Wonderla Holidays is engaged in the business of Amusement Parks and Resort. Wonderla came up with their IPO in April 2014 to raise 181 cr. which went into funding their upcoming amusement park in Hyderabad, which was operationalized in 2016. The company was set up by Kochouseph Chittilappilly in 2000, the same promoter group also founded V-guard brand of stabilizers and runs V-Guard Industries.

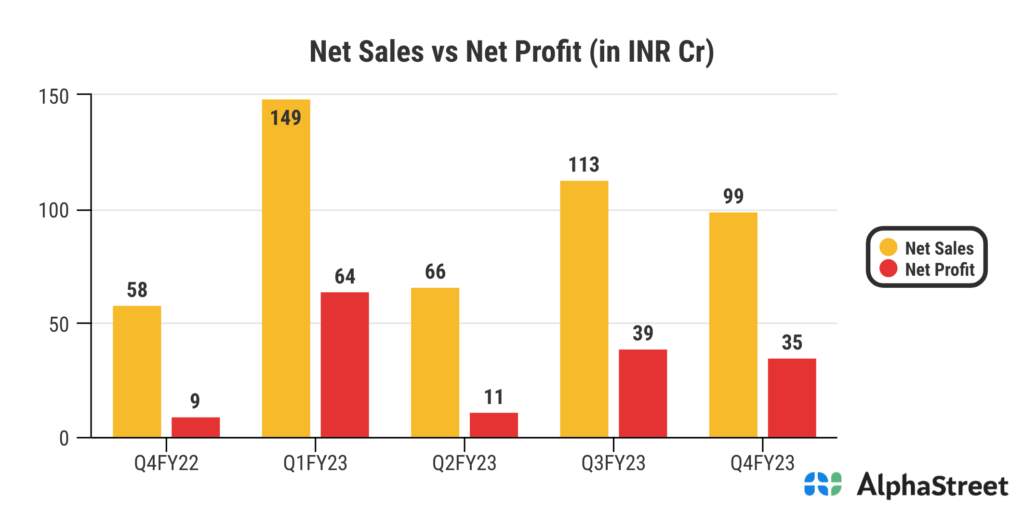

- Wonderla Holidays Ltd reported Total revenue for Q4 FY23 of ₹99 Crore, up from ₹58 Crore year on year depicting a growth of 71%.

- Total Expenses for Q4 FY23 of ₹65 Crore up, from ₹48 Crore year on year, a growth of 35%.

- Consolidated Net Profit of ₹35 Crore, up 289% from ₹9 Crore in the same quarter of the previous year.

- The Earnings per Share is ₹6.2, up 313% from ₹1.5 in the same quarter of the previous year.