About Company:

Started in the late 1990s, IndiaMART is India’s largest online B2B marketplace. It connects buyers and sellers of products and services. It provides ease and convenience to the buyers by offering a wide assortment of products and a responsive seller base while offering lead generation, lead management and payment solutions to its sellers.

Let’s delve deeper into its revenue model:

Revenue Model:

The company’s revenue primarily comes from providing subscription based offerings to the suppliers. While most of the suppliers register themselves free on the platform, the company generates revenue through monetization of a small number of our total suppliers by sale of subscription packages. The packages are classified under Silver, Gold and Platinum categories and are offered on monthly, semi-annual, annual and multi-year basis. The packages include providing a web storefront, cloud telephony services, priority listing, RFQ selection credits (BuyLeads), customer relationship management through a lead manager, facility for online payment and better profile information of the prospective buyers.

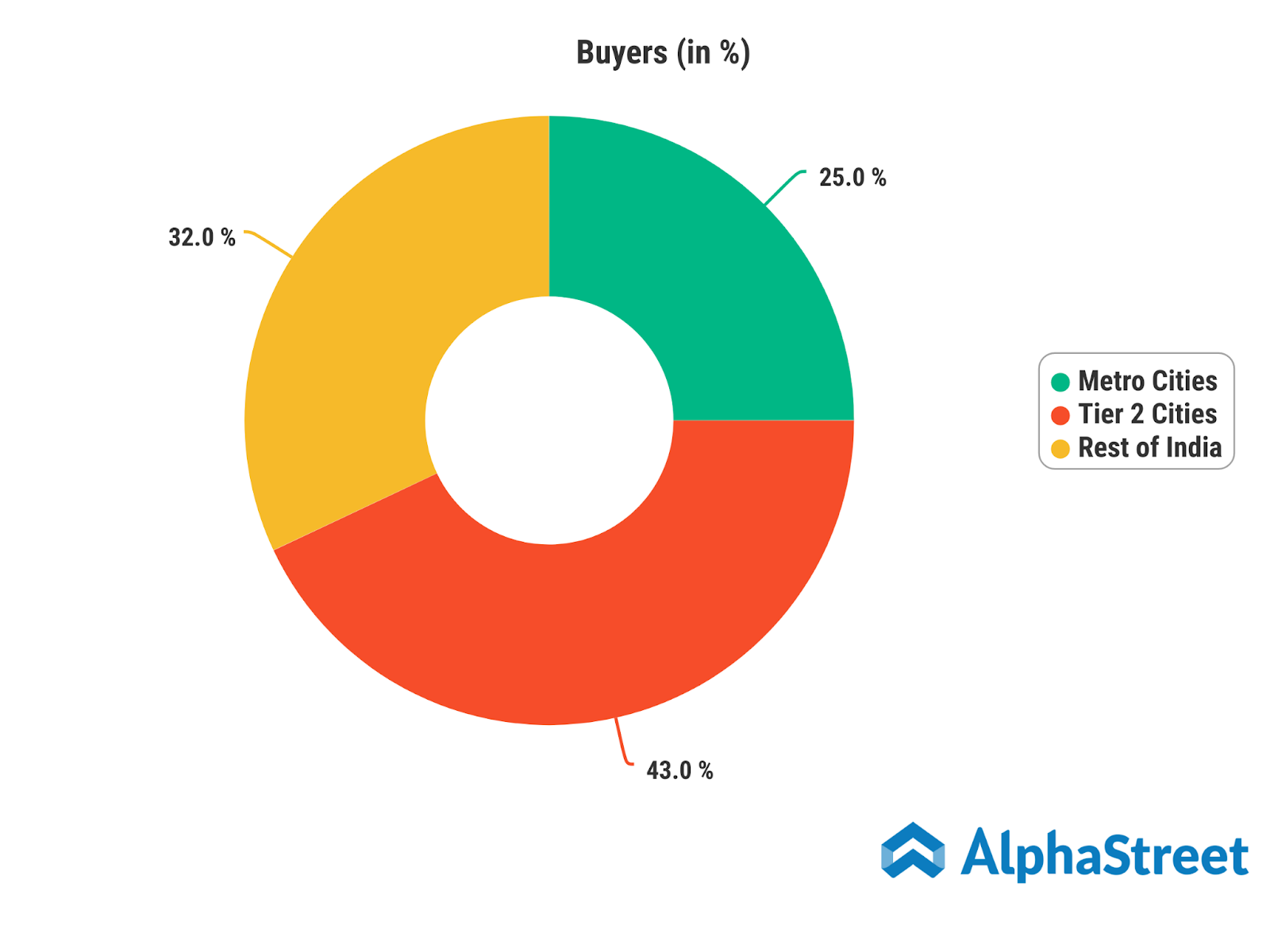

Pan India presence:

The company has been diversifying its presence and now the Metro cities account for 32% of buyers while tier-2 cities account for 25% & rest of India accounts for 43% of the total buyers.

The diversified presence helps to minimize the impact of region-specific risks on its business.

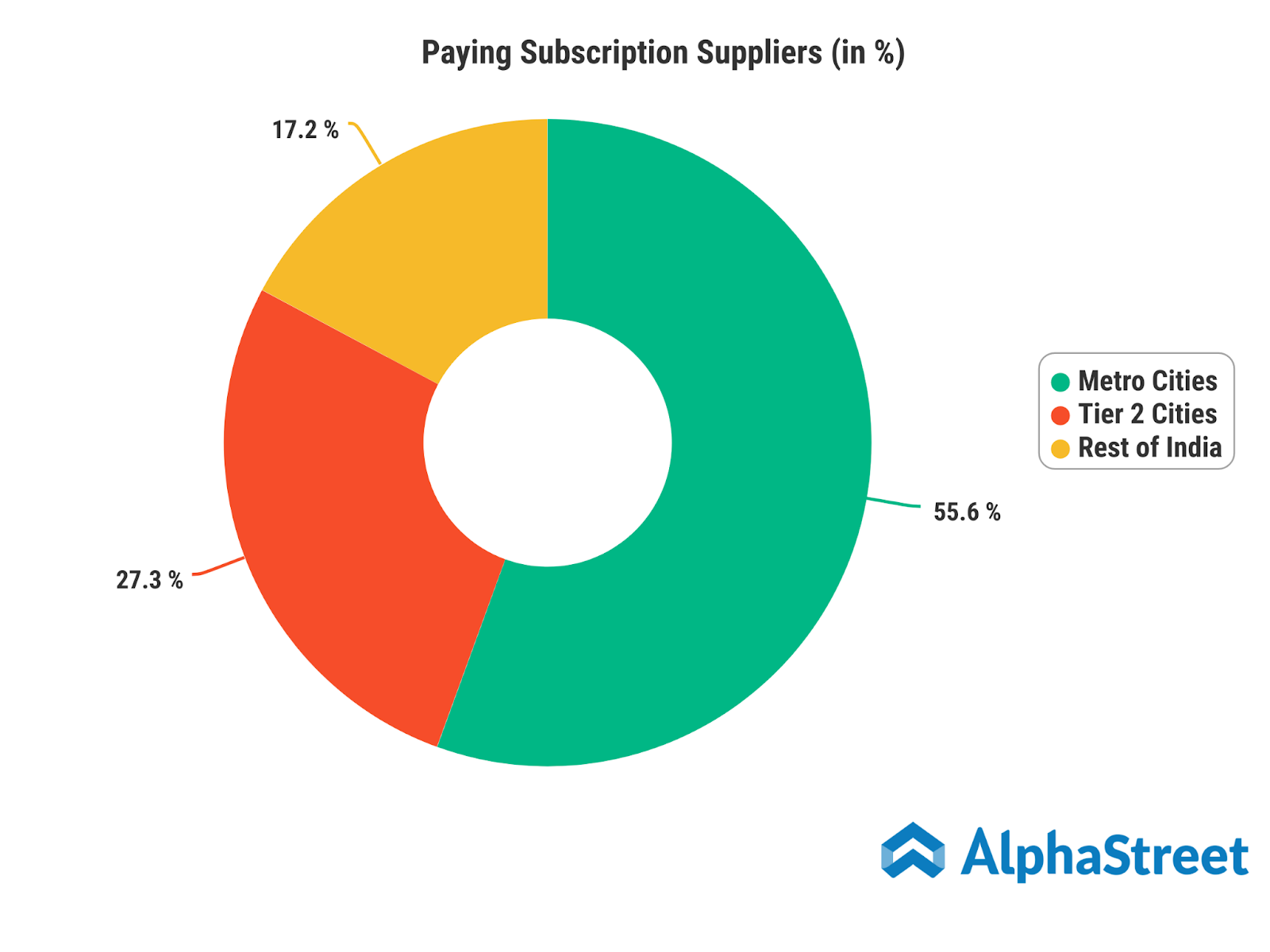

Interestingly, the paying subscription suppliers stand the highest in metro cities and account for 55% of the total paying subscriber base while Tier 2 cities account for 27% and the rest of India accounts for 17% of the total paying subscription suppliers.

Largest in the industry:

The company commands nearly 60% market share of the online B2B classifieds space which makes it the largest player in the industry. It has a portfolio of 7.3 million supplier storefronts, 160 million registered buyers.

Well Diversified Marketplace:

The business has ~87 million products from 56 different industries listed across its website which makes it one of the most diversified marketplace in the country. No single industry accounts for more than 10% of the marketplace. Industrial plants, machinery & equipment is the largest category in the marketplace and covers 8% of it, followed by Construction & raw material (7%), packaging Material, Supplies & Machines (6%), consumer electronics & household appliances (6%) and many more.

Customer Profile:

The business for the company largely comes from small and medium enterprises (SMEs). The platform makes it easier for buyers & suppliers through its offerings which include the marketplace, convenient price discovery, intelligent connect & easy and secure payments.

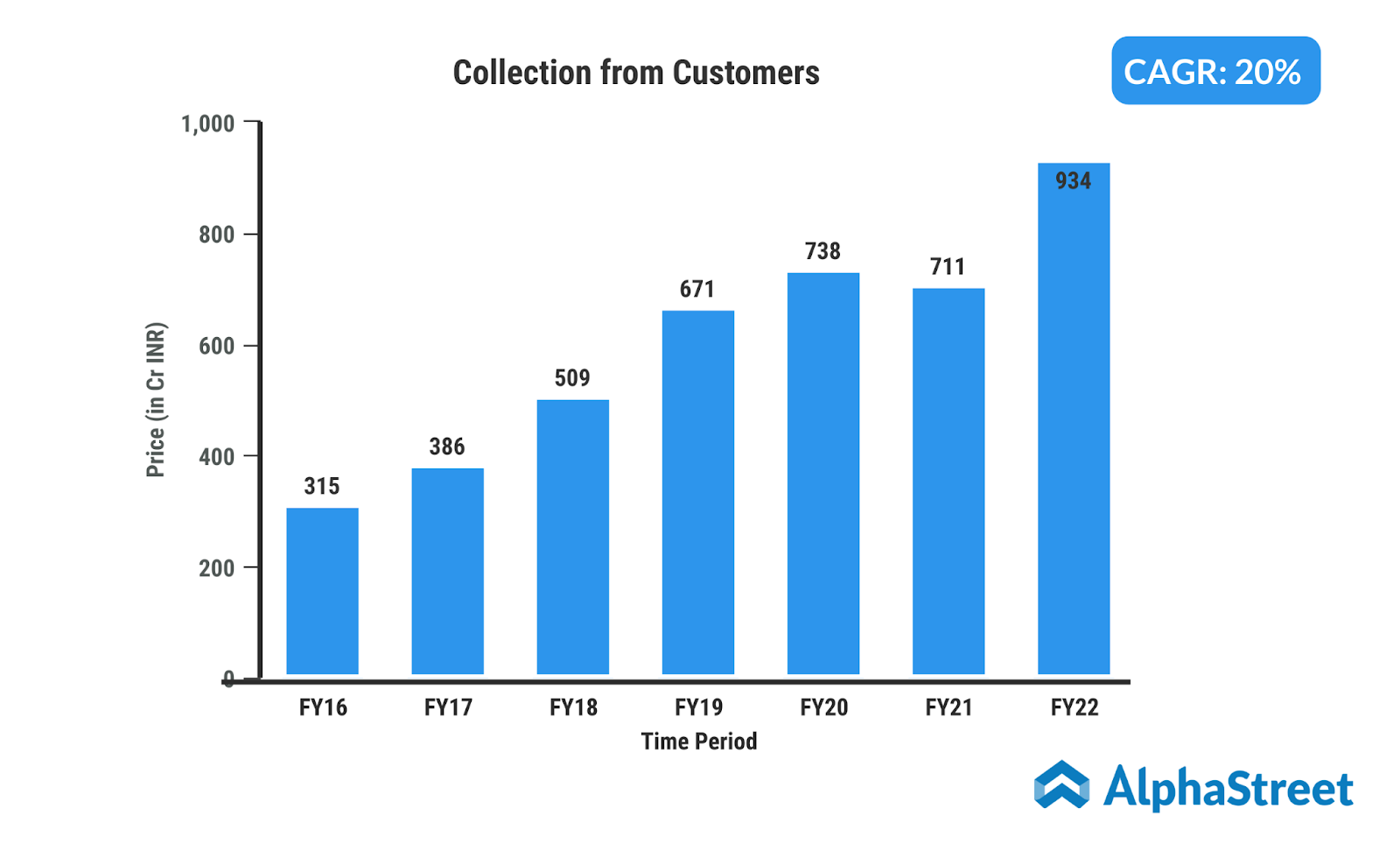

The collection from customers has been growing at a CAGR of 20% over the period of last 7 years and stood at INR 264 crores for the second quarter of FY23.

Strong and growing Employee base:

It has nationwide coverage with more than 85 office branches and a sales & service staff of ~4,088 employees. 21% employees have stayed with the company for more than 5 years depicting the trust they have on the company which in return also increases the efficiency of the company.

Income Source:

The company follows a freemium model and sources 98% of its revenues from the subscription. The top 1% paying customer contributes to 18% of the revenue with an average revenue per user of INR 8.7 Lacs while top 10% contributes 47% of the company’s revenue with an average revenue per user od INR 2.2 Lacs. 58% of revenues comes from sellers in metro cities, followed by tier 2 cities (28 %) & rest of India (15%).

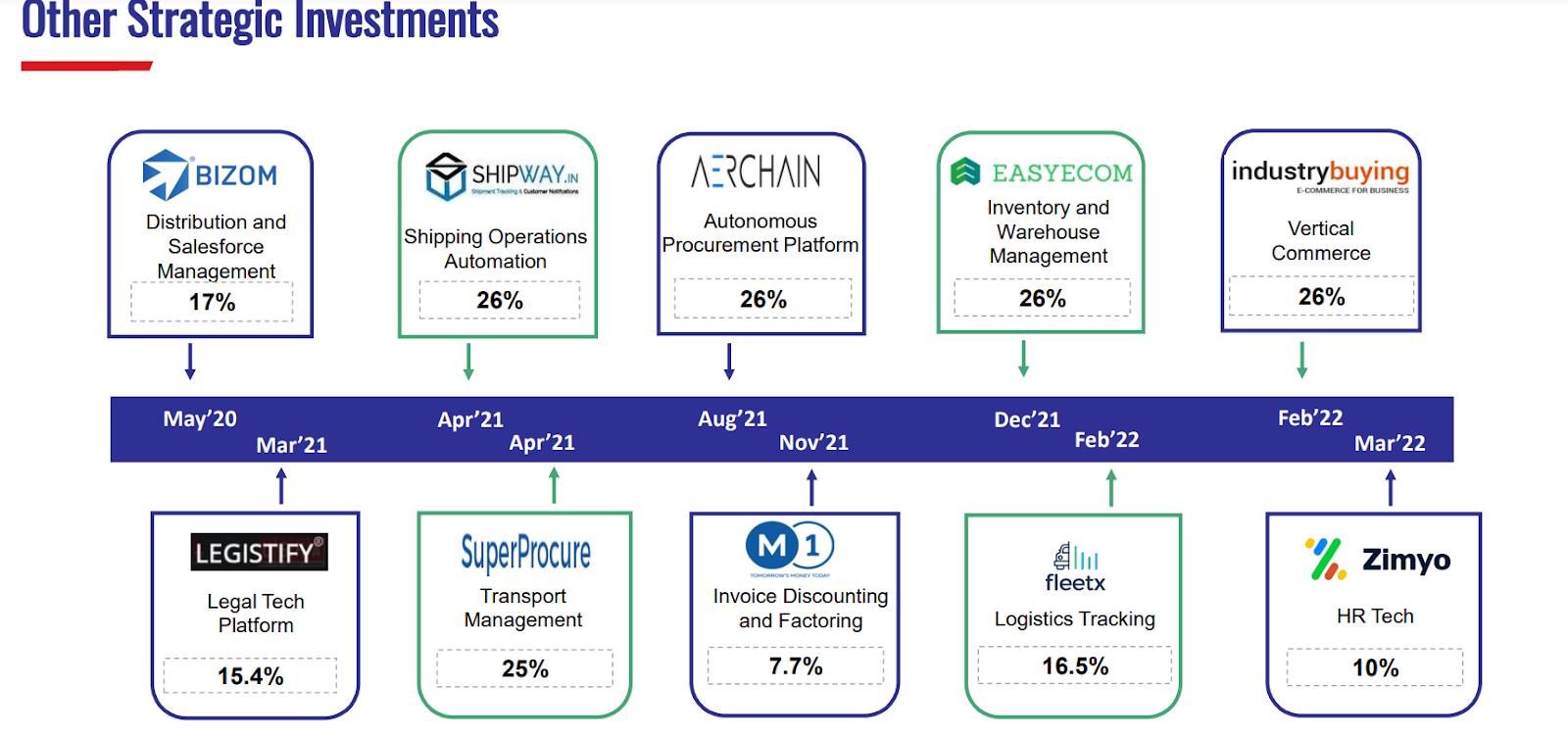

Vyapar and other investments:

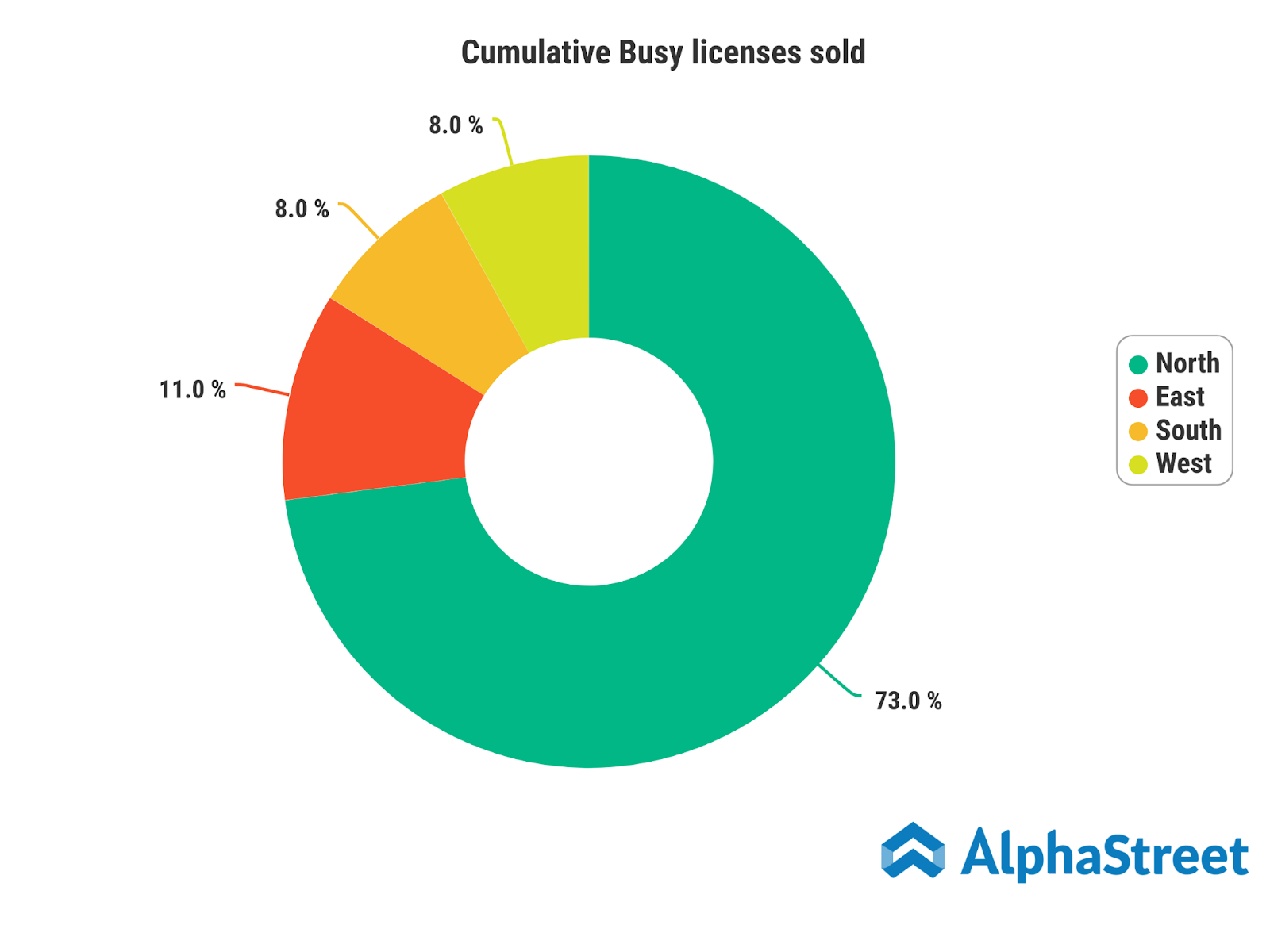

Since listing, IndiaMart has deployed ~INR 9 Bn in over 10-12 investments in software start-ups for minority stakes/big buyouts. Of this, ~INR 6.5 Bn has been deployed in four companies in accounting. It acquired Busy Infotech (on-premise accounting and GST software) for INR 5 Bn in an all-cash deal, hiked its stake in the startup Vyapar (27.5% stale) (offering do-it-yourself, mobile-based accounting and GST software to small businesses), injecting INR 634 Mn, and recently invested in Realbooks (26% stake) and Livekeeping. Now with these four investments in accounting, the company has a portfolio of products that appeals to the entire spectrum of businesses (micro to large). It plans to use cross-selling opportunities to drive growth. Summing it up, we can state that the company pushes a lot of focus on the accounting softwares and wants to tap into the B2B market completely.

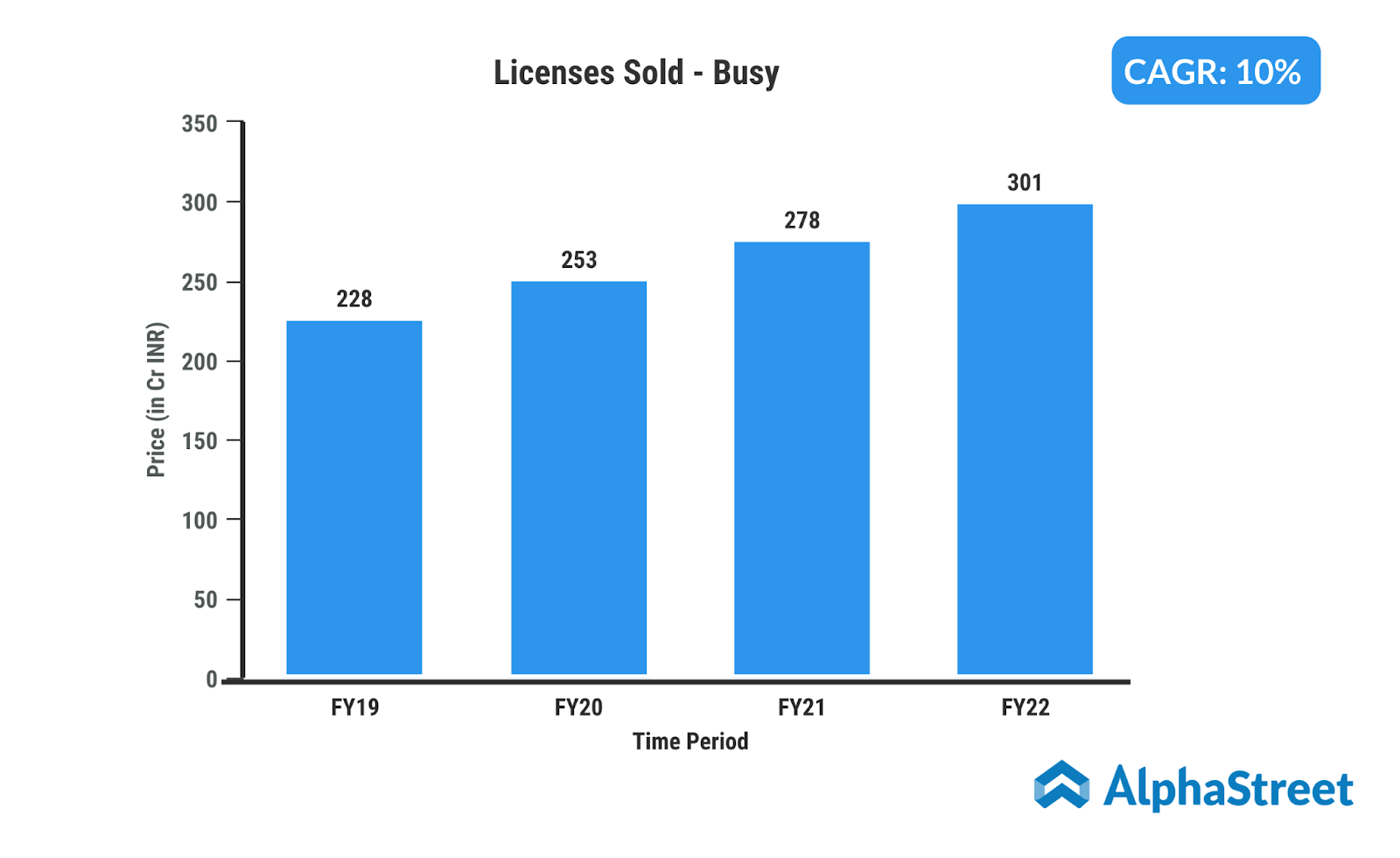

The company also sold accounting software Busy licenses worth INR 301K depicting a CAGR of 10% over the period of last 4 years. The sales for the same have been INR 11.7 crores for the year while the net profit was INR 2.9 crores for the fiscal year 22

The company also has other strategic investments in other businesses as well that includes logistics, people management and operations management.

Let’s take a look at the revenues earned by its investments over the period:

| Particulars (INR Mn) | Revenue FY20 | Revenue FY21 | Revenue FY22 | PAT FY20 | PAT FY21 | PAT FY22 |

| Buzy Infotech | 348 | 424 | 500 | 87 | 110 | 120 |

| Vyapaar | 56 | 117 | NA | NA | NA | NA |

| Realbooks | 21.9 | 26.3 | 33.8 | NA | NA | NA |

| Live keeping | 10 | 20.5 | 33.7 | 0.02 | 2.4 | 5.2 |

We believe that despite the government’s push, MSME owners have been reluctant or slow to digitize systems. While GST, demonetisation and Covid-19 compelled many to switch, the larger proportion still keep accounts offline, which is the way platforms such as Busy and Tally are structured. As more corners of the MSME sector are digitized, a huge market is opening up for software companies. Since IndiaMart is already bringing buyers and sellers online, it makes sense for the marketplace to add digital accounting and billing solutions.

How are they different from its competitors:

A lot of startups have started focusing on SMEs like Power2SME, Moglix, IndustryBuying, Udaan, Bizongo, OfBusines but out of all these, Udaan has drawn heavy focus from the VCs. It commands a huge valuation of almost 5 billion plus (as of 11 Feb 2022). However, the operational business of Udaan is still small compared to IndiaMART.

Udaan operates only in a few verticals like apparel, electronics, pharmacy, staples, fresh food and FMCG products while IndiaMART’s main focus is on long-tail manufacturing products (Also no single category contributes more than 10% of revenues of IndiaMART). Udaan is also into the lending business and yes, it is lending from its own books. So the company needs to turn around its table because once the VC money is all blown up, Udaan will face a severe existential crisis.

Such huge focus / funding by VCs and entry by new startups in this area asserts the longevity of the industry. The company faces a stiff competition from its traditional competitors – Trade India and Exporters India.

| Competitors | Industries Served | Registered suppliers (Mn) | Registered Buyers (Mn) | Number of categories | Market Share |

| IndiaMART | 56 | 7.2 | 149 | 95,000+ | ~60% |

| Trade India | 40+ | 4.2 | 5.8 | 87,886+ | ~14% |

| Exporters India | 40 | 1.2 | 1.6 | 75,000 | NA |

Share price insight:

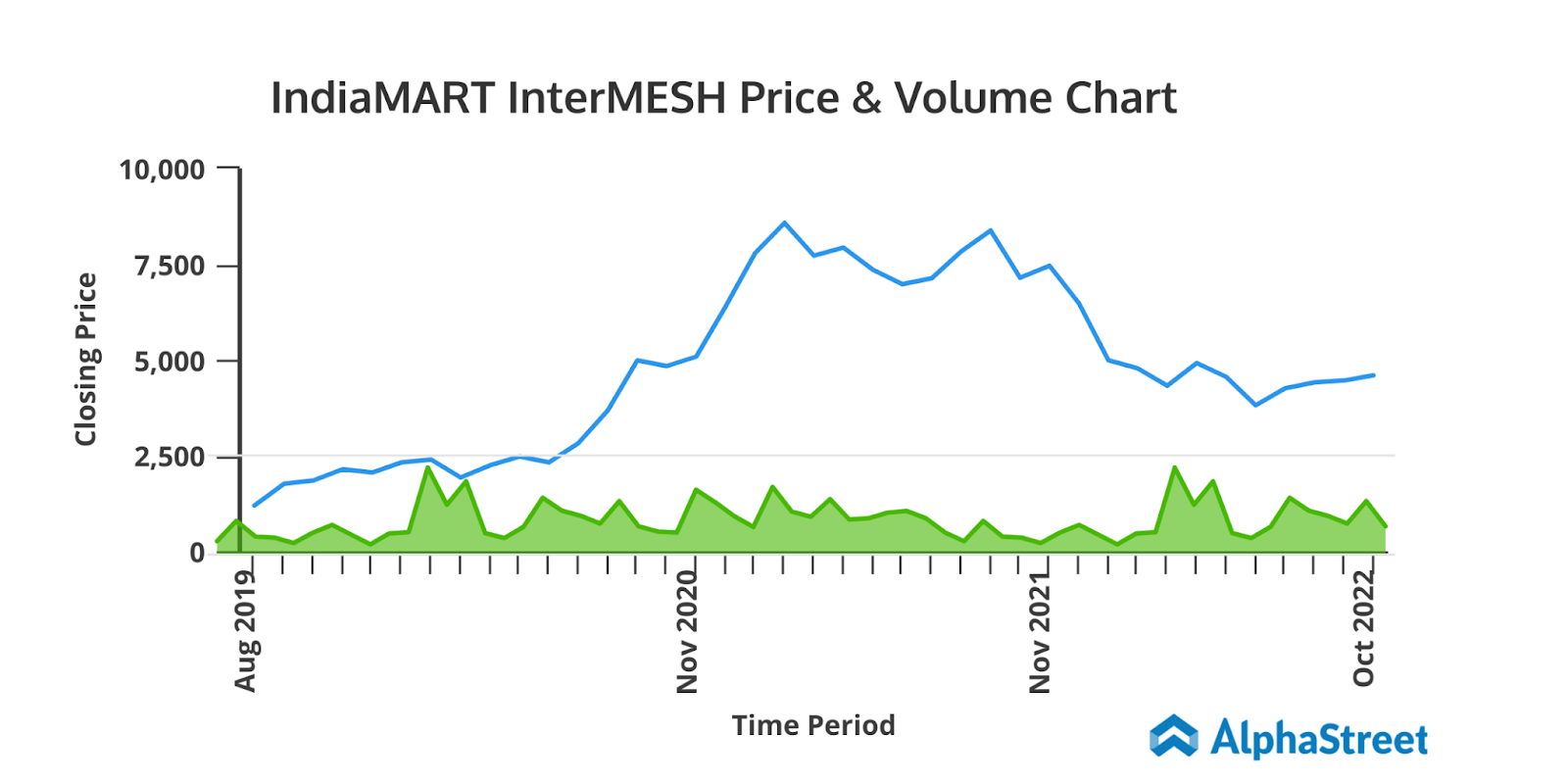

- With the current price of INR 4,608 as of November 1, 2022, IndiaMART is hovering in the mid range of its 52-week range of INR 3676 – INR 7928.

- The stock price has generated a CAGR of 36% over the period of last 3 years.

- The stock delivered a whopping 3-year positive return of 247.3%.

Financial Snapshot:

| FY15 | FY16 | FY17 | FY18 | FY19 | FY20 | FY21 | FY22 | |

| Revenue | 176 | 254 | 318 | 411 | 507 | 639 | 670 | 753 |

| Expenses | 228 | 373 | 391 | 487 | 490 | 472 | 344 | 458 |

| Net profit | -32 | -116 | -64 | -60 | 54 | 211 | 389 | 390 |

| EPS | -34.78 | -126.42 | -70.18 | 54.89 | 7.01 | 50.96 | 92.14 | 97.37 |

IndiaMART has delivered a compounded sales growth of 19% while the compounded profit growth has been a whopping 46% over the period of last 5 years. The company has also given a generous return to its investors as the Return on Equity of the company has been around 25% compounded over the period of last 3 years. Interestingly the company is virtually debt free and hence its bottom-line is not much affected by hefty interest costs. There is also a good revenue visibility for upcoming years due to deferred revenue.

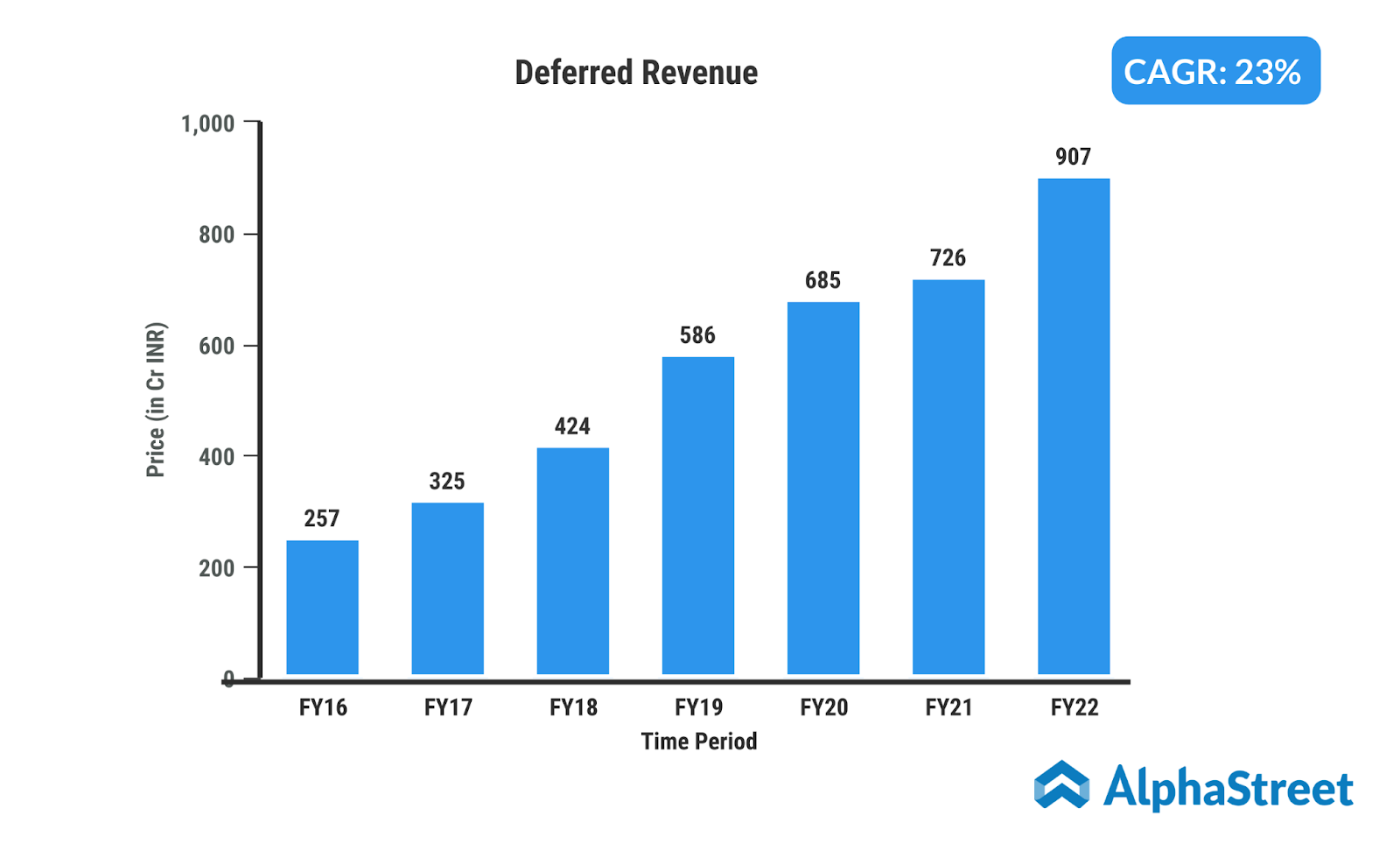

What is the concept of deferred revenue:

IndiaMART has a concept of “Deferred Revenue”. So, when suppliers buy packages for the full year or for a couple of upcoming years, the company already has the cash in their accounts but the revenue is recognized only when that time period passes. All the remaining cash will be accounted as “Deferred Revenue”. Typically, 60% of Deferred Revenue represents contracts for the next 12 months and remaining 40% represents for time period post next 12 months.

The deferred revenues have been growing at a CAGR of 23% over the period of last 7 years and stood at a whopping INR 984 crores for the second quarter of FY23. This states a healthy revenue visibility of the company over the next few years.

Q2FY23 Results:

IndiaMART InterMESH reported a 17 per cent drop in consolidated net profit to INR 68 crore for the quarter ended September. The company had posted a net profit of INR 82 crore in the same period a year ago.

The consolidated revenue from operations, however, increased by 32 per cent to INR 241 crore from INR 182 crore in the September 2021 quarter. The EPS further dropped 17% Y-o-Y to INR 22.34

IndiaMART said it registered traffic of 26.1 crore and total business enquiries of 12.2 crore during the reported quarter. “Paying subscription suppliers grew by 25 per cent YoY (year-on-year) to 1,88,092 with a net addition of 8,832 paying subscription suppliers during the quarter,” the company said.

To visit the alphagraph please click the link here

Factors to consider:

- Disruption:

With VCs shifting focus to B2B now with pretty aggressive moves it might become hard for IndiaMART to face this competition while maintaining profitability.

- Fake suppliers:

Listing of fake products by the suppliers can cause trust issues in the marketplace. The company has turned very stringent while approving suppliers. It is looking for suppliers with 100% verification of mobile numbers and also registering suppliers who have their GST registration completed.

- Hacking / Security issues:

Leaked information of the customers can lead the company into huge troubles which could dampen their profit line.

- Advertising Costs:

IndiaMART had incurred losses few years back when they were bang on in advertising. As of now, they have stopped advertising. P&L statements can take a hit again if they have to go aggressive on advertising again in the future. This might be the case as a lot of new startups are entering the B2B space like Udaan.

- Differential Pricing:

IndiaMART prices SMEs the same across categories, industries, towns and cities. This can cause some suppliers to never afford the packages sold by IndiaMART thus losing out revenues from them. This leaves room for competitors to come up with niche platforms to grab these customers. The company said it will work in this direction after a few years.

Recent Highlights:

- Surge in Product & technology costs is driven by workforce investment. Around 416 employees were hired in H1 FY23. The Company targets returning to 80% gross profit margins in the coming six quarters.

- Most talent acquisition has been made, and only some back-end hiring is left. Manpower hiring will stay up significantly for the next two quarters before stabilizing from FY24. The company plans to add at least 200-500 employees in H2 FY23.

- CAC has gone up due to a substantial increase in demand for talent, which was seen at the end of FY21. Due to this, the industry salaries were revised, resulting in an abrupt rise in CAC.

- Currently, the revenue is split equally between in-house employees and channel partners.

- The guidance of 8,000-9,000 paying customer additions a quarter stays unchanged. For the next four quarters, the Company will maintain a similar customer addition run rate each quarter and will focus on reducing the churn rate, which might elevate on account of aggressive paying supplier addition.

- Currently, 2/3rd of the new customers are added to the silver monthly package, and the rest in silver annually. Historically, Silver Monthly has contributed 15%-20% to the total revenue (Contribution in Q2FY23 stood at 18%).

- Churn rates have almost returned to pre-covid levels. Monthly churn rates of Gold/Platinum are < 1%, silver annual packages are 2%-2.5%, and silver monthly packages are 5-6% a month. The Company starts pitching package upgrades from the 3rd month onwards. Historically, the majority of upgrades have happened post 6-18 months of joining the platform. Silver package (base package) prices are expected to be in the same range and not see hikes soon. On the other hand, the contribution and ARPU of the top 1% and top 10% of customers, which are platinum customers, have increased. The company believes some juice is still left in the city-category combination offerings and will keep experimenting with platinum customers.

- Currently, the Company is finding ways to integrate the acquisitions and investments that can benefit both the Company and invested companies. During the quarter, the Company recorded an FVTPL gain of Rs. 140 Mn. from investments in Legistify and Bizom, which increased other income.

- Majorly, Q4 is the strongest quarter in terms of collection, which also increases the costs related to it. When the deferred revenue recognized in the quarter is lower, margins take a hit. Thus, H2 and Q4 of FY23 are expected to see a negative impact of ~3% compared to H1. Although, the guidance of ~28% operating margins is still intact.

- The company has no plans to sign up for ONDC, as ONDC is still in its trial phase. Once successful in B2C, ONDC will enter the B2B category

Industry Analysis:

In March 2022, GST collections recorded an all-time high of INR 1.42 lakh crores and with this, the average monthly collection in FY 2022 stood at INR 1.24 lakh crores. According to the Ministry of Corporate Affairs, 1.67 lakh new companies were incorporated in FY 2022 which further validates the improving business sentiments in the economy.

The Micro, Small & Medium Enterprise (‘MSME’) segment is a key driver of the Indian economy, contributing 30% to its nominal GDP. Following a significant impact of the pandemic, it is now reviving and witnessing increased digital adoption. A report titled Digital SMBs – Key Pillar of India’s Economy, issued by Zinnov, estimates that India would have 105 million Small & Medium Enterprises (‘SME’) base in 2024, out of which 90% of SMEs to be ‘’digitally influenced’’.

The revival in business, particularly in the MSME segment, is leading to increased digital adoption in the country. India has seen rapid growth in its internet consumption, with the number of users crossing the 830 million mark in 2021 and average internet data usage surging over 11x to 14.1 GB per month from 2018 levels. More and more SMEs are now getting “digitally influenced” and are getting listed on aggregator portals or social platforms etc. The Indian B2B marketplaces have been witnessing strong growth. The sector is facilitating buyers in discovering high quality goods at reasonable prices and it is expected to continue its growth momentum.