ABB India Limited is an integrated power equipment manufacturer supplying the complete range of engineering, products, solutions and services in areas of Automation and Power technology.

Financial Results:

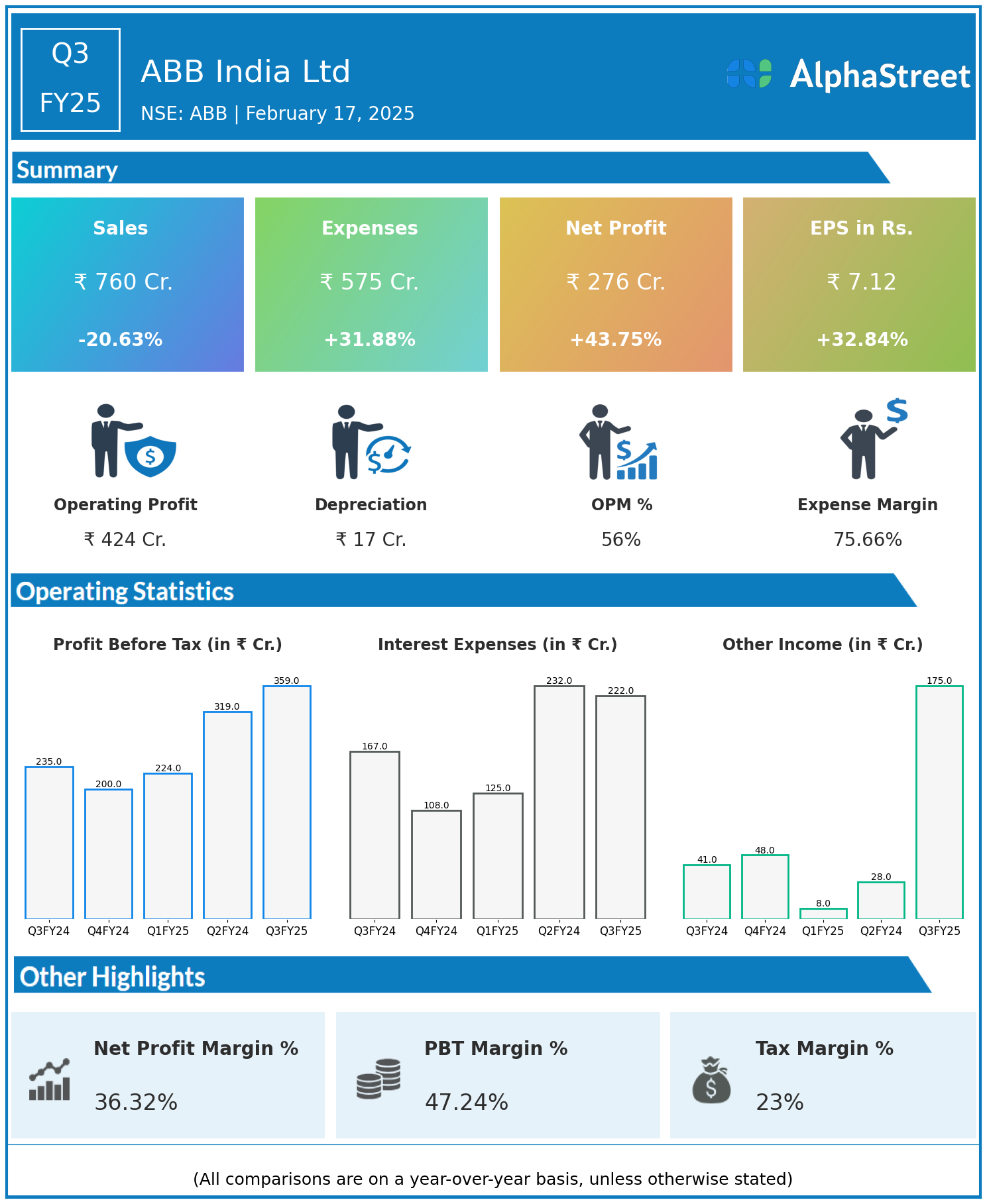

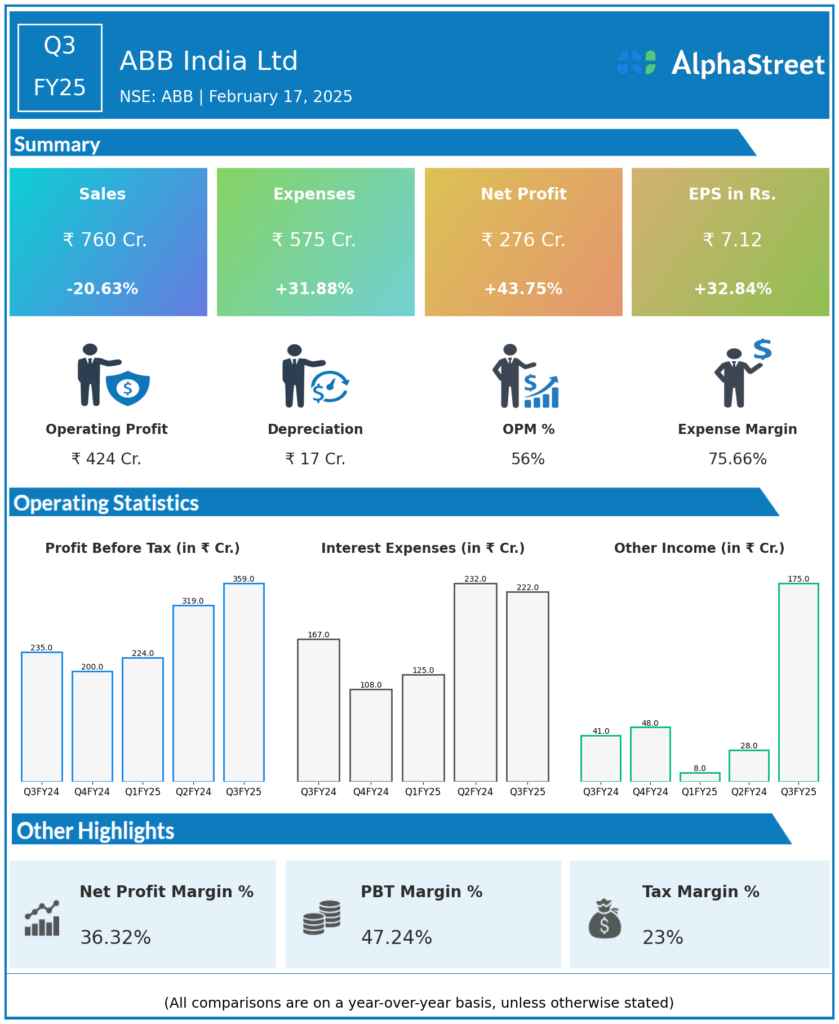

ABB India Ltd reported Revenues for Q3FY25 of ₹760.00 Crores down from ₹1,006.00 Crore year on year, a fall of 20.63%.

Total Expenses for Q3FY25 of ₹575.00 Crores up from ₹436.00 Crores year on year, a rise of 31.88%.

Consolidated Net Profit of ₹276.00 Crores up 43.75% from ₹192.00 Crores in the same quarter of the previous year.

The Earnings per Share is ₹7.12, up 32.84% from ₹5.36 in the same quarter of the previous year.