UltraTech Cement is engaged in the manufacturing and sale of Cement and Cement related product primarily across globe.

Q3 FY26 Earnings Results

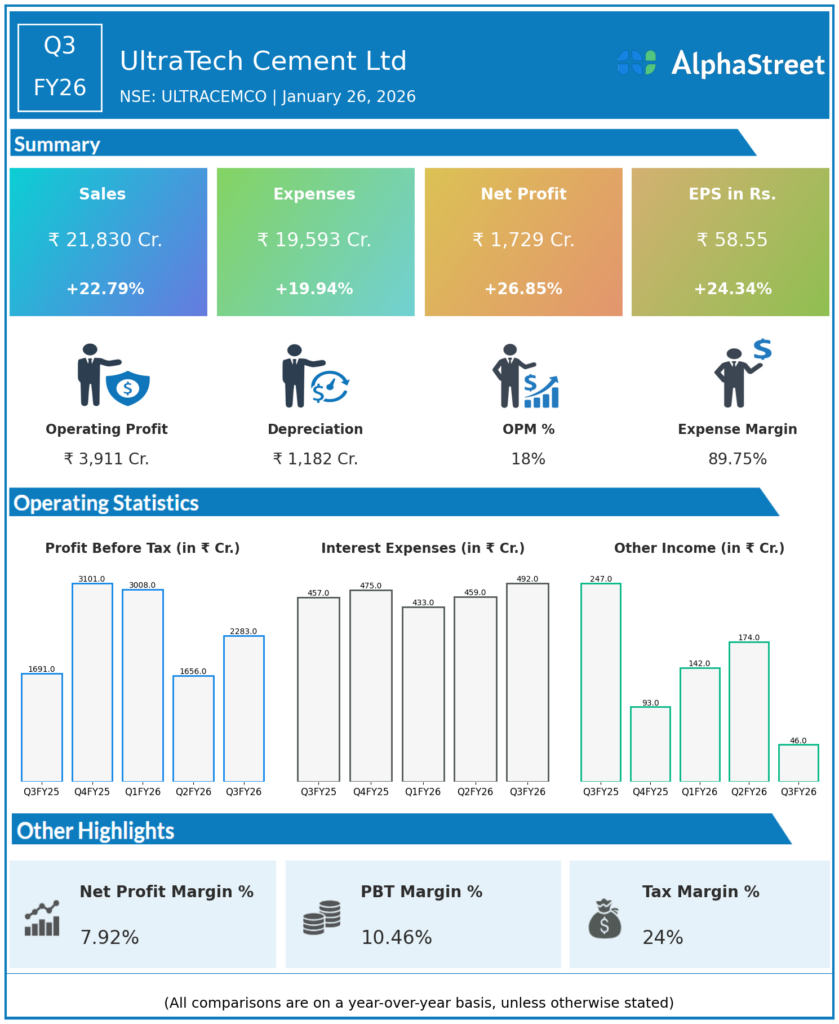

Revenue from Operations / Net Sales: ₹21,506 cr, up 22.5% YoY from ₹17,555 cr in Q3 FY25, +9.7% QoQ from ₹19,607 cr in Q2 FY26, driven by strong domestic grey cement volumes (+15.4% YoY to 36.37 MT) and Ready Mix Concrete (+25.8% YoY to ₹1,848 cr).

Operating PBIDT (EBITDA): ₹4,051 cr, up 28.9% YoY from ₹3,142 cr in Q3 FY25, +21.5% QoQ from ₹3,268 cr in Q2 FY26, with operating margin expanding 166 bps YoY to 18.81%.

Operating EBITDA per MT: ₹1,051/MT, up ₹140 YoY (+15.4%) and ₹97 QoQ (+10.1%), reflecting improved cost efficiency and capacity utilisation.

Profit After Tax (PAT): ₹1,725 cr (reported), up 26.9% YoY from ₹1,359 cr in Q3 FY25, +40.1% QoQ from ₹1,232 cr in Q2 FY26; PAT margin at 7.92% (up from 6.31% QoQ), with exceptional charge of ₹88 cr on new Labour Code provisions reducing reported PAT to ₹1,725 cr versus normalised ₹1,813 cr.

Total Expenses: ₹17,914 cr, up from ₹15,557 cr QoQ; Cost of Materials Consumed rose 30.6% YoY, outpacing revenue growth; Depreciation ₹1,182 cr (+3.0% QoQ), Employee Costs ₹1,041 cr (-2.2% QoQ), Interest ₹492 cr (+7.2% QoQ).

9M YTD Performance: Revenue ₹62,712 cr (+18.6% YoY), PAT ₹5,183 cr (+45.7% YoY), highlighting strong first-half momentum sustained through Q3.

Management Commentary & Strategic Decisions

Strong operational momentum driven by volume growth, market share gains from India Cements integration, and gradual easing of input costs; raw material costs/MT increased 6% YoY to ₹664/MT (improved clinker conversion ratio), whilst other costs/MT declined 7% YoY benefiting from operating leverage.

Strategic capital allocation remains disciplined with net debt-to-EBITDA at 1.08x and ₹2,357 cr capex deployed in Q3; company reiterated capacity expansion roadmap to add 22.8 MTpa and launch Cables & Wires business in Q3 FY27.

Green power mix improved to 41.1% in 9M FY26 with ESG target to reduce Net CO₂ emissions to 462 kg CO₂/MT cement by FY32, underlining transition focus amidst structural margin headwinds.

Q2 FY26 Earnings Results

Revenue from Operations: ₹19,607 cr, up 20.3% YoY from ₹16,301 cr in Q2 FY25, down 9.7% QoQ from Q1 FY26, reflecting seasonal weakness post-monsoon.

Operating EBITDA: ₹3,268 cr (PBIDT per estimates), up 45% YoY (est.), +3.0% QoQ; operating margin at 15.78% (up 334 bps YoY but down 495 bps QoQ due to seasonal factors and maintenance costs).

Profit After Tax: ₹1,238 cr, up 75.2% YoY from ₹704 cr in Q2 FY25, down 40.1% QoQ from Q1 FY26; PAT margin at 6.3% (up 197 bps YoY, down 418 bps QoQ).

Management Commentary Q2

Inline operational performance with volume growth offsetting seasonal demand trough; margin pressure reflected underlying cost inflation and competitive dynamics in cement markets, alongside higher effective tax rate drag.

To view the company’s previous earnings and latest concall transcripts, click here to visit the Alphastreet India news channel.