Founded in the year 1863, Bombay Burmah Trading Corporation Limited (BBTCL) is a flagship Company of Wadia Group.

Originally BBTCL was formed as a public company to carry out Teak business of William Wallace and was catering to domestic demands. Later in 1913 BBTCL turned to tea plantations by investing in Tea estates in South India.

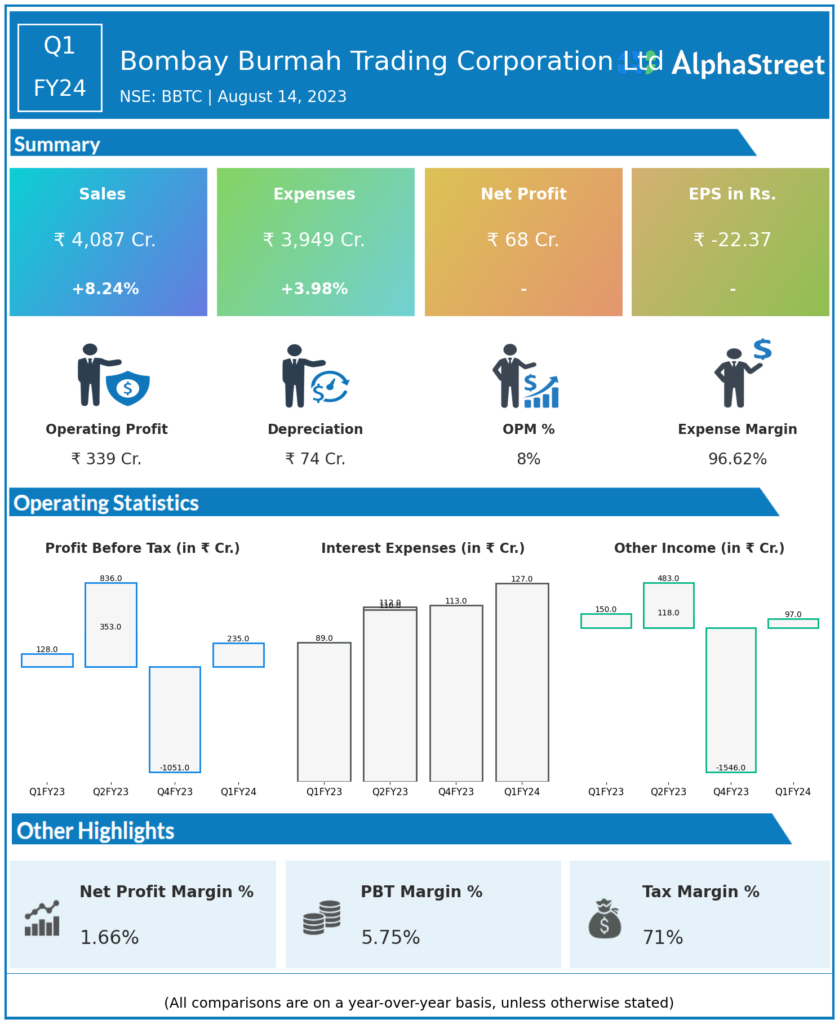

Financial Results:

Bombay Burmah Trading Corporation Ltd reported Revenues for Q1FY24 of ₹4,087.00 Crores up from ₹3,776.00 Crore year on year, a rise of 8.24%.

Total Expenses for Q1FY24 of ₹3,949.00 Crores up from ₹3,798.00 Crores year on year, a rise of 3.98%.

Consolidated Net Profit of ₹68.00 Crores from ₹0.00 Crores in the same quarter of the previous year.

The Earnings per Share is -₹22.37, from -₹23.62 in the same quarter of the previous year.

*It is important to note that the way the results have been accounted for are slightly different than the ones the companies may choose to publish.

*The presented data is automatically generated. It may occasionally generate incorrect information.