Symphony was established in 1988, in Ahmedabad, India. The company is engaged in the manufacturing and trading of residential, commercial, and industrial air coolers in the domestic and international markets. It is the largest air cooler manufacturer in the world. 97% of the revenue comes from the sale of Air coolers. The organized air cooler market is 30% of total market and out of this, Symphony has 50% market share. The company has one manufacturing plant and 25 offices in India. Internationally, it operates four manufacturing plants and two offices. Additionally, Symphony has six overseas subsidiaries managing operations in different countries, though it does not have any standalone overseas office locations. Presenting below are its Q1 FY26 earnings results.

Q1 FY26 Earnings Results

-

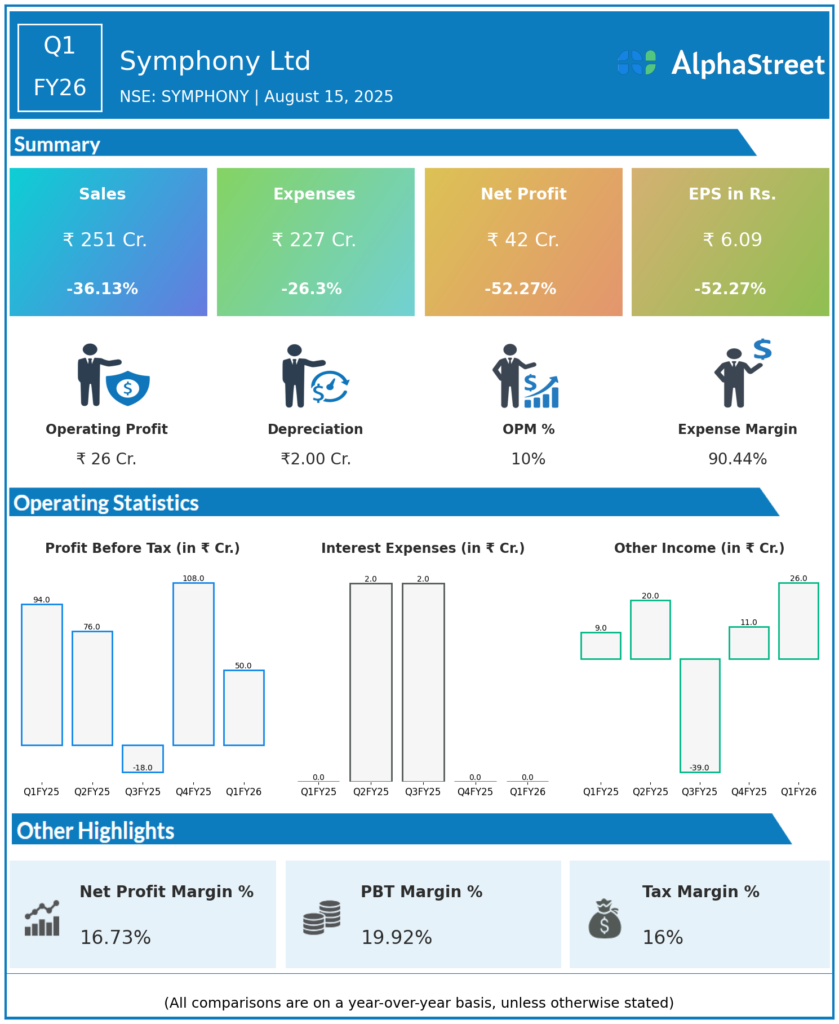

Revenue: ₹251 crore, down 36.3% year-over-year (YoY) and 20.2% quarter-on-quarter (QoQ).

-

Net Profit (PAT): ₹42 crore, down 52.2% YoY and 12.5% QoQ.

-

EBITDA: ₹26 crore, down 70% YoY; EBITDA margin compressed to 10.2% from 22.3% last year.

-

EPS: ₹6.09, down from ₹12.80 YoY and ₹7.00 QoQ.

-

Expenses: ₹227 crore, down 26.3% YoY and 19.8% QoQ.

-

Symphony’s performance was affected by strong seasonal headwinds and a challenging high base last year.

-

The company reported a dividend of ₹1 per share (face value ₹2) for FY25-26 interim.

Management Commentary & Strategic Highlights

-

The company acknowledged the seasonal softness in demand in the first quarter and attributed the YoY decline to a high base of Q1 FY25.

-

Symphony is accelerating growth in all-season and counter-seasonal categories such as tower and kitchen cooling fans, large space venti-cooling (LSV), and water heaters.

-

The company leverages its innovation, brand equity, and distribution network for future growth.

-

Management aims to mitigate seasonality effects by building a broader product portfolio across seasons.

Q4 FY25 Earnings Results

-

Symphony reported Q4 revenue of ₹381 crore which was up by 14.7 percent on the YoY basis

-

Net profit was ₹79 crore, up by 64% on the YoY basis.

-

EBITDA margin stood at approximately 18%, higher than Q1 FY26.

-

Seasonally stronger quarter compared to Q1 FY26.

To view the company’s previous earnings and latest concall transcripts, click here to visit the Alphastreet India news channel.