Incorporated in 1991, Kolte-Patil Developers Ltd. (“KPDL”| BSE: 532924, NSE: KOLTEPATIL) is India’s leading Real Estate player with a leading position in the Pune residential market. The company also has a growing presence in the Mumbai and Bengaluru residential space thereby attaining a top 3 position among all Real Estate players in the area. Leveraging its more than three decades of experience and a highly professional management, the company has developed and constructed more than 50 projects including residential complexes, integrated townships, commercial complexes and IT Parks, hence covering a saleable area of ~20 million square feet across Pune, Mumbai and Bengaluru. Not only this, but the company’s Long-Term Bank Debt and Non-Convertible Debentures have been awarded a stable/A+ rating by CRISIL, which is one of the highest ratings given by CRISIL to any publicly listed residential Real Estate player in India.

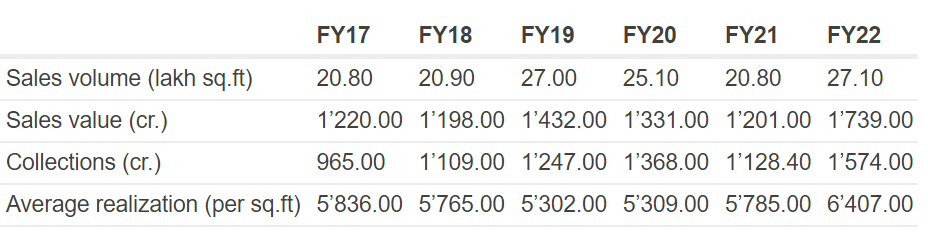

In addition, it has also been given a “Positive” rating by ICRA. An interesting fact about Kolte Patil is that it has smoothly navigated through all varied economic cycles by trebling its revenues then be it 2008 Housing market crisis or the COVID crisis and has therefore maintained the lowest levels of debt in the sector. This can be further proved by the fact that when the world was witnessing lockdown, the Company recorded the highest collection of 1,368 Crore in its three-decades of existence.

Let’s talk about the company’s market areas:

KPDL markets its projects under two brands namely: ’Kolte-Patil’ (addressing the mid-income segment) and ‘24K’ (addressing the premium luxury segment). The Company executed projects in multiple segments – standalone residential buildings and integrated townships.

- Pune

Kolte Patil holds an undisputed market leadership with an extensive presence in the Pune city. Interestingly, the company holds 65-70% of its portfolio in the middle income group segment (50 Lacs to 1 Crore) which is the pulse of the Pune market. And this is how the company is able to maintain steady margins with a large volume in Pune. The homes in this area are bought by the customers based on the track record, brochures and ‘blueprint’ thus making it a credible decision.

- Mumbai

The Company entered the Mumbai Real Estate market in 2013 and signed three society Redevelopment Projects in the first year of its operations. Now, Mumbai being a land-locked and congested city makes Redevelopment as the most preferred mode of development and this segment represents a huge opportunity going forward.

Unlike building a property from scratch, Redevelopment work is a low capital commitment which guarantees the payment of corpus funds with additional returns. KPDL also provides rentals to the tenants with prior approvals. By doing such actions, Kolte Patil has been able to generate a high ROCE from this area. Quite astonishingly, KPDL has established itself as one of the largest listed Real Estate Companies in society Redevelopment space in Mumbai within a very short period.

- Banglore

The residential demand in Bangalore is majorly dominated by an immigrant salaried employee and hence the company targets the middle income segment here. The company builds its projects in attractive locations which helps them convert their prospective clients into buyers.

Given the consistent efforts, the company has been able to generate ~25% of its top line from the Mumbai and Bangalore residential space.

So what’s the Business model:

Being in the Real Estate business is very expensive considering the high land and raw material costs and this is the main reason why you would find a large chunk of debt on the books of major Real Estate players. But Kolte Patil follows an asset light business model. The company partners with Private Equity players like KKR, Portman Holdings, JP Morgan and other notable players like ASK, Motilal Oswal and ICICI ventures. These players have deep financial pockets and a robust knowledge network. For large scale projects, this funding helps with de-risk execution and upfront funding for projects. So, typically if the PE investors agree on a 1 million sq ft construction then KPDL does not invest more than 10-15 crores of their funds initially.

The company also follows a Development Model Approach (DMA) which adds fee income to the revenue stream of the company. Now what’s a DMA you may ask?

So, the land-owner turned developers often find it difficult to sell the property on their own due to the absence of a robust brand value. Now these developers can partner with big brands like Kolte Patil to sell their projects. In return, these large brands can avail between 10 to 30 percent of the total sale proceeds as their share. Hence, such arrangements are a win-win for both the parties.

Further, the company outsources their construction to multiple partners and this depends majorly on the product type. This helps them leverage the material cost. Also, KPDL is an early adopter of new construction technology in Pune wherein they invested Rs. 68 crore in FY12. This resulted in reduced slab cycles and labor requirements from conventional methodology. This further adds to the fact that the company does not shy away from investing in technology and innovating itself unlike other Real Estate companies of India.

Building trust with the customer centric approach:

Delighting customers through the timely delivery and execution are the key to survive in the Real Estate industry and KPDL has become a master of this game through decades of its learnings. The company has an in-house asset management team in place to rent, sell or lease properties thus extending the customer relationship cycle and creating goodwill. This further saves an overhead outsource cost of the company.

Let’s see how the company mitigate risks:

So there are three kinds of risks that a Real Estate development company can face:

- Litigation risk:

The company acquires land clear of any title to ensure the capital is not blocked.

- Regulatory risk:

The company mitigates this risk by paying more to acquire land with key approvals in place with the land owner.

- Macro risk:

The company operates with low debt and focuses more on improvising faster sales and cash flows.

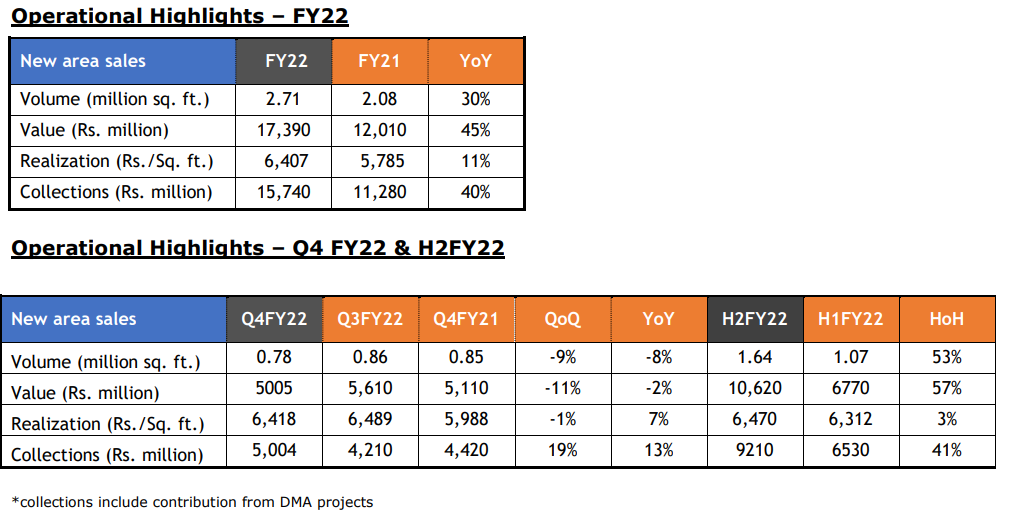

Some Concall Highlights – Q4FY22:

- Some operational highlights:

- The company is confident of delivering 3 mn sq ft during FY23. Leading to Rs.1800+cr of revenue with EBITDA margins of 25%.

- The Mumbai portfolio reported best ever performance and the company further anticipates crossing Rs.650 cr. with IRR target of more than 25% of redevelopment portfolio. Current margin is 22-25%

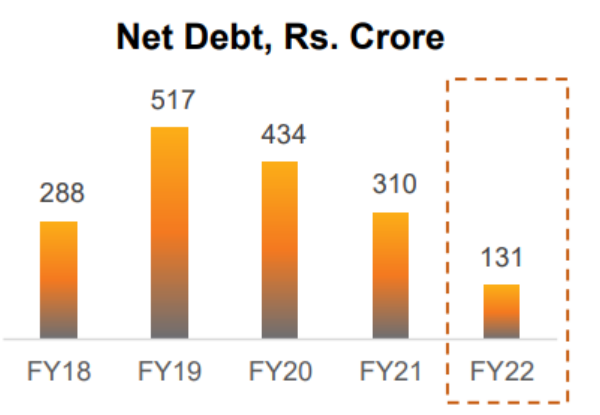

- The company’s debt to equity stood at 0.14 times.

“We reduced Net Debt by Rs. 179 crore during FY22 and by Rs. 41 crore during Q4FY22. This was the third consecutive year of Net Debt reduction, with Rs. 386 crore being reduced in the last three years. As on March 31, 2022 Net Debt/Equity stood at 0.14x.”

Current debt level is at 20 days of collection of business.

- The company is confident of launching projects worth 4,000cr in FY23. This year it was 1,000cr where 70% was from Pune and 30% from Mumbai and Bangalore

- 63% of last year’s inventory has been sold.

- In Mumbai customers are coming to the company even at better terms for the developer showing brand recall.

Management commentaries:

“In addition to the growth in business, we are seeing higher diversification that has resulted in almost 32% of sales by value coming from Mumbai and Bengaluru. Our Mumbai portfolio has reported its best ever performance with a sales value of ~Rs. 450 crore, up 150% YoY. Verve and Vaayu have performed well and witnessed improved realizations. Mumbai portfolio is moving as per plan, and will continue to scale in the coming years with increased launches and business development activity.”

Mr. Rahul Talele, Group CEO

Where is the Quarter?

| Financials | Q4 FY2022 | Q3 FY2022 |

| Total Income | ₹ 380.99 crs | ₹244.70 crs |

| Net Profit | ₹26.82 crs | ₹5.37 crs |

| EPS | ₹ 3.53 | ₹ 0.71 |

The Net Sales improved by 27.02% from Rs 244 crores to Rs 376.07 crore while the total income rose to Rs 380.99 crore in Q4 FY 2022. The Net profit stood at Rs.26.82 crores from Rs 5.37 thereby registering a growth of ~400% from the previous quarter. EBITDA grew 0.38% to 45.39 crore in March 2022 while the EPS has increased to Rs. 3.53 in March 2022.

Future Outlook and Valuations:

Pune, Bangalore and Mumbai are the major IT and financial hub of the country. With the IT boom and Salary hikes, the Real Estate sector will surely revamp itself from its low points. The company is confident of growing its topline by 25-30% in FY23 where the deliverables will be more than 3 million sq ft.

| Reported Sales | Share Price |

| 2008 (peak sales) | ~ 421 cr. |

| 2010 (low sales) | ~ 148 cr. (-65% from peak) |

| 2014 (peak sales) | ~ 764 cr. (416% from low, 81% from peak) |

| 2015 (low sales) | ~ 697 cr. (-9% from peak, 371% from low) |

| 2018 (peak sales) | ~ 1403 cr. (101% from low, 84% from peak) |

| 2021 (low sales) | ~ 692 cr. (-51% from peak, 0% from low) |

| Year | Market Cap/Sales |

| 2015 peak | 2.37 (peak market cap 2015 / peak sales 2014) |

| 2018 peak | 2.19 (peak market cap 2018 / peak sales 2018) |

| 2016 low | 0.85 (low market cap 2016 / low sales 2015) |

| 2020 low | 1.13 (low market cap 2020 / low sales 2021) |

So, In terms of Mcap/sales Kolte got ~2.2x in 2015 and 2018 cycles. Now, if we just look at projected FY23 deliveries, it should be around 1800 cr. (3 mn sq.ft * 6000/sq.ft). With around 25% EBITDA margins, current EV/EBITDA stands at ~ 4.5x. On an EV/pre-sales number, Kolte is currently trading at less than 1x. This is in stark contrast to previous upcycles where it traded at more than 2x of its sales. So, in a quick summary, Real Estate business is in an upcycle and valuations are towards the 2016 and 2020 lows. With the growing economy, the Real Estate sector is expected to boom again in the upcoming financial years. Given the fact of the company’s upcycle, it’s an interesting opportunity to enter the stock at current valuations.