“The company is looking for close to Rs. 500 Cr to Rs. 550 Cr of capex by March 2025 mainly related to value-add CAPEX on the BOPET line, CPP line, BOPP line, specialty chemicals and some in Zigly. The net debt stands at Rs. 355 Cr. We are expecting without even considering any bottom-line addition from the new CAPEX, the net-debt to EBITDA should remain between 1-2x even at the peak level of debt because of these expansion.”

-Neeraj Jain, Group Chief Financial Officer

Stock Data

| Ticker | COSMOFIRST |

| Exchange | NSE & BSE |

| Industry | Packaging |

Share Price

| Last 1 Month | -4.2% |

| Last 6 Months | -28.3% |

| Last 12 Months | -52.7% |

Business Basics

Cosmo First Limited (NSE: COSMOFIRST) is a leading global manufacturer of specialty films for packaging, lamination, and labelling applications. The company offers a wide range of specialty films, including BOPP (biaxially oriented polypropylene) films, thermal lamination films, and CPP (cast polypropylene) films. Cosmo Films has a strong customer base across the globe and serves several industries, including packaging, labelling, and industrial applications. The company has built a reputation for providing high-quality products that meet the evolving needs of its customers. Cosmo Films invests heavily in research and development to develop innovative products and technologies that enable it to stay ahead of the competition. The company’s robust business model, diversified product portfolio, and strong customer relationships are some of its key strengths, enabling it to navigate the challenges posed by the competitive market environment.

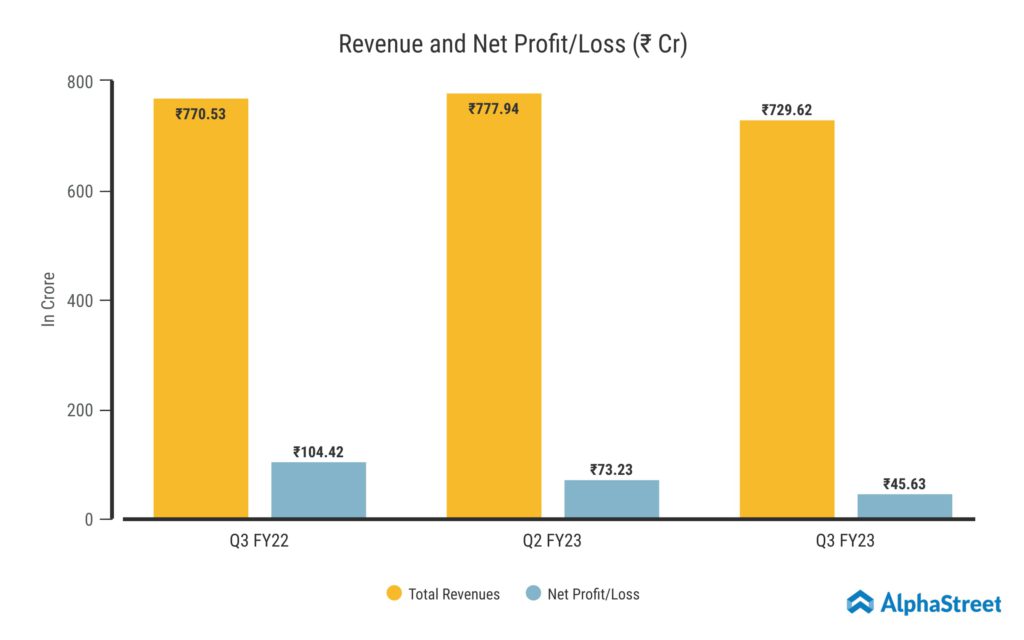

Q3 FY23 Financial Performance

Cosmo First Limited reported Revenue from Operations for Q3 FY23 of ₹729.62 Crore down from ₹770.53 Crore year on year, a decline of 5.3%. Consolidated Net Profit of ₹45.63 Crore, down 56.3% from ₹104.42 Crore in the same quarter of the previous year. The Earnings per Share is ₹16.65 for this quarter.

Sales Lowered Due To Maintenance

The consolidated sales for the quarter are down 5% from the December 2021 quarter. This decrease was primarily due to lower sales volume as a result of a planned maintenance shutdown, with some additional impact from a change in sales mix. The EBITDA for the quarter fell by 47% year over year to ₹86 Crore. This resulted from the loss of ₹32 crore worth of non-repetitive goods. Included in this are a one-time inventory loss on raw materials and finished goods of about ₹14 Crore, as well as planned maintenance on some of the production lines that resulted in a 10% decrease in BOPP volume.

As per the management, “Generally, we prefer doing such maintenance activity during the low margin period and the lower specialty film sale, majorly due to inventory correction in Europe and US. We feel this is fairly temporary and can already see that normalization has started to happen from quarter 4 onwards.”

Expansion of BOPP & CPP Production Capacity

The company’s growth projects in flexible packaging, as well as work on the BOPP and CPP lines, are proceeding as planned. Both lines will have the highest production capacity in the world and nearly double the company’s current production capacity. Because the CPP and BOPP line will have a single layer of material, it will encourage sustainability. The company will be able to further expand its speciality film portfolio due to the capacity additions represented by the specialised BOPET line, which we completed in September 2022, as well as the proposed BOPP line and CPP line.

Updates In Business Divisions

Sales for the Specialty films division of Cosmo First temporarily declined in the third quarter. The volume has decreased to 57% as of the December 2022 quarter from 64% the previous quarter, primarily as a result of inventory correction in the US and Europe. In FY23, the management anticipates specialty growth to be largely flat, and in FY24, they anticipate double-digit specialty growth. The company plans to launch a few specialty products on the BOPET line in Q1 of FY 2024, including PET-G films, window films, security films, and many others.

The Company’s Specialty chemicals subsidiary reported ₹34 Crore in sales during the December 2022 quarter, which is nearly 31% higher than the December 2021 quarter.

As per the company’s management, “We expect FY23 to close between Rs. 160 to 170 Cr of sales with positive EBITDA. Even after inventory loss in Q3, the Speciality chemical subsidiary should post full year’s profit for the FY23. Company has reached close to 75% capacity utilization on masterbatch line and the complementary adhesive business for the packaging segment is planned to be launched in Q4FY23. This is going to add to top line and bottom line from next year.”

Zigly, the company’s direct-to-consumer pet care vertical, which debuted in September 2021, opened 11 experience centers at the end of the third quarter. Furthermore, the business intends to add another 15 experience centers by the end of March 2023. The target growth rate for the next two to five years is a 10 times increase from the current monthly Gross Merchandise Value of ₹1.3 Crore. Over 10,000 customers have been served by Zigly to date, with almost a third being repeat customers. Zigly is a valuation-driven company that should benefit shareholders in the years to come. However, the pet care division currently experiences a quarterly EBITDA loss of about ₹4 Crore due to its growth and expansion.