Asahi India Glass Ltd (AIS), India’s leading integrated glass solutions provider and a prominent player in automotive and architectural glass, reported a challenging quarter for Q2FY26.

Financial Highlights:

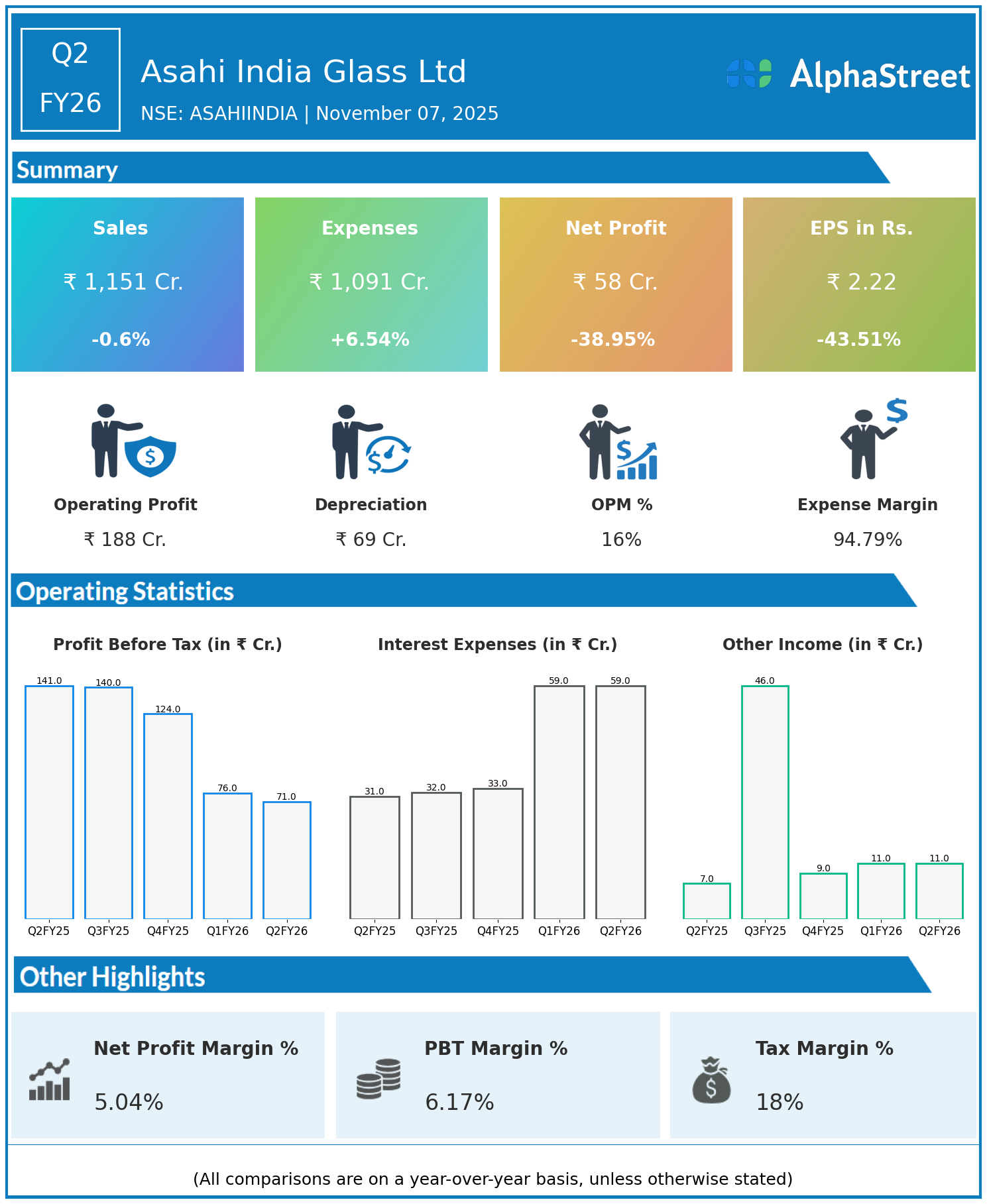

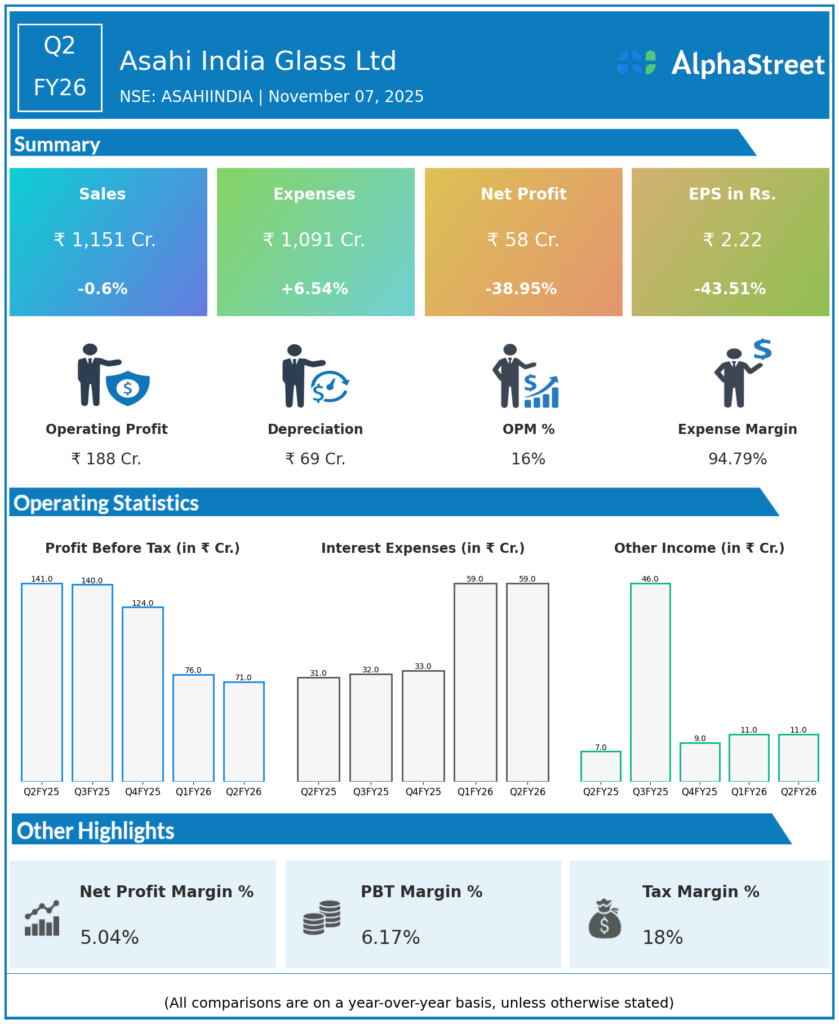

- Revenues for Q2FY26 stood at ₹1,151 crore, marginally lower by 0.6% from ₹1,158 crore in the previous year’s quarter.

- Total expenses increased 6.54% to ₹1,091 crore, up from ₹1,024 crore last year.

- Consolidated net profit plunged 38.95% to ₹58 crore, down from ₹95 crore in Q2FY25.

- Earnings per share fell 43.51% to ₹2.22 from ₹3.93.

Despite nearly steady top-line performance, the sharp rise in expenses impacted margins significantly. Increased raw material, energy, and overhead costs contributed to the profit slide.

Outlook:

AIS remains focused on innovation and operational efficiency across its value-added glass product lines. The company’s leadership in both automotive and architectural segments positions it for long-term recovery once cost pressures subside and end-market demand improves.

This quarter’s results highlight the immediate challenges from higher expenses, but AIS’s diversified portfolio and established market presence provide a base for future growth.

Explore the company’s past earnings and latest concall transcripts, click here to visit the AlphaStreet India News Channel.