I believe India is well placed in the post pandemic world. Our favorable demographics, stable democratic set up, and increasing impact of technological innovations like India Stack coupled with structural reforms are helping India emerge as a knowledge and technology leader in the world. Overall, our Bank is well positioned to capitalize on the emerging opportunities, and the recent acknowledgment as ‘Best Small Finance Bank’ by BT-KPMG will inspire us further”. Mr. Sanjay Agarwal, MD & CEO, AU Small Finance Bank

| Stock Data | |

| Ticker | NSE: AUBANK & BSE: 540611 |

| Exchange | NSE & BSE |

| Industry | BANKING & FINANCE |

| Price Performance | |

| Last 5 Days | +4.33% |

| YTD | -12.02% |

| Last 12 Months | -10.22% |

Company Description:

AU Small Finance Bank is a scheduled commercial bank in India that provides banking and financial services to individuals, micro, small and medium-sized enterprises (MSMEs), and retail customers. It was originally incorporated as Au Financiers (India) Limited in 1996 and was granted a license to operate as a Small Finance Bank by the Reserve Bank of India in 2017. The bank offers a range of products and services including savings accounts, current accounts, fixed deposits, loans, insurance, and investment products. It operates through a network of branches and digital channels across India. AU Small Finance Bank has a strong focus on financial inclusion and serves customers in rural and semi-urban areas, providing them with access to banking services and credit facilities. The bank has received several awards for its innovative products, customer service, and technology-enabled solutions. It is also known for its strong corporate governance practices and has been recognized as one of the best companies to work for in India.

Critical Success Factors:

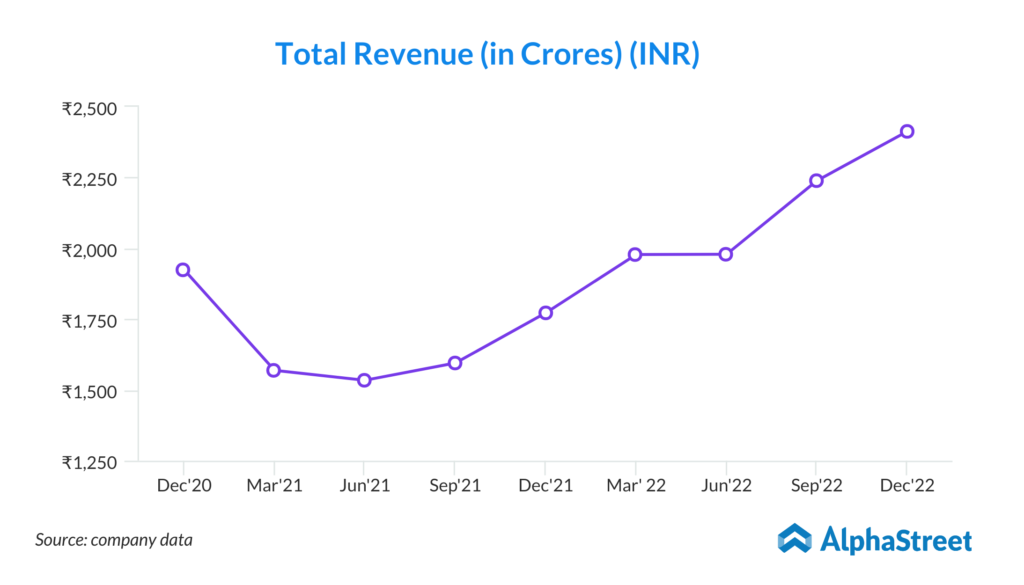

- AU Small Finance Bank’s credit growth remained strong at 7% QoQ and cumulative credit growth for FY23YTD stands at 20%. The bank is on course to deliver 28-30% YoY growth in FY23E. The credit growth trajectory during 9MFY23 has been robust, with a steady improvement in sequential loan growth. Disbursements grew sharply by 16% QoQ during Q3FY23, largely driven by the commercial banking division and HL. However, growth in wheels and SBL continued to lag behind overall advance growth. The management expects full-year FY23 credit growth to exceed the 25% mark, considering Q4FY23 as the strongest quarter. Overall, the data suggests that the bank has been performing well in terms of credit growth, driven by the commercial banking division and HL.

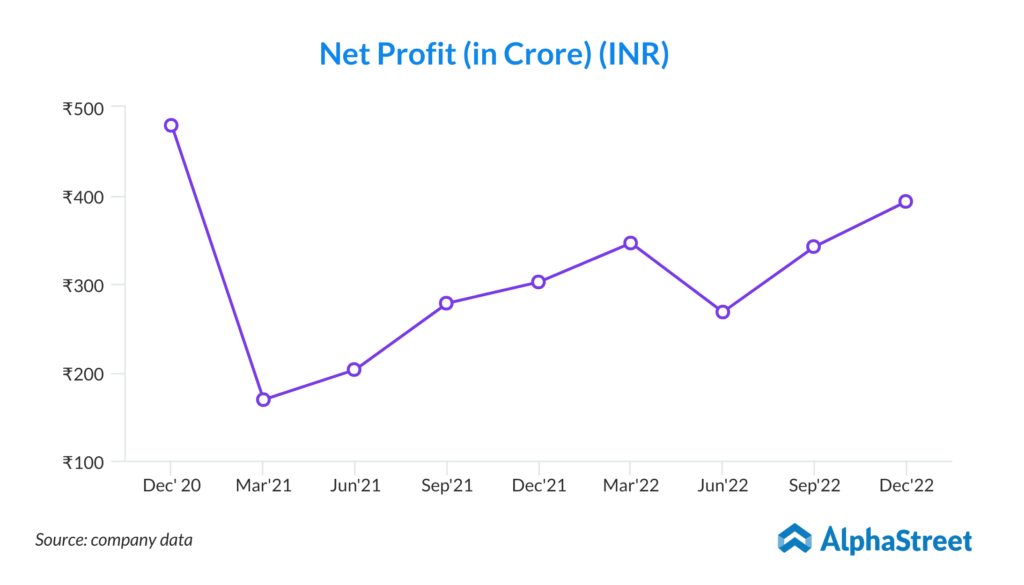

- AU Small Finance Bank’s asset quality remains pristine, with 81% of its advances originated post-pandemic having a gross non-performing asset (GNPA) ratio of only 0.6%. The bank’s asset quality performance during the COVID phase reflects the quality of its asset franchise, resiliency of its customer base, strong risk management, and tight credit filters. The bank has maintained its pristine asset quality even during the post-COVID era, with a steady decline in the GNPL ratio to 1.8% in Q3FY23 compared to 2.6% in Q3FY22 and 1.9% in Q2FY23. The strong provision coverage ratio (PCR) of 72% also provides comfort. Slippages have continued to remain at pre-COVID levels, at approximately 1.6% (Rs2.3bn), while recoveries broadly matched slippages at Rs2bn (including write-offs at Rs0.2bn). The management sounds confident about sustaining the asset quality going forward, as most of its business segments are witnessing improving cash flow and strong collections of 107% during Q3FY23.

- AU Small Finance Bank will continue to invest in building up its franchise. Over the past two years, the bank has been using its strong core operations to build up the ‘AU franchise.’ Since March 2020, it has added over 10,000+ workforces and 350+ banking touchpoints. The bank invested approximately Rs2.6bn towards building new product lines, brand building, and distribution expansion during FY22. During 9MFY23, it invested Rs3.5bn towards franchise build-up. The investments are starting to show positive results, such as the encouraging adoption of AU 0101 (around 30% of total ~3.5mn customers are monthly active on AU 0101), approximately 30% of total savings account acquisition via video banking, and 0.3mn live credit cards with 53% of cards to new-to-bank customers.

- AU Small Finance Bank has seen encouraging traction in its newly launched credit card portfolio with 0.39 million credit cards issued since the launch, out of which 53% of the cards were issued to new-to-bank (NTB) customers and 32% to first-time credit card users. The average spend per card is already in line with the industry average, which reflects the quality of customers. The bank has tied up with Pine Labs and PayU on point-of-sale (PoS) and online payments to facilitate no-cost equated monthly instalments (EMI).

Key Challenges:

- AU Small Finance Bank’s net interest margins (NIMs) remained stable at 6.2% during Q3FY23. This was mainly due to the equity capital raising during Q2FY23 and the rationalization of deposit rates, which led to a lower increase in the incremental cost of funds compared to the repo rate hike in the past 9 months. However, the strong systemic credit growth and tight liquidity are intensifying competition in deposits, and this is likely to result in higher deposit rates in the future. This has caused a 30bps QoQ decline in the incremental spread, with a 23bps QoQ increase in the cost of funds being the main reason. This poses a risk of NIM compression over FY24E. The management has stated that it is working to calibrate its funding mix to mitigate the adverse impact on NIM due to higher deposit costs. Overall, the data suggests that while NIMs have remained stable in the near term, there is concern over the trajectory of NIMs due to the decline in incremental spread and the potential increase in deposit rates in the future.

- Any slowdown in the Indian economy can lead to slower loan growth and higher credit costs for AU Small Finance Bank. As a result, the bank may face challenges in maintaining its profitability and asset quality. AU Small Finance Bank relies on its retail deposit franchise to fund its lending activities. If the bank experiences slower growth in its deposit base, it may need to rely on more expensive sources of funding, which could put pressure on its net interest margin (NIM) and profitability. The bank’s NIM is a key driver of its profitability. Any decline in NIM due to increased competition or higher funding costs could negatively impact the bank’s earnings.

- While AU Small Finance Bank has maintained a strong asset quality, any deterioration in the quality of its loan book could lead to higher credit costs and impact the bank’s profitability. Changes in regulations or policies by the Reserve Bank of India (RBI) or other regulatory authorities could impact the operations of AU Small Finance Bank. The bank may need to incur additional costs to comply with new regulations or may face restrictions on its lending or deposit-taking activities.

- AU Small Finance Bank has a concentrated loan book, with a significant portion of its loans being extended to the micro, small, and medium enterprises (MSME) segment. Any adverse developments in the MSME sector could impact the bank’s asset quality and profitability. Like other financial institutions, AU Small Finance Bank faces liquidity risk. In case of a sudden outflow of deposits or other funding sources, the bank may need to liquidate assets or rely on expensive sources of funding, which could impact its profitability.