“Gravita has signed an MoU to develop a battery recycling plant via JV in Oman with a annual capacity of 6000 metric ton per annum in Phase I. With the establishment of this plant, Gravita would expand its entry into the Middle East.”

– Yogesh Malhotra, Chief Executive Officer

Stock data

| Ticker | GRAVITA |

| Exchange | BSE and NSE |

| Industry | Non Ferrous Metals |

Price Performance:

| Last 5 days | -0.37% |

| YTD | +34.9% |

| Last 1 year | +128% |

Company description:

Established in 1992, Gravita India Ltd is one of the largest lead producers in India. The company’s business is organized across four specialized verticals: Lead Recycling (flagship), Aluminum recycling, Plastic recycling and Turnkey projects.

The company also has expertise in the recycling of used batteries, cable scrap/other Lead scrap, Aluminum scrap, Plastic scrap, etc.

Product Portfolio:

Gravita’s product portfolio is classified into 5 verticals:

Lead recycling, Aluminium recycling, Plastic recycling, Rubber recycling, and Turnkey Solutions. Some of its products are Pure Lead, Specific Lead Alloy, Lead sheets, Lead powder, Pet flakes and many more.

Export:

Gravita India Limited exports ~38% of its total turnover of the company to countries outside.

Manufacturing Units:

The Company has 11 Recycling plants with a Production capacity of 2.05 lac +, of which 30% of its capacity is from overseas. In FY23, its Capacity utilization was 67%.

User Industries:

The company provides services in four key segments: Battery Manufacturers, Cable manufacturing Industries, Paint & Pigment industries, Die Casting Industry and Plastic industries.

Customer Base:

The company has a global clientele of 375+ customers in Asia, the Middle East, Europe and the Americas, spanning 38+ countries. Its India operations cater to 230+ domestic customers in 22 states, and 90+ customers in 36 countries around the world.

The company’s main clients include names like Schneider Electric, Exide, Tata Batteries, KEC, Amara Raja, KEI, Prysman, Panasonic, etc.

Geographical Revenue:

The Company generates 38% of its revenue from outside India and 62% of its revenue from India.

Procurement Network:

It has 27 Own yards, 1500+ Touch points across the globe, with a Scrap collection of 2,05,000 MT+ in FY23. In FY23, 46% of Raw materials was domestically collected within India.

Order Book:

The company has an order book of 60,000 MT+ as of March 2023.

Future Plans:

Gravita aims to increase its Non-Lead business to 25%+ by 2027 and to enter into new verticals like E-Waste, Lithium, Rubber, Copper & Paper. It also aims to increase its capacity to 4,25,000 MTPA by 2027. It further aims to grow its topline and ROCE by 25%.

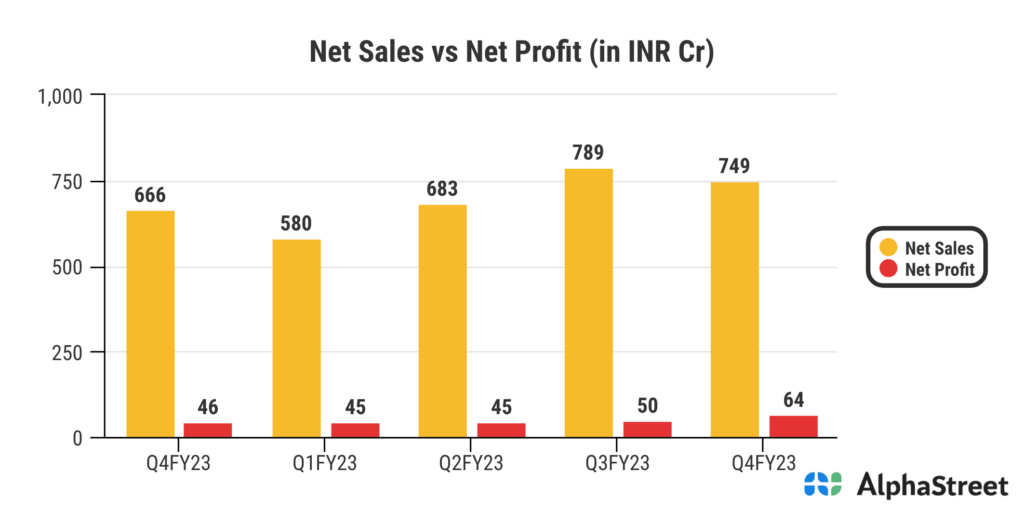

Financials:

What we like:

- Ambitious management team with years of experience:

Gravita India Ltd. was founded by entrepreneurs operating in regional markets which now over time has been able to establish business in India and outside India with plans to take it to a higher level. The company has gone down the journey of institutionalizing their companies, professionalizing their management teams and have successfully scaled across different regions within India despite starting as local jewelers.

- Reinforcing specialist position in secondary lead – Poised to grow:

GIL has a specialist position in secondary lead manufacturing, its core competencies includes a deeply-embedded global lead scrap collection network and plants that are located close to these scrap collection centers. R&D expertise and sound knowledge around the science of lead has reinforced its turnkey services offering for third party clients in recycling infrastructure, thus opening up a growing revenue stream and enabling it to continuously improve its technical services.

- The informal to formal shift will help the company achieve its bottomline:

With redefining of Battery Waste Management Rules (BWMR), Extended Producers Responsibility (EPR) and stricter implementation of GST, the scrap availability for the formal recycling sector has increased and is further expected to grow. GIL having Pan India presence and association with OEM’s will benefit the most from this shift.

GIL is slated to reap and enjoy most of the benefit emanating out of the structural shift as the demand and price of lead acid would only grow and is going to play an indispensable role which is an emerging tailwind for GIL.

Factors to consider:

- Risks from competitors and the entry of miners and OEMs into recycling. However, in reality, due to higher focus on battery recycling, battery OEMs prefer recycled Lead over mined Lead due to lower relative profitability.

- Amara Raja Batteries Ltd. (major client) is constructing a battery recycling unit to get backwardly integrated. Though this can hit GIL’s volumes but the major shift from the unorganized to organized volume (2-3x additional volumes) will fill the gap.

- Sri Lanka business which is 5-7% of total revenue is running at a slower pace hence volume contribution will be lower in the future.

- GIL has no hedging for Aluminium division as of now but management is planning to get it done by H1FY24.

- Adverse global commodity prices, economic & industrial slowdown, macro events, oversupply and broader cyclicality can impact recycling business realizations, margins and volumes.