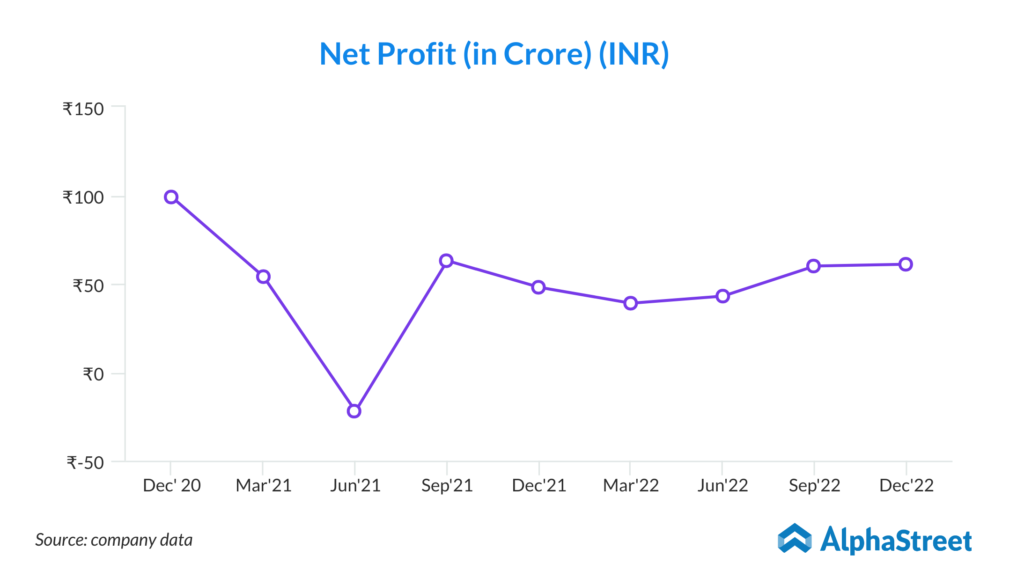

“Consumer Products revenues have crossed Rs 1,000 crore for the quarter, which has helped achieve a PBT growth of 25.2%, in a tough market. EPC has delivered positive EBIT for the current quarter coupled with a strong focus on a collection of receivables.” – Mr. Shekhar Bajaj, Chairman of Bajaj Electricals Limited

| Stock Data | |

| Ticker | NSE: BAJAJELEC & BSE: 500031 |

| Exchange | NSE & BSE |

| Industry | CONSUMER DURABLES |

| Price Performance | |

| Last 5 Days | +1.49% |

| YTD | +3.38% |

| Last 12 Months | -7.26% |

Company Description:

Bajaj Electricals Ltd is an Indian consumer electrical equipment manufacturing company that produces a wide range of products including fans, lighting, household appliances, and power distribution equipment. The company was founded in 1938 and is headquartered in Mumbai, India. Bajaj Electricals has a strong presence in India and operates through a network of dealers and distributors across the country. The company has also expanded its operations globally and has a presence in several countries including the UAE, Oman, Yemen, Kenya, Nigeria, and Ghana. The company has a diverse product portfolio and caters to various customer segments. In recent years, Bajaj Electricals has focused on expanding its product offerings and has also invested in research and development to introduce innovative products to the market. The company has also embraced technology and has launched several smart and connected products.

Critical Success Factors:

- Bajaj Electricals’ CP segment revenue has increased by around 10% year on year to approximately 1040 crore, driven by strong growth in fan revenue. The fan revenue has increased by approximately 64% year on year in Q3FY23, due to the company’s focus on de-stocking of non BEE rated fans to comply with changes in BEE norms. The demand outlook for Bajaj Electricals is positive. The demand for consumer appliances is expected to pick up from Q1FY24, driven by fresh inventory build-up of new star-rated fans at the dealer level, and a pick-up in rural demand supported by the easing of inflationary pressure.

- The company is also focusing on new product launches, including into premium segments, and market share gains in the lighting segment. The restructuring of consumer lighting distribution is likely to be completed by H1FY24, and the company is strengthening its management team and adding new dealers to drive revenue growth. Additionally, Bajaj Electricals has a healthy order book of approximately 1200 crore in the EPC (engineering, procurement, and construction) segment, and it expects steady growth in this segment going forward.

- Bajaj Electricals’ CP and lighting segment revenues exceeded expectations, driven by the company’s focus on de-stocking non-star rated fans in Q3FY23. However, it is believed that the preseason inventory build-up at the dealer level is largely complete, and the volume offtake of new star rated fans is expected to slow down in Q4FY24. Management commentary indicates that primary sales of fans are likely to pick up from H1FY24, supported by channel filling and a pick-up in rural demand due to the easing of inflationary pressure. On the lighting front, strong demand for professional lighting, completion of the dealer realignment program, and new product launches are expected to drive lighting revenue growth in the future.

Key Challenges:

- Bajaj Electricals’ lighting revenues declined by around 2% year on year to approximately 270 crore, mainly due to lower revenues from the consumer lighting segment, which was impacted by the realignment of distribution networks. However, the professional lighting segment grew strongly, supported by market share gains. The company expects the EBIT margin under the lighting segment to move upwards from the current level, supported by new product launches and higher operating leverage. However, revenues for appliances and Morphy Richards were down by approximately 4% and 15% year on year respectively, primarily due to lower demand in rural regions and slower sales of water/room heaters due to a delay in the onset of winter.

- One major risk is the potential impact of supply chain disruptions due to the ongoing COVID-19 pandemic. This could affect the company’s ability to source raw materials and manufacture products, which in turn could impact its revenues and profitability. Another concern is the competitive landscape in the consumer appliances and lighting segments, with the company facing intense competition from both domestic and international players. This could impact the company’s market share and profitability, especially if it is unable to keep up with changing consumer preferences and market trends. Additionally, there is a risk that the company’s EPC segment could face challenges in securing new orders or executing existing ones, which could impact its revenue growth and profitability. Finally, the company’s dependence on the domestic market could be a risk if there are any changes in government policies or economic conditions that impact consumer demand for its products.

Q3FY23 Result:

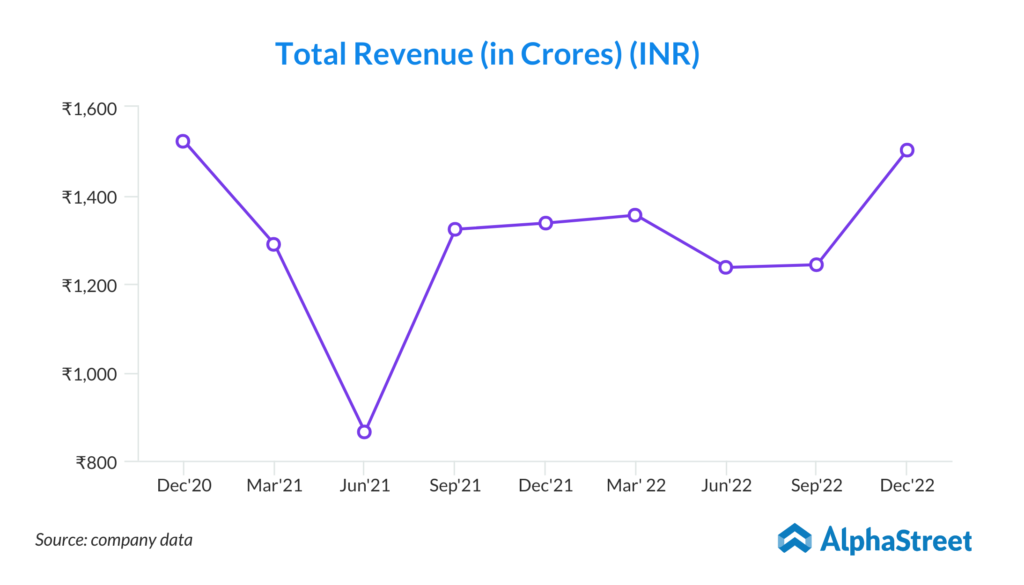

Bajaj Electricals Ltd announced its Q3FY23 results, reporting a 12% YoY growth in revenue from operations to Rs 1,484 crore. The Consumer Products (CP) segment’s revenue increased by 9% YoY to Rs 1,039 crore, driven by strong growth in fan revenue, which increased by 64% YoY. The Lighting Solutions (LS) segment’s revenue declined by 2% YoY to Rs 270 crore due to lower revenues from consumer lighting, but the professional lighting segment grew strongly supported by market share gains. The EPC segment achieved a total revenue of Rs 175 crore, registering a growth of 87% YoY. The company also generated positive cash flow from operations of Rs 375 crore in 9MFY23, and its cash equivalents and surplus investments were at Rs 380 crore. The management expects the demand for consumer appliances to pick up from Q1FY24 onwards, driven by fresh inventory build-up of new star rated fans at the dealer level and pick up in rural demand. The company is also increasing its focus on new product launches and market share gains in the lighting segment, and it expects the EBIT margin of the lighting segment to move upwards from the current level supported by new product launches and higher operating leverage.