Apollo, established in 1972, manufactures automatic bias and radial tyres, and tubes. It has plants in Kochi, Vadodara, Pune, and Chennai. The product profile includes prominent tyre brands in the T&B, light truck, passenger car, and farm vehicle segments in India, catering to both original equipment manufacturers, and the replacement market.

Financial Results:

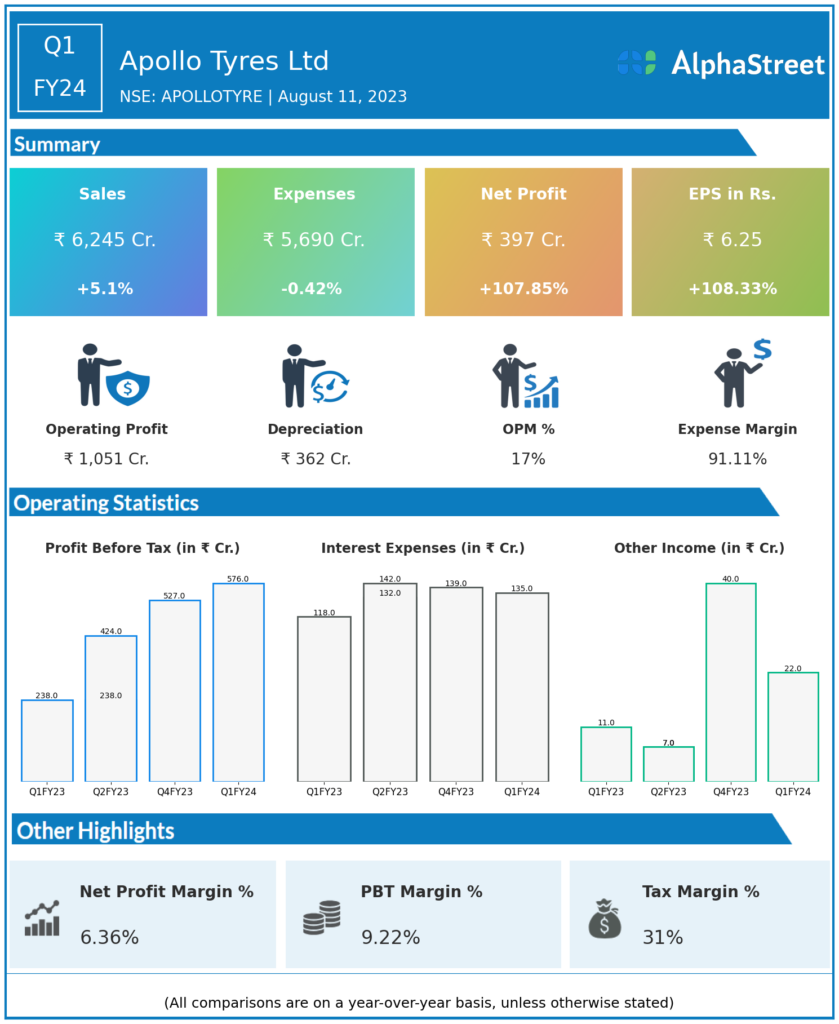

Apollo Tyres Ltd reported Revenues for Q1FY24 of ₹6,245.00 Crores up from ₹5,942.00 Crore year on year, a rise of 5.1%.

Total Expenses for Q1FY24 of ₹5,690.00 Crores down from ₹5,714.00 Crores year on year, a fall of 0.42%.

Consolidated Net Profit of ₹397.00 Crores up 107.85% from ₹191.00 Crores in the same quarter of the previous year.

The Earnings per Share is ₹6.25, up 108.33% from ₹3.00 in the same quarter of the previous year.

*It is important to note that the way the results have been accounted for are slightly different than the ones the companies may choose to publish.

*The presented data is automatically generated. It may occasionally generate incorrect information.