Awfis Space Solutions Limited (NSE: AWFIS) reported a strong financial performance for the third quarter ended December 31, 2025, driven by robust growth in its core co-working business and operating leverage benefits.

Quarterly Performance

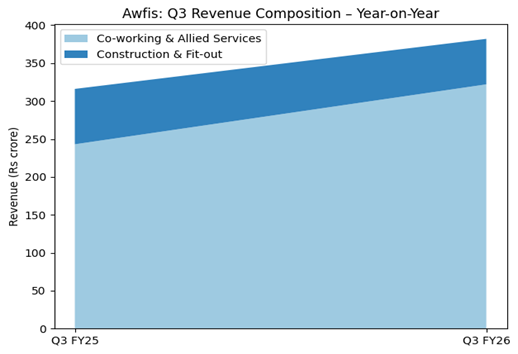

For Q3 FY26, consolidated revenue from operations rose 20% year-on-year to ₹382 crore, compared with ₹318 crore in the same period last year. Net profit increased 43% YoY to ₹22 crore, up from ₹15 crore, reflecting scale efficiencies and margin expansion.

Operating EBITDA for the quarter stood at ₹139 crore, marking a 30% YoY increase, while EBITDA margin expanded to 36.5% from 33.8%, supported by a higher share of mature centres and improved operating leverage.

Segment Performance

- Co-working and Allied Services revenue grew 32% YoY to ₹322 crore, driven by healthy demand from enterprise and Global Capability Centre (GCC) clients.

- Construction and Fit-out Projects (Awfis Transform) revenue declined 18% YoY to ₹60 crore, reflecting lower execution during the quarter.

Nine-Month Performance

For the nine months ended December 31, 2025, revenue from operations increased 25% YoY to ₹1,083 crore, while profit after tax (excluding exceptional items) rose 50% YoY to ₹48 crore, underscoring sustained momentum and improved profitability.

Operational Highlights

During the quarter, Awfis added 10 new centres, taking its total footprint to 257 centres with approximately 177,000 seats across 18 cities. Total operational capacity stood at 152,000 seats, representing a 25% YoY increase.

Strategic Update

The Board approved the slump sale of the Design and Build business to its wholly owned subsidiary, Awfis Transform Private Limited, for an initial consideration of approximately ₹26.6 crore, aimed at sharpening strategic focus and operational efficiency.

Outlook

With flexible workspaces accounting for a growing share of office leasing, Awfis remains well positioned to benefit from industry tailwinds. The company’s strong managed aggregation pipeline, expanding GCC portfolio, and disciplined capital allocation provide visibility for sustained, profitable growth.