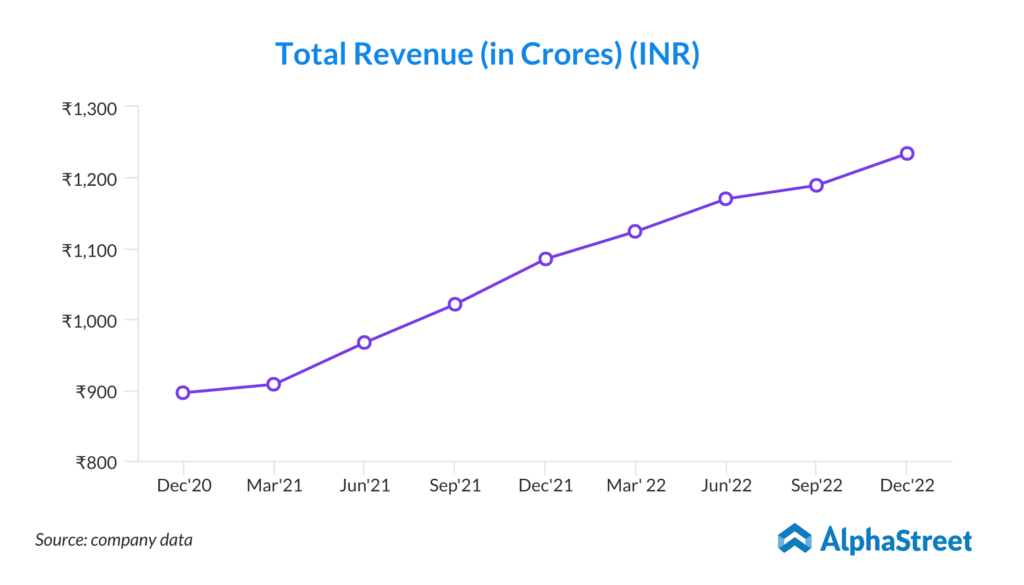

“Our revenues for the quarter have grown 14% YoY and 2.5% QoQ to Rs 12,219 million. Deal wins have also been strong at US$ 231 million TCV for the quarter. We continue to strengthen our position as a domain and enterprise digital capability-led player. The business is fundamentally robust and we are making the investments necessary for future growth, which makes me confident about our outlook going forward.” – Mr. Angan Guha, Chief Executive Officer and Managing Director, Birlasoft

| Stock Data | |

| Ticker | NSE: BSOFT & BSE: 532400 |

| Exchange | NSE & BSE |

| Industry | IT Services |

| Price Performance | |

| Last 5 Days | -7.85% |

| YTD | -15.29% |

| Last 12 Months | -44.76% |

Company Description:

Birlasoft, the global technology services division of the CK Birla Group, has successfully integrated with KPIT Technologies. CK Birla Group is one of India’s leading commercial and industrial houses, with strategic equity participation by GE Capital. Birlasoft offers IT services worldwide from its development centers in India and Australia. After the merger with KPIT Technologies in January 2019, the new combined entity had revenues of USD 475mn in FY19 and a headcount of around 10,000. Despite the merger, there is limited overlap in clients and service offerings between Birlasoft and KPIT Technologies. The sales of the combined entity have been aligned to verticals to streamline sales efforts, with sales teams focusing on specific industries such as healthcare, finance, and retail. Birlasoft’s successful integration with KPIT Technologies, which has allowed the company to overcome integration challenges, restructure its sales and delivery functions, and optimize its cost structure. This has enabled Birlasoft to offer a broader range of services to clients while increasing its competitiveness in the global IT services market.

Critical Success Factors:

- The company is experiencing a healthy deal pipeline that will drive double-digit revenues. The company is witnessing healthy traction in cloud migration, app modernization, and workplace modernization. Additionally, Birlasoft has partnered with Microsoft to drive cloud migration of on-premise SAP and JD Edwards. Birlasoft’s steady deal wins, indicating a strong pipeline. For the quarter ending Dec’22 , Birlasoft reported a total contract value (TCV) of US$231 mn, up 39.2% quarter-over-quarter (QoQ) and including new deal wins of US$102 mn, down 26.1% QoQ. The company won three large deals for the quarter, and it aims to have more sticky revenue from clients, especially from its top 20 accounts. Birlasoft also mentioned that its legacy business is likely to report flattish revenue growth in FY23, while growth from new-age and digital business is likely to be industry-leading. This suggests that Birlasoft is successfully adapting to the changing market demands, and its focus on digital business will help it to maintain industry-leading growth. The steady deal wins and strong pipeline suggest that Birlasoft is well-positioned for future growth, while the focus on digital business suggests that it is adapting to changing market demands

- The company reported healthy margins in the quarter, led by higher utilization and offshoring. It is expected that margins will improve mainly due to pyramid rationalization, rationalization of support staff and subcontracting costs, and an increase in annuity revenues and fixed-price projects, partially offset by investment in reskilling of employees and geographic expansion. Birlasoft’s revenue from its top 5/10/20 clients grew by 1.7%/1.2% and 0.4% quarter-over-quarter (QoQ), respectively. Additionally, the company’s last twelve months (LTM) attrition declined 190 basis points (bps) QoQ to 25.5%. The company expects attrition to moderate further and provide a tailwind lever for margin improvement. The company’s utilization during the quarter improved by 160 bps QoQ to 84%. Furthermore, Birlasoft’s growth momentum in the banking, financial services, and insurance (BFSI) sector continues to be good, as it has been in a leadership position in a couple of processes in this space and is looking to capitalize on the same for further growth acceleration. The company has a good set of clients in the BFSI space, and growth in some top accounts is helping them. Birlasoft’s sustained improvement in margins is expected, primarily due to rationalization and cost optimization measures, an increase in annuity revenues, and a decline in attrition. Additionally, the company’s leadership position in BFSI processes and good set of clients in the BFSI space provide a positive outlook for further growth acceleration.

- Birlasoft has made some recent leadership appointments in the hi-tech, manufacturing, life sciences, and energy verticals. The company is optimistic about the growth prospects of these verticals in the medium-term. In manufacturing, the company has observed growth in both discretionary and non-discretionary spending, although growth may slow down for a few quarters before rebounding. Birlasoft is currently focused on growing its organic capabilities and business, but it may consider opportunities for inorganic growth in the future. However, the management clarified that it is not actively looking for any inorganic opportunity at the moment.

Key Challenges:

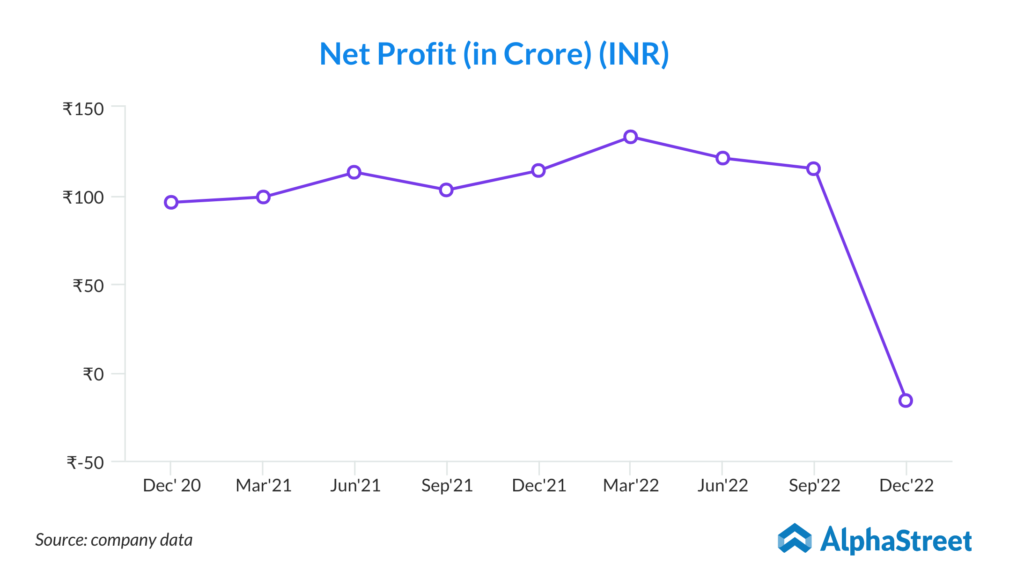

- Birlasoft’s major client, Invacare Corporation, has filed for bankruptcy protection and restructuring, which has impacted the company’s revenue. Invacare is a leading manufacturer and distributor of medical equipment used in non-acute care settings. The contribution of Invacare to Birlasoft’s topline was around 3%. In response to the situation, Birlasoft has created a provision of Rs. 151.04 crore against the outstanding receivables and contract assets. The management stated that they are not expecting any revenues from Invacare in Q4FY23. The provision has been made to account for the revenue impact, but the management needs more clarity on the costs side, and they are taking a legal opinion on the same.

- The company derives a significant portion of its revenue in foreign currencies, particularly the US dollar. Any appreciation in the Indian rupee or adverse cross-currency movements can have a negative impact on the company’s earnings. Birlasoft’s business is closely linked to the global economy and any macroeconomic headwinds, such as a possible recession in the US, could moderate the pace of technology spends and impact the company’s revenue growth.

- Birlasoft operates mainly in the US market and depends on the availability of skilled local talent. A constraint in local talent supply in the US could affect the company’s ability to deliver services and impact its earnings and the IT services industry is highly competitive, and Birlasoft faces competition from global and domestic players. Any inability to compete effectively could impact the company’s market share and revenue growth. The company’s revenue is concentrated among a few key clients, and any adverse development with these clients could impact its revenue and profitability.

- Birlasoft reported weak quarterly results with a decline in Enterprise Solutions revenue by 7.1% QoQ, while Business & Technology Transformation revenue grew by 5.5% QoQ. The company’s dollar revenue stood at $148.4 million, a YoY increase of 3.5% but a QoQ decline of 0.3%. However, in rupee terms, the revenue grew by 14.0% YoY and 2.5% QoQ to Rs. 1221.9 crore. The company’s EBITDA was impacted due to the one-time provision taken on account of the filing of bankruptcy by one of their major clients, Invacare. Consequently, the company reported a net loss of Rs. 16.4 crore for Q3FY23. However, excluding the one-time provision, the EBITDA was Rs. 158.4 crore, and the EBITDA margin was 13.4%.