Stock Data

Ticker- DCMSHRIRAM

Exchange- NSE

Price Performance

Last 5 days: (+4.54%)

YTD: (+3.8%)

Last 12 Months: (+10.43%)

Story Behind the Growth:

- Despite the rise in input costs, the Chemical segment grew substantially. The sheer increase in volumes and product pricing became the major driver of profitability.

- The government’s objective regarding ethanol blending has provided a huge opportunity for sugar manufacturers. The 20% ethanol blending by 2025 aim for India bodes well for the firm.

- The Fenesta business grew dramatically. With the introduction of new products coupled with an expansion strategy, Fenesta has provided higher profitability on the backs of higher volumes and better margins.

Critical news to watch out for:

- Updates on Uttar Pradesh’s Government Policy regarding the Sugar Industry for the next Sugar Season.

Company Description:

DCM Shriram Ltd. is a diversified business entity, with a considerable presence across the Agri-Rural value chain with a stake in the Sugar and Urea Industry. It also possesses a sizeable stake in the Chloro-Vinyl industry. The firm has introduced value-added segments in these domains primarily Fenesta which focuses on UPVC windows and doors.

Research Summary

“Margins in the Chemical business are expected to normalize over the next few quarters after significantly high levels over the last three quarters.”

Mr. Ajay Shriram, Chairman and Senior Managing Director in the Q1FY23 Earnings Call

Thus, insinuating that the biggest driver of profitability will observe lower margins, which would affect profitability. However, with the huge CapEx pipeline of the firm focused mainly on the Chemical and the Sugar business, the profits might not see a drop in absolute values over the long term.

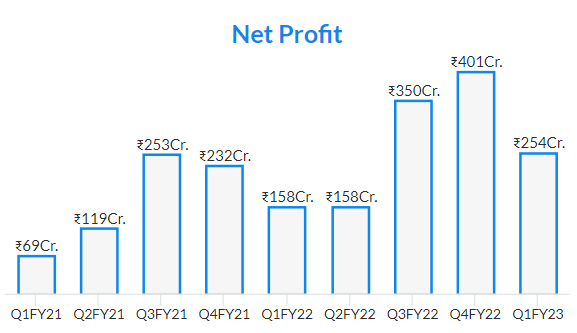

| (₹ Cr.) | Q1FY23 | Q1FY22 | YoY (%) |

|---|---|---|---|

| Total Revenue | 2,999.90 | 2,025.11 | 48% |

| Total Expenditure | 2,613.25 | 1,809.41 | 44.5% |

| Profit After Tax | 253.96 | 157.50 | 61% |

Sugar business when analysed from a global standpoint seems bright. With international prices showing signs of strength mainly due to the global diversion towards ethanol caused by the rise in fuel prices. Domestically, the Indian government’s objectives towards Ethanol blending poses itself as an opportunity for the firm. However, the Uttar Pradesh Sugar Export Policy and views on cane-juiced ethanol stands as an obstacle. This affects the firm’s sugar business as all the firm’s sugar production units and distillery units are based in Central UP. The firm expects the State Government to come up with a lucrative sugar export policy. DCM Shriram Ltd. will benefit greatly from this, given that the firm has invested ₹ 550 Cr. in the form of CapEx in the sugar business. These undertakings will be commissioned by Q3FY23 as per the management.

Fenesta Building Systems has shown great promise. This diversification strategy has been an intelligent move by the firm. The firm has taken initiatives to expand the regional presence as well as the product offerings.

| Fenesta Segment (₹ Cr.) | Q1FY23 | Q1FY22 | YoY% |

| Revenue | 167 | 108 | 54 |

| PBIT | 28 | 9 | 218 |

| PBIT Margin | 17 | 8 | 107 |

| Order Book | 185 | 87 | 113 |

Our View:

The company is trading at a discount considering the long term growth prospects of the firm. The company has heavily invested in its future. Along with that, the diversified nature of the firm provides a safer alternative to traditional companies. The company has prudently diverted its CapEx to well performing segments of its holdings while also investing in segments that have brighter futures ahead of them due to the macro environment surrounding them. The debt level of the firm is under control while the firm is generating healthy levels of cash flows. The current investments are majorly financed with internal accruals and debt.