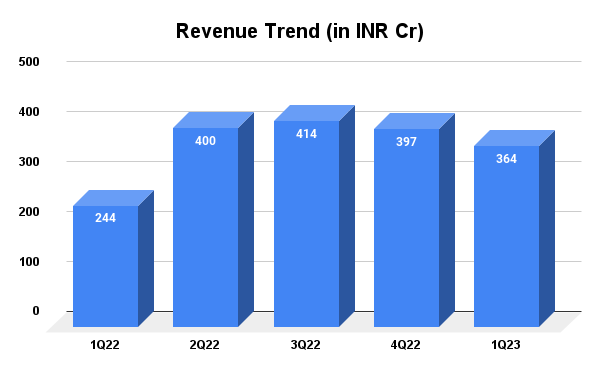

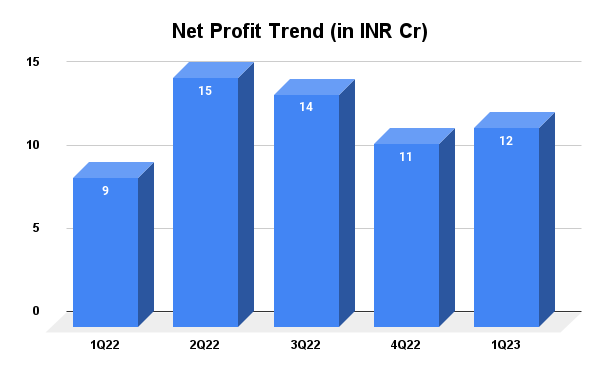

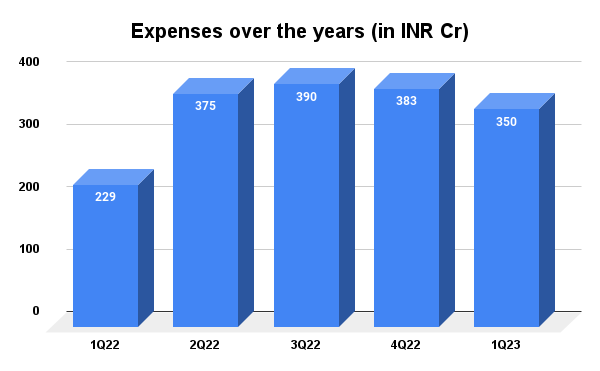

Pondy Oxides opened the FY23 with a robust performance wherein the total income grew 49% to INR 364 crores in Q1 FY23 from INR 243.97 crores in Q1 FY22. Net profit jumped 35% to INR 11.59 crores. Sequentially, the net profit rose 9%. The company has further managed its expenses very well as cost of raw materials consumed have gone down 16% from the last quarter.

Surprisingly, the interest cost for the company has reduced by over 7% on year resulting in an improved bottom line. Further, the EPS grew by 35% during the same period.

In addition to the positive quarter, the company has recommended issue of bonus shares subject to the approval of shareholders in the ratio of 1: 1 i.e. one new bonus equity share of INR 10 each to be issued for every one existing equity share of INR 10- each held by the shareholders on the cut-off date of Sep. 14, 2022. Last month, Dolly Khanna, a renowned investor and stock market trader, increased her stake in the firm to 3.9% from 3.6% reflecting the bullish outlook on stock.