FY24 has started on a promising note. Our focus on expanding our value-added portfolio and operational efficiencies has enabled us to deliver a sustained performance in the face of continued macroeconomic pressures. An enhanced product mix saw the Aluminium India Downstream Business generating higher value, with Q1 EBITDA increasing by 31% QoQ. Despite significant market headwinds, Novelis continued to show sequential improvement in adjusted EBITDA and EBITDA per ton, backed by record sales of automotive aluminium sheets. The Copper Business achieved record metal sales and maintained its market share despite undergoing a planned shutdown.”

Satish Pai, Managing Director

Stock data

| Ticker | HINDALCO |

| Exchange | BSE and NSE |

| Industry | Non Ferrous Metals |

Price Performance:

| Last 5 days | -1.54% |

| YTD | -6.20% |

| Last 1 year | +8.27% |

Company description:

Incorporated in 1958, Hindalco Industries Ltd. is a flagship company of the Aditya Birla Group. The company and its subsidiaries are primarily engaged in the production of Aluminium and Copper. It is also engaged in the manufacturing of aluminum sheet, extrusion and light gauge products for use in packaging markets like beverage and food, can and foil products, etc.

Business Segments:

- Aluminum: The company ranks among the top global five aluminum producers based on shipments and is an integrated producer with a low-cost base and a strong presence across the value chain.

- Copper: The company’s copper division operates one of the world’s largest single-location customs copper smelters. Hindalco produces copper cathodes, and continuous cast copper rods in various sizes.

- Chemicals: Hindalco is also engaged in the manufacturing of Calcined alumina (used in grinding media, wear-resistant ceramic components, etc.) and Alumina hydrates (used in the manufacture of water treatment chemicals like aluminium sulphate, zeolite, etc.)

Market Leadership:

The company is the world’s largest aluminium rolling and recycling company. It is also one of Asia’s largest producers of primary aluminium. Moreover, it is the largest flat rolled aluminium producer in the world and the largest downstream aluminium player in India.

Novelis:

Novelis is a subsidiary of Hindalco Industries Limited producing automotive and beverage can sheets. It operates an integrated network of technically advanced rolling and recycling facilities across North America, South America, Europe and Asia.

Manufacturing Capabilities:

The company has 52 manufacturing units spread across 10 countries. It has 17 units in India, 19 operational bauxite mines, and 33 overseas units of Novelis.

Revenue Breakdown:

In Q1FY24, Novelis accounted for 61% of the total revenue earned by the company, followed by aluminum accounting for 19% of the revenue and copper for the remaining 20%.

Production Capacity (in MN MT):

Alumina – 3.6

Specialty Alumina – ~0.4

Primary Aluminum – 1.3

Aluminium VAP – ~0.4

Copper Cathode – 0.4

Copper Rods – 0.5

Novelis Rolling Capacity – 4

Novelis recycling capacity – 2.5

Expanding Geographical Footprint:

The company has expanded its scale by acquiring Kuppam facility at Rs. 247 crore of enterprise value and Ryker Base Private Limited, now Asoj at an enterprise value of Rs. 323 crore

Capacity Expansion:

In FY22, the company completed its 500 kt Utkal’s Alumina refinery brownfield capacity expansion which required a capital outlay of Rs. 1,500 crores. Further debottlenecking is planned at Utkal Alumina by 350 kt to take the capacity to around 2.5 Million MT by FY24. Additionally, it has started to expand the FRP production capacity at Aditya Aluminium and Hirakud plants by 170 KTPA with a planned investment of about Rs. 2,690 Crore. The plants at Aditya and Mahan are due to get an 18-pot expansion each at a cost of Rs. 417 Crore and Rs. 429 Crore.

Investments:

Hindalco has invested Rs. 609 Crore in Silvassa to build new extrusions plants with a planned capacity of 34 KTPA. The company has announced certain organic growth investments in India in the businesses of Aluminium, Copper, Specialty Alumina and also Resource Securitisation over the next 5 years in the range of $3.0 – 3.3 billion. Novelis has identified more than $4.5 billion of potential capital investment opportunities in new capacities and facilities. The new facilities will be established in the US, China, South Korea, Germany, and Brazil. Of the estimated range of total investments, ~$3 Billion is expected to be invested in the US.

Renewable Energy Target:

At present, the company has a total renewable capacity of 100 MW. It intends to achieve a renewable capacity of 300 MW by FY2024-25, including 100 MW solar power capacity with hybrid storage.

Fund Raising:

In March 2021, Novelis Inc. announced the completion of €500 million aggregate principal amount of 3.375% euro-denominated senior green notes due April 15, 2029, by Novelis Sheet Ingot GmbH, an indirect wholly-owned subsidiary of Novelis.

Further, in July 2021, Novelis Inc. raised $750M principal amount of its senior notes due in 2026 and $750M aggregate principal amount of its senior notes due in 2031.

Focus:

The company continues to focus on its downstream strategy to increase its downstream capacities in the Flat Rolled Products, Extrusions and other flat rolled products.

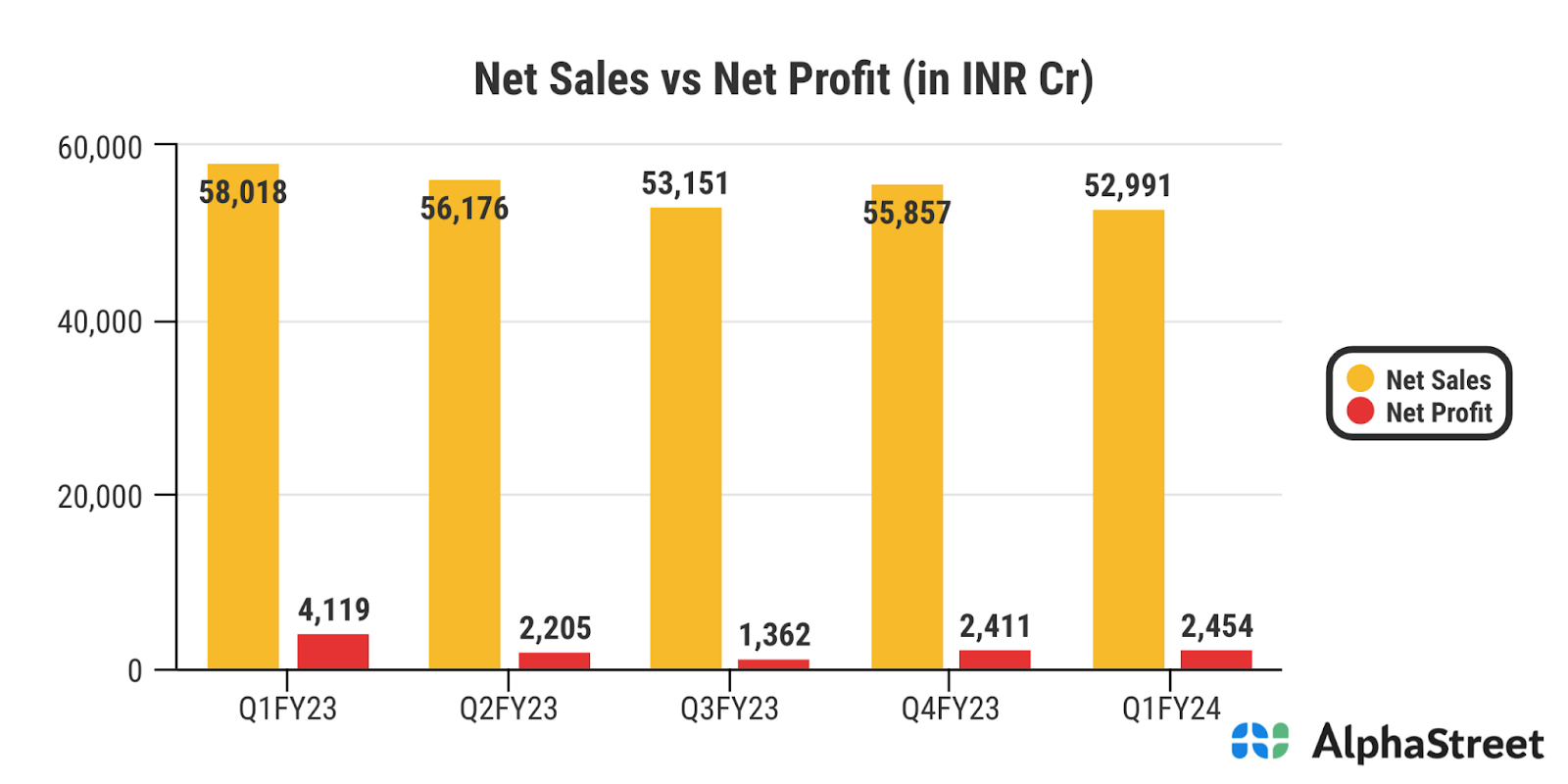

Financials:

What we like:

- Diversified Product Portfolio:

Hindalco Industries operates in both the aluminum and copper industries, providing diversification across different metals. This diversification can help mitigate risks associated with fluctuations in commodity prices. When aluminum prices are low, favorable copper prices can help balance the overall revenue and profitability.

- Global Operations and Subsidiaries:

Hindalco has a global presence through its subsidiaries like Novelis, which is a leading producer of rolled aluminum products. This global reach allows the company to tap into international markets and potentially reduce its dependence on any one specific region’s economic conditions.

- Vertical Integration and Value-Added Products:

Hindalco’s vertical integration, from mining and refining to downstream manufacturing, provides control over its supply chain. This integration can lead to cost efficiencies and better margin management. Additionally, Hindalco’s focus on producing value-added products, such as flat-rolled products and extrusions, can lead to higher margins compared to basic metal production.

- Infrastructure Development:

As India continues to invest in infrastructure development, there will likely be increased demand for aluminum and copper products in construction, transportation, and power sectors. Hindalco is well-positioned to benefit from this trend by supplying essential materials for these projects.

- The company is priming for growth and cost reduction:

Growth projects at both Novelis and India operations are on track with:

- Bay Minette plant likely to commence operations from FY26.

- Rolling volumes from India are likely to increase by 170kte by Q1FY25.

- 34 ktpa extrusions capacity at Silvassa has commenced operations.

- 350 ktpa debottlenecking at Utkal is in progress. In India, Aluminium upstream is expected to decline further in line with lower e-auction prices and linkage share at 60%. In captive coal mining, progress on Chakla mine is proceeding well with box-cut likely in Oct ’24. Recently, the company also won MeenakshiEast mine (6-7mtpa), which too will aid in further coal security.

Factors to consider:

- Energy inflation worsening or sustaining for longer can affect the company’s profitability

- Demand conditions worsening can also affect the bottomline of the company.

- Delay in ongoing expansion can lead to an increased OPEX and delayed capacity utilization. This can also affect the company’s growth.