Chalet Hotels Limited (NSE: CHALET) Hospitality operator sees double-digit RevPAR expansion and improves margins as it advances a 1,180-key development pipeline. Robust demand in the wedding and corporate segments offset temporary occupancy declines caused by renovations in the Mumbai region.

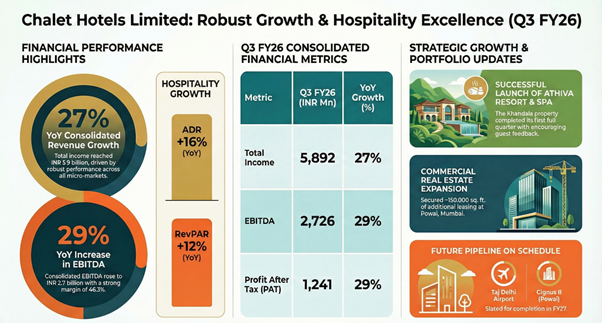

Chalet Hotels Limited reported a 27% year-over-year increase in consolidated revenue to ₹5.9 billion for the third quarter ended December 31, 2025. The company’s financial performance was supported by a 12% expansion in Revenue Per Available Room (RevPAR) to ₹10,162, driven largely by a 16% rise in Average Daily Rates (ADR) across its hospitality portfolio. While consolidated EBITDA rose 29% to ₹2.7 billion, management noted that ongoing renovation and construction activities in the Mumbai Metropolitan Region (MMR) had a temporary impact on occupancy levels.

Hospitality Growth

The quarter’s performance was primarily driven by the hospitality segment, which generated revenue of ₹4.9 billion, reflecting a 23% year-over-year increase. Key operational developments during the period included the full launch of Athiva Resort & Spa in Khandala and the rebranding of Courtyard by Marriott Aravali Resort as Aravali Marriott Resort & Spa. In addition, the company secured environmental clearance for its Hyatt Regency project in Airoli, representing a key milestone in its Navi Mumbai expansion plans.

Expansion Pipeline

The company is currently pursuing a strategic expansion of its premium lifestyle segment through its new brand, ATHIVA. Its development pipeline consists of approximately 1,180 rooms, including the 385-390 key Taj at Delhi International Airport, which is slated for completion by the fourth quarter of fiscal year 2027. In the commercial segment, Chalet is developing the Cignus II tower in Powai, expected to be operational in fiscal year 2027, as part of a plan to increase its leasable area from 2.4 million to 3.3 million square feet.

Financial Performance

For Q3 FY26, Chalet reported a consolidated EBITDA margin of 46.3%, an improvement of 76 basis points over the previous year. Profit after tax for the quarter was ₹1.2 billion, up 29% from ₹965 million in Q3 FY25. On a nine-month basis (9M FY26), consolidated revenue surged 84% to ₹22.4 billion, primarily due to the recognition of revenue from residential project handovers earlier in the year. Net debt was recorded at ₹20.1 billion as of the end of the period, with a cost of debt of 7.5%.

Investment Thesis (Bull vs. Bear)

Bull Case:

- Revenue growth is underpinned by significant ADR expansion in high-growth micro-markets such as Hyderabad, Bengaluru, and Pune, which benefit from increasing commercial activity and tech sector growth.

- The successful launch of the ATHIVA brand and a diversified revenue stream from commercial real estate, which saw 150,000 square feet of additional leasing this quarter, provide a foundation for long-term annuity income.

Bear Case:

- Occupancy levels declined to 68% from 70% a year ago, reflecting the impact of inventory additions and disruptive renovation work at key Mumbai properties.

- The company maintains a high capital expenditure commitment for its 1,180-room pipeline.

- hospitality segment’s EBITDA margin saw a slight contraction of 82 basis points on a nine-month basis compared to the prior year.

Execution Priorities

Management’s strategy focuses on maintaining operating momentum through the festive and wedding seasons while leveraging new inventory in Bengaluru and Khandala. Capital allocation is prioritized toward high-end hotels and luxury resorts in major Indian transit hubs and leisure destinations. Operational priorities include driving efficiencies through recently acquired assets and maintaining industry-certified workplace standards.

Industry Tailwinds

The company’s growth reflects broader trends in the Indian hospitality sector, characterized by sustained demand for Meetings, Incentives, Conferences, and Exhibitions (MICE) and leisure travel. Increased commercial activity and the expansion of Global Capability Centers (GCCs) have specifically bolstered performance in the Hyderabad and Bengaluru markets. Chalet has also aligned its operations with international sustainability standards, achieving a score of 67 in the Dow Jones Sustainability Index.