LT Foods Limited is one of the leading rice brands in India. The company focuses on the production and marketing of branded & non branded segments of Basmati rice in Indian as well as Overseas Market. Along with Basmati Rice, the company has also delved into the business of Organic Foods and other niche segments.

| Stock Data | |

| Ticker | DAAWAT |

| Exchange | NSE |

| Industry | FOOD |

| Price Performance | |

| Last 5 Days | -0.56% |

| YTD | -15.48% |

| Last 12 Months | +6.52% |

*As of 12.04.2023

Management Outlook & Company Goals

As per the management, the company plans to reinvest its earnings back into the business to strengthen its brand & distribution network in order to generate growth across all segments. LT Foods plans to leverage its existing strength in its distribution network and goodwill to introduce new product lines such as Ready to Cook, Ready to eat & other rice based snacks. These niche segments have the potential to secure higher margins that are less susceptible to volatilities in input costs. With the focus on growth and margin expansion, the company hopes to increase profitability in the coming years.

As a part of the firm’s capital allocation plan, the company has decided to keep its Debt to EBITDA ratio within 2x – 3x. Additionally, the company plans to carry out steady and sustained dividend payments to shareholders in the range of 20% – 30% of its standalone profits.

Key Strengths:

- Strong Supply chain and Robust Global Distribution Network: LT Foods transformation into an FMCG company requires a strong distribution network. The company has over the years built an extensive network of distributors and retailers in the domestic as well as the global markets. The company serves its customers through 1,52,000 plus retail outlets in India, 7,200 plus modern trade channels including hypermarkets, supermarkets, Cash n Carry etc and all leading e-commerce platforms.

The company also has more than 1300 distributors across the globe out of which more than 1200 distributors are in India and more than 100 distributors in the overseas market. The Company’s strong distribution network is a testimony to the Company’s sustained financial performance, year after year.

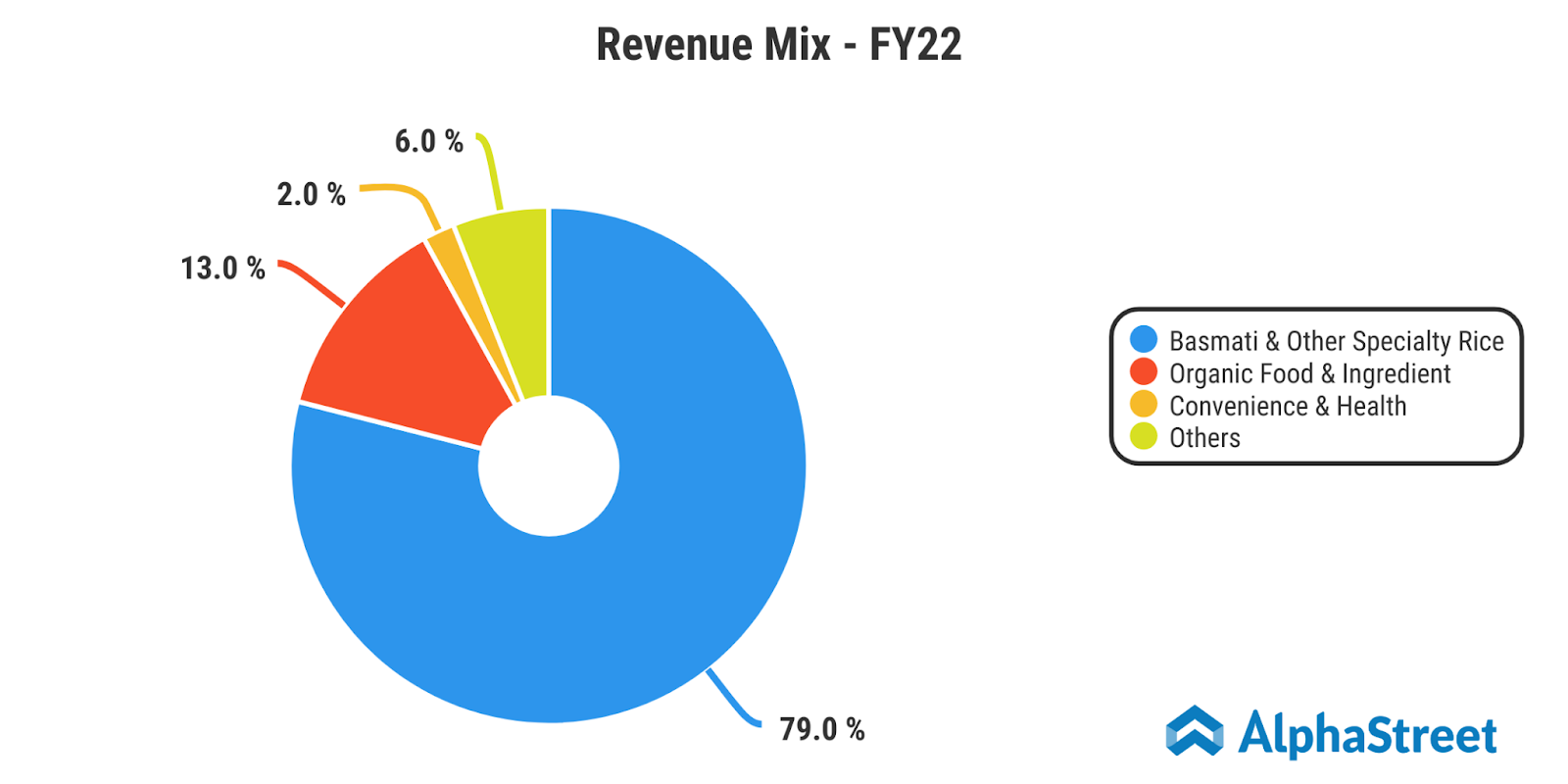

- Strong Brand: The company lays constant emphasis on its brand building initiatives to sustain consumer loyalty and limit opportunities for competition. Relying on a solid reputation, excellent brand recall and a commitment to consistently deliver value, LT Foods today has securely cemented its position as a global leader par excellence. It is evident in the company’s revenue mix.

- High entry Barrier: As the basmati industry requires huge inventory and thus it is a huge working capital intensive business therefore not many plates can enter the industry and stay to compete with established players like LT foods. Secondly, building a relationship with hotels and the restaurant industry required years of hard work which LT foods has already done. Once this trust is built, it becomes very hard for new players to break into the industry.

Key Risks:

- Freight Cost – Margin Impact: The profitability margins of the company are susceptible to freight costs. The shortage of freight containers on a global level had negatively impacted the profit margins of the company in previous quarters. As the freight costs pressures have cooled down, the margins are looking comparatively better. However, the rising inflations in raw materials have resulted in an increase in input costs.

- Susceptibility to volatile raw material prices and regulatory changes: LTF starts the paddy purchase in the third quarter and stores it for the rest of the year. Now, being a commodity, the prices of rice and paddy are susceptible to factors like supply, demand, rain and availability of healthy land.

The company usually enters into an understanding with customers for supply of rice, though this is not binding. Hence, exposure to risks related to any steep decline in paddy prices, subsequent to procurement, remains high.

Additionally, exports of agricultural commodities, including rice, are highly regulated. However, having strong brands, wide geographical reach and sourcing capabilities have helped the group maintain profitability.

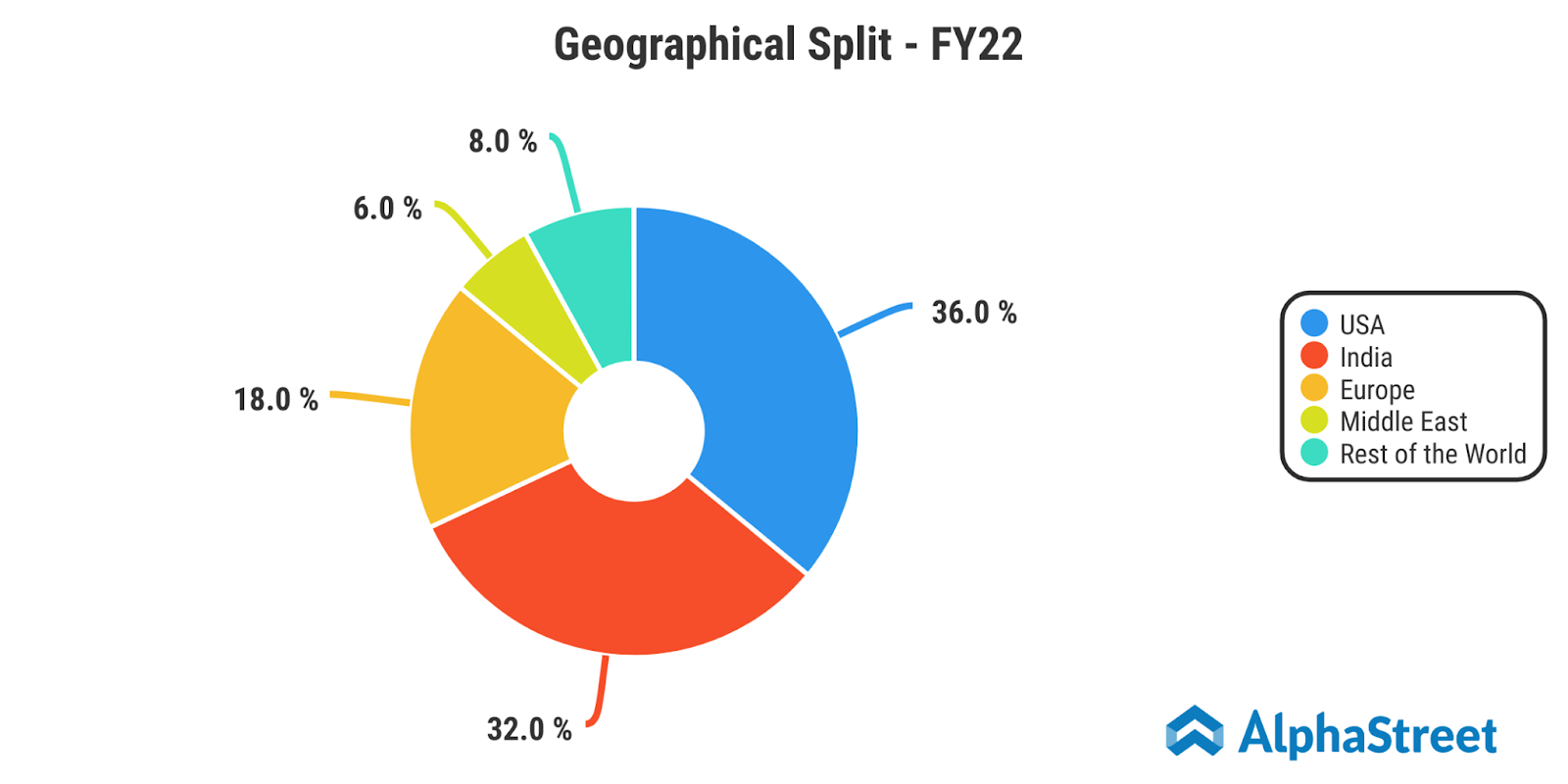

- Foreign Exchange Rate Risk: LTF derives 68% of its revenue from the global market making it susceptible to exchange rate fluctuations. However, the company has put in place a well-framed hedging policy that mitigates any potential risk due to currency volatility and causes a financial impact.

- Too many competitors in the space: In India, there are few major branded players in the Basmati rice business which dominate the local as well as the export markets.

- Geopolitical Risks: LTF is a global rice company having exports in more than 60 countries. Any geo-political tensions between major economies can cause supply & demand glut in turn affecting the prices of raw material and final products.

Valuation & Outlook

LTF’s consistent efforts on strengthening the brands, and widening distribution network, along with region & product diversification through organic & inorganic routes have been the strategy for growth. The margin is expected to improve in the coming quarters as freight costs are peaked out. We recommend holding the stock in your portfolio as a long term investment for an effective value unlocking.