Aptech Ltd. (NSE: APTECH) is a well-established company in the non-formal education and training sector with a global presence. Founded in 1986, the company has a strong reputation as a pioneer in the industry, having trained students, professionals, universities, and corporates through its various streams of business. Aptech has a diverse portfolio, with a presence in sectors such as IT training, media & entertainment, retail & aviation, beauty & wellness, banking & finance, and pre-school education. The company has two main streams of business: Individual Training and Enterprise Business Group.

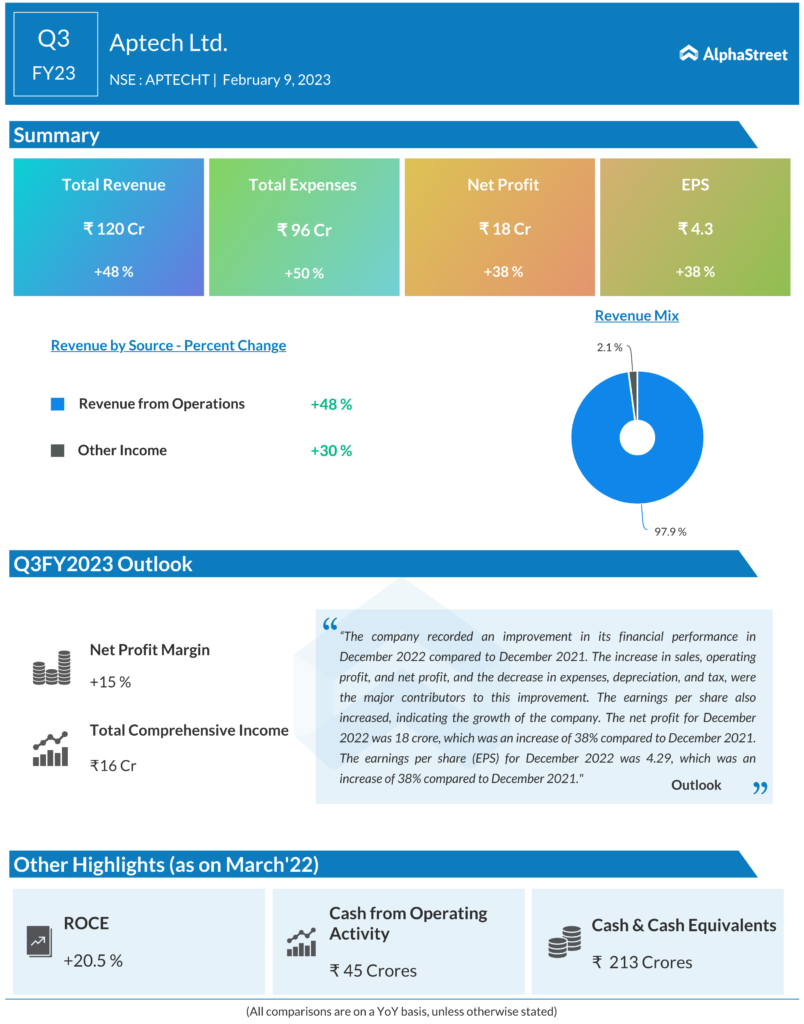

The company recorded an improvement in its financial performance in December 2022 compared to December 2021. The increase in sales, operating profit, and net profit, and the decrease in expenses, depreciation, and tax, were the major contributors to this improvement. The earnings per share also increased, indicating the growth of the company.