Company Overview

Atul is a diversified and integrated Indian chemical company, part of the Lalbhai Group, Gujarat. It operates mainly in two segments: Life Science Chemicals and Performance and Other Chemicals, offering products used in various industries across nine business units. Presenting below its Q2 FY26 Earnings Results.

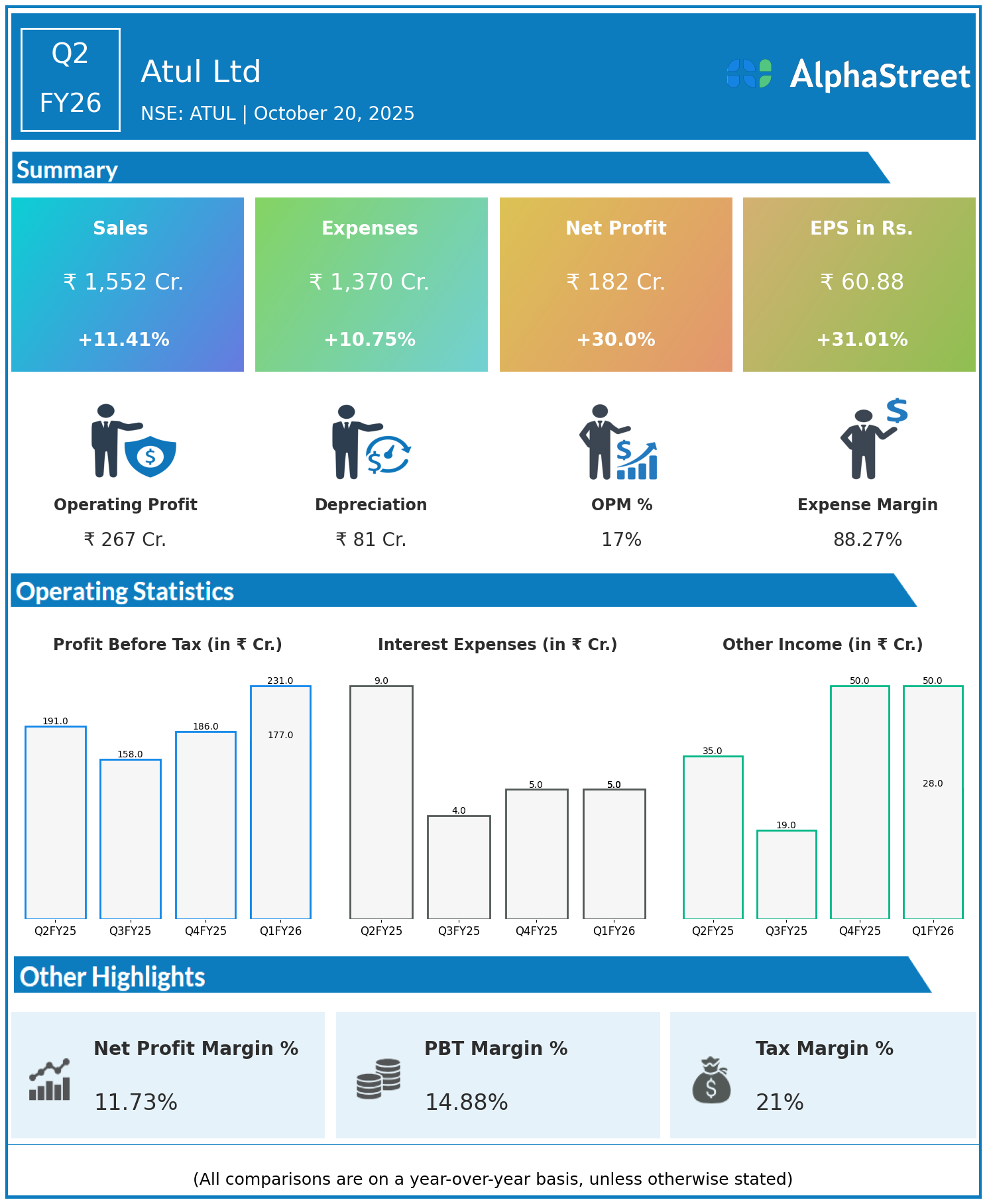

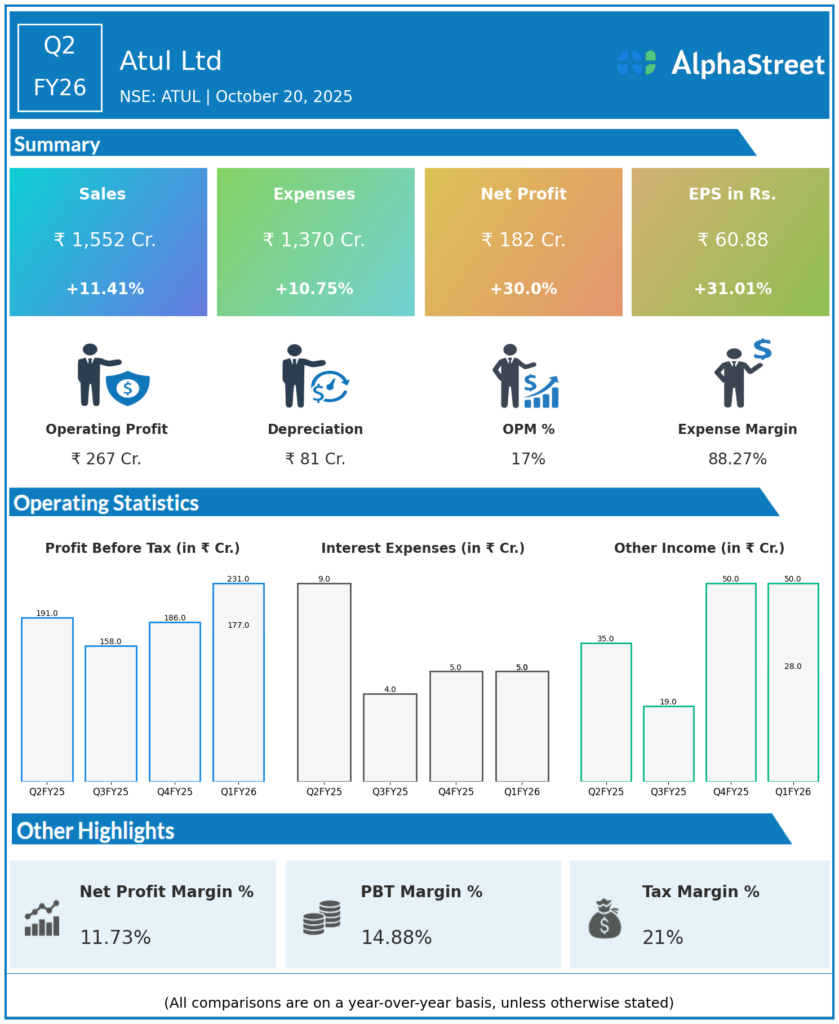

Q2 FY26 Financial Results

- Revenue for Q2 FY26 was ₹1,552 crore, up 11.41% year on year.

- Total expenses were ₹1,370 crore, a 10.75% increase year on year.

- Consolidated net profit increased by 30.0% to ₹182 crore compared to ₹140 crore in the same quarter last year.

- Earnings Per Share (EPS) rose 31.01% to ₹60.88 from ₹46.47.

Operational Highlights

- Both main segments reported solid growth: Life Science Chemicals and Performance Chemicals.

- Margins improved due to operational efficiencies and a favorable product mix.

- Continued investment in innovation and capacity expansion supports sustainable growth.

Outlook

Atul Ltd aims to maintain growth momentum through product diversification, strengthening market leadership, and focusing on sustainability initiatives. The company is well positioned for long-term value creation amid favorable industry trends.

Explore the company’s past earnings and latest concall transcripts, click here to visit the AlphaStreet India News Channel.