“In conclusion, short-term headwind aside, the fundamentals and prospects of HIL’s business remain attractive, and we remain on course to achieve our 2026 ambition of $1 billion turnover with robust profitability.”

– Mr. Akshat Seth, Managing Director & CEO on Q4FY23 Results

| Stock Data | |

| Ticker | HIL |

| Exchange | NSE |

| Industry | CONSTRUCTION |

| Price Performance | |

| Last 5 Days | -0.37% |

| YTD | +16.86% |

| Last 12 Months | -13.21% |

*As of 03.07.2023

Company Description:

HIL Ltd. operates in multiple segments within the building materials industry. The main segments in which the firm operates are as follows:

- Roofing Solutions: HIL Ltd. is a leading player in the roofing solutions segment. The company manufactures and sells a wide range of roofing products, including roofing sheets, tiles, metal roofing products, and other related accessories. These products are designed to provide durability, weather resistance, and energy efficiency to meet the diverse roofing needs of residential, commercial, and industrial buildings.

- Building Solutions: HIL Ltd. specializes in building insulation materials, which contribute to thermal and acoustic insulation in buildings. The company produces insulation boards, panels, and related solutions that help in reducing heat transfer, minimizing energy consumption, and enhancing comfort. These products are widely used in residential, commercial, and industrial constructions.

- Plumbing Solutions: HIL Ltd. manufactures pipes and allied products that find application in plumbing, irrigation, and other infrastructure projects. The company produces high-quality pipes, fittings, and related accessories that are used in water supply systems, sewage systems, and agricultural applications. These products comply with industry standards and are known for their durability and performance.

- Other Building Materials: Apart from the above-mentioned segments, HIL Ltd. also produces and sells other building materials that complement their core offerings. This includes products like autoclaved aerated concrete (AAC) blocks, dry-mix mortar, and construction chemicals. These additional building materials contribute to the overall construction process and offer comprehensive solutions to customers.

- Flooring Solutions: HIL Ltd. offers a range of flooring solutions designed to cater to diverse customer requirements. The company manufactures flooring products such as tiles, laminates, and vinyl flooring options. These flooring solutions provide aesthetics, durability, and ease of maintenance, making them suitable for residential, commercial, and industrial applications.

Financial Results:

“FY24, April, however, has started with slower volume offtake due to the festive season and high volumes of rains, and this meant a slightly muted demand sentiment at the start of the season. However, recent trends indicate that the season is picking up, and we believe that this will offset the slow start. And in the next 4 to 6 weeks, we should cover the deficit from the soft start that we experienced in April. Overall, last year, the high cost of raw material did impact margins adversely. And it will remain a factor in this quarter as well.”

– Mr. Akshat Seth, Managing Director & CEO on Q4FY23 Results

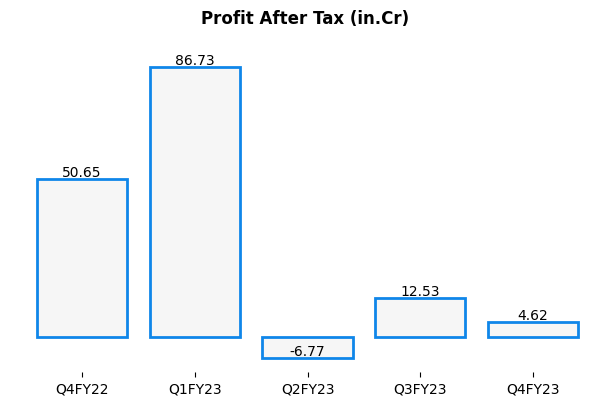

- Hil Ltd reported Revenues for Q4FY23 of ₹863.27 Crores down from ₹949.44 Crore year on year, a fall of 9.08%.

- Total Expenses for Q4FY23 of ₹862.75 Crores down from ₹886.72 Crores year on year, fall of 2.7%.

- Consolidated Net Profit of ₹4.62 Crores down 90.88% from ₹50.65 Crores in the same quarter of the previous year.

- The Loss per Share is ₹6.13, down 90.91% from ₹67.41 in the same quarter of the previous year.

Key Strengths:

- Strong Brand Reputation: HIL Ltd. has established a strong brand reputation over several decades of operation. The company is well-known for its quality products, reliable performance, and customer-centric approach. The brand recognition and trust it has built contribute to its market leadership and customer loyalty.

- Diverse Product Portfolio: HIL Ltd. offers a diverse portfolio of building materials across various segments. This wide range of products allows the company to cater to the diverse needs of different customer segments. The comprehensive product portfolio gives HIL Ltd. a competitive edge and enables cross-selling opportunities.

- Technological Expertise: The company possesses strong technological expertise in manufacturing building materials. HIL Ltd. invests in research and development to continuously innovate and improve its products. This technological prowess enables the company to stay ahead of market trends, meet customer demands, and offer innovative solutions.

- Extensive Distribution Network: HIL Ltd. has established an extensive distribution network that spans across India. The company has a wide presence in both urban and rural areas, ensuring the availability of its products to a large customer base. The robust distribution network strengthens its market reach and enhances customer accessibility.

- Manufacturing Capabilities: HIL Ltd. operates modern and efficient manufacturing facilities that adhere to high-quality standards. The company’s production capabilities enable it to meet market demands effectively and efficiently. The manufacturing excellence contributes to consistent product quality, cost control, and timely delivery.

Key Challenges:

- Raw Material Price Volatility: The prices of raw materials, such as steel, cement, and polymers, which are used in the production of building materials, are subject to fluctuations in global and domestic markets. Volatility in raw material prices can impact the company’s profitability and margins. HIL Ltd. needs to effectively manage and mitigate the risks associated with raw material price volatility.

- Economic Uncertainty: The performance of the building materials industry is closely linked to the overall economic conditions. Economic fluctuations, such as changes in GDP growth, interest rates, and investment levels, can impact the demand for construction and infrastructure projects. Economic uncertainty can affect the company’s revenue growth and profitability.

- Supply Chain Disruptions: HIL Ltd. relies on a complex supply chain to source raw materials, manufacture products, and distribute them to customers. Disruptions in the supply chain, such as transportation constraints, logistics challenges, and availability of raw materials, can impact the company’s production and delivery capabilities. Managing supply chain risks and ensuring continuity is crucial for HIL Ltd.

- Currency Exchange Rate Fluctuations: HIL Ltd. operates in domestic as well as international markets, which exposes the company to currency exchange rate fluctuations. Changes in exchange rates can impact the company’s export-import business, profitability, and competitiveness in global markets. Effective currency risk management is essential to mitigate the impact of exchange rate fluctuations.

- Competitive Market Environment: The building materials industry in India is highly competitive, with the presence of both domestic and international players. HIL Ltd. faces competition from established companies as well as new entrants. Sustaining market share and profitability in such a competitive landscape requires continuous innovation, cost management, and differentiation strategies.