metro and Power Development business of Nabha Power which is a major Revenue contributor of this segment. Improved ridership in metro and higher PLF in Nabha drive the revenue growth for this segment in this quarter. The daily average for metro ridership increased from 1,46,000 in Q2 FY22 to 3,55,000 in Q2 FY23. Due to the increase in average daily ridership, metro was able to report an EBITDA margin of 39% in Q2 FY23 as compared to 13% in Q2 of the previous year. The consolidated Net Loss improved to ₹3.28 billion compared to the loss of ₹4.47 billion in Q2 of the previous year.