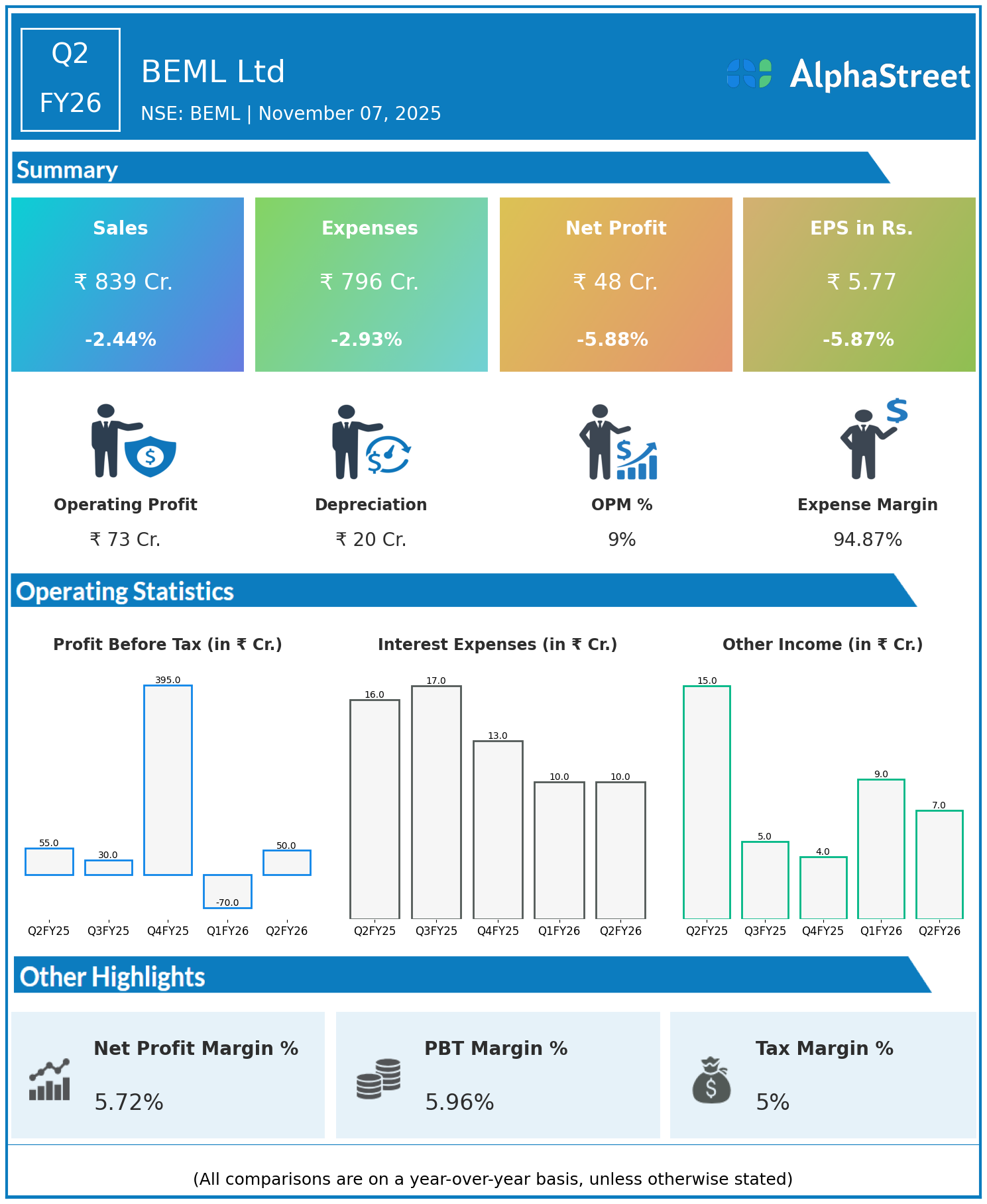

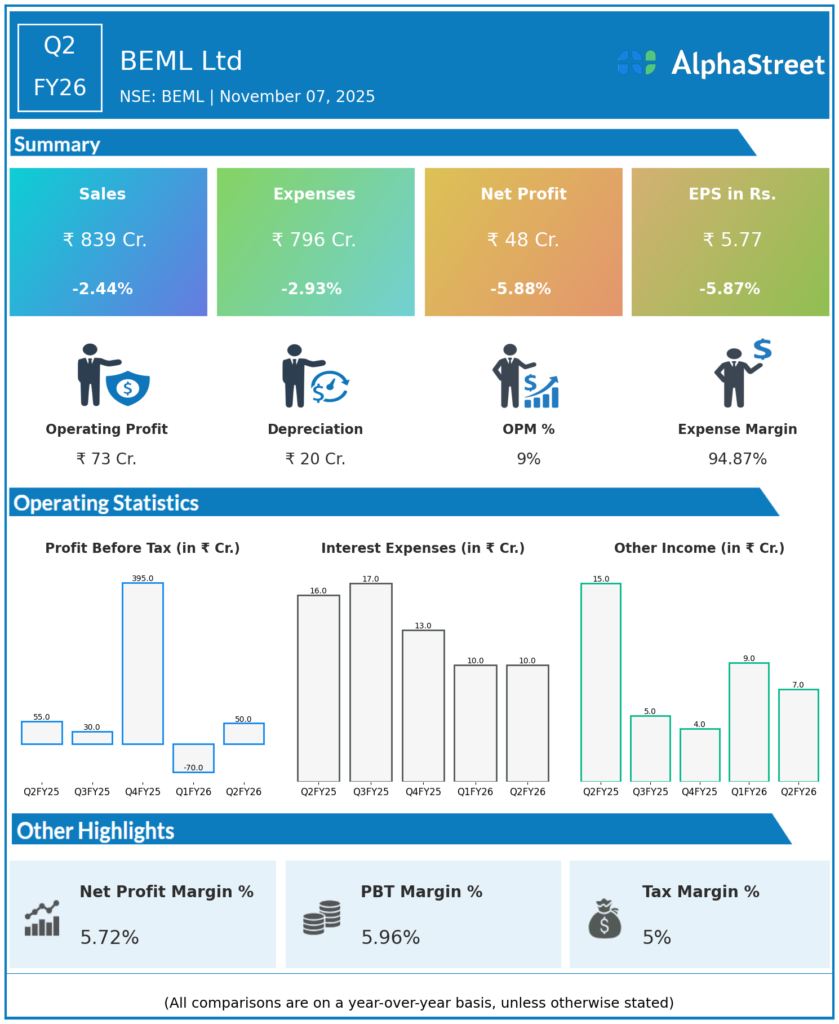

BEML Ltd, a key manufacturer of heavy earthmoving equipment serving mining, construction, defense, and railways sectors, reported a slight decline in Q2FY26 financials amid softer demand conditions.

Financial Highlights:

- Revenues declined 2.44% year-on-year to ₹839 crore from ₹860 crore.

- Total expenses fell 2.93% to ₹796 crore compared to ₹820 crore last year.

- Consolidated net profit decreased 5.88% to ₹48 crore from ₹51 crore.

- Earnings per share declined 5.87% to ₹5.77 from ₹6.13.

The company demonstrated stable operating margins with effective cost control measures offsetting some revenue softness. Order execution remained robust with a sizable order book supporting near-term prospects.

Outlook:

BEML is focused on delivering value through operational efficiency, timely execution of defense, rail, and infrastructure projects, and leveraging emerging market opportunities. The company aims to return to growth as market conditions normalise.

This quarter’s results reflect resilience amid headwinds, positioning BEML for a steady recovery in the evolving industrial landscape.

Explore the company’s past earnings and latest concall transcripts, click here to visit the AlphaStreet India News Channel.